This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

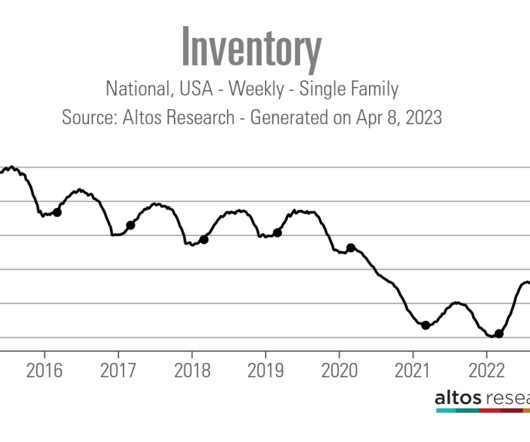

Since most sellers are buyers, inventory should be stable if demand is stable. million, currently at 1,110,000 As you can see above, inventory grew at a healthy clip in previous decades and then had a parabolic run higher in 2006 and 2007 when active inventory reached 4 million. So you can see why we have so few stressed sellers.

Typically we have a natural set of newlistings each year; inventory rises in the spring and summer and then falls in the fall and winter. It wasn’t the rate move that caught my attention — it was the newlisting data. As you can see below, that sharp move to 6.25% caused newlisting data to stall at first.

On Wednesday, existing home sales collapsed near the lows we saw during COVID-19 and back in 2007 when the housing bubble burst. “The principal factor was the rapid increase in mortgage rates, which hurt housing affordability and reduced incentives for homeowners to list their homes. .” Confused by this?

Weekly housing inventory Since newlisting data was trending at all-time lows in 2023, some feared we wouldn’t see the typical spring inventory increase. After the last few weeks , we can put that fear aside: we are finally getting the seasonal increase in active listing. didn’t go into recession until 2008.

The seasonal housing inventory bottom evaded us again last week as active listings fell and newlisting inventory decreased. Here’s a quick rundown of the last week: Active inventory fell 5,383 last week, and newlisting data is still trending at all-time lows in 2023.

These were forced credit sellers, which means these sellers don’t sell to buy a home like a traditional seller does. Since they were distressed forced sellers, inventory skyrocketed in 2006 and stayed very elevated in 2007 and 2008. Total inventory levels. NAR: Total Inventory levels 1.22

Active inventory rose by 823 single-family homes and newlisting data is trending at all-time lows. The NAR data going back decades shows how difficult it’s been to get back to anything normal on the active listing side. In 2007, when sales were down big, total active listings peaked at over 4 million. but now U.S.

As the spring selling season kicks off, many educated sellers know that buyers are experiencing spring fever and are tired of sitting on the fence watching home prices increase. In Denver in particular, newlistings increased 29.12% month-over-month and 22.63% year-over-year.

The one thing that is positive this year which is different than last year is newlisting data is rising year over year, nothing spectacular, but it’s a positive story for housing This means we have more sellers that will be buyers in 2024. million, and in 2007, it peaked at 4 million.

That’s according to Black Knight , which just released a white paper that studies how long it would take to sell all the homes currently listed for sale in a given market based on a prevailing sales rate, if no newlistings are added (a metric it calls “months of remaining inventory”).

Seasonal impacts are the norm with housing, and newlisting data is negative 6% year to date. We saw newlisting data decline when rates got to 6.25% the first time. A traditional seller is primarily a homebuyer, so not only do we lose the inventory for sale when this happens, but we also lose a buyer. months to 3.3

However, the glaring difference today versus the recession of 2008, is that in 2007 the builders had to deal with over 4 million active listings as competition for their pricey new homes. The builders will pull back on construction when the supply is 6.5 months and above.

However, the real positive story here is that even with newlisting data trending at an all-time low, we are getting the growth in active listings we traditionally see in the spring and summer. In addition, newlisting data turned negative year over year after the second half of 2022.

If we are trending below 4 million — a possibility with newlisting data trending at all-time lows — then we have much weaker demand than people think. million before we saw the massive stress spike in supply from 2005 to 2007. We have a workable range for 2023 sales in the existing home sales market between 4 million and 4.6

I don’t need to see total active listing get back to the historical range of 2-2.5 Newlistings are declining now. One of the issues with existing home inventory has been that, for the most part, a traditional seller is usually a buyer of a home. This is not encouraging news at all, in my view. From Redfin.

One of my biggest concerns for housing started at the end of June 2022: once mortgage rates got above 6%, the newlisting data began to decline faster and earlier than normal. This is a problem for the existing home sales market since a traditional seller is usually also a buyer, so the lack of listing growth was a big hit to demand.

The median price of the newlistings this week is $399,900. As the summer progresses, each subsequent week of newlistings gets priced at a slight discount to the previous weeks. During the GFC, inventory rose in 2007, 2008, 2009 and 2010. Sellers are in much better shape than they were last year.

The chart (below) puts it in sharp focus: Except for the pandemic year of 2020 when there were 2559 newlistings that April, last month was the slowest April since at least 2008 when easy access to Northwest Multiple Listing Service data became available. Where are all the sellers? between May 2007 and January 2012.

If you take 2007-2011 out of the equation, we have had only one year go negative; that was 1990, and that was only a 1% decline. To get a real price crash, we would need to see a surge of housing inventory and distressed sellers. In 2007, active inventory spiked to 4 million. million in September. Today, it’s only at 1.39

Inventory of homes listed reached a record low by July of 2023 , and mortgage rates increased dramatically, diminishing buyer affordability. Many sellers are holding the line, and buyers continue to face competition. If a home has been listed and isn’t selling, that means the list price may be too high.

Further down the funnel are more engaged consumers applying for mortgages, followed by buyers and sellers reaching mutual agreement on a deal, and then happy homeowners moving in at the end of the funnel. Meantime, the number of contract listings – known as Pending sales – rose 6.1% The number of Active listings is another eye-opener.

First a look at September’s numbers: A wave of last-chance listings for the year hit the market after Labor Day. That increased newlistings by 7.5% (2884) and available homes on the market by 12% (3602) between Sept. Seattle alone saw a 29% (1213) monthly increase in newlistings. 1 and Oct.

The sellers custom built the home between 2007 and 2009, using high-end materials and finishes, including a wall of windows and 26-foot-high ceilings in the great room. The seller wanted that to be a part of the home, and he didn’t want it down in a cellar. But the MLS is also finding new benefits in its partnership with RPR®.

.” [00:04:36] Austin real estate sales volume and velocity in April 2023 Austin’s housing market in April saw a decline in newlistings and sales volume, but the market remains a seller’s market. However, a decrease in newlistings is helping to stave off even higher inventory.

The county saw the combined number of single-family, townhome and condo listings increase in June by 4.4% While that percentage may appear strong, it’s nothing compared to the April-to-May rise of 18%, signaling a probable cooling of newlistings in the future. New single-family-home listings rose 3.8%

NAR total inventory since 1982: I prefer the Altos Research weekly single-family data to the NAR data because it gives us a fresh look at not only active listing data but newlisting data. The Altos Research newlisting data is essential in tracking the supply aspect of housing, which is why I include it as part of the Tracker.

Others – Meritage Homes (+20% YoY in 2021) and Tri Point Homes (+15-30% YoY in 2022) – expect tremendous growth of new communities. And many of the new projects are larger than in years past. That’s the most since 2007. Active listings as of Sept. The sellers are seeking $3.86M, $1222/sq. SMILE FOR THE CAMERA.

This looks a lot like the housing boom that we saw prior to the 2007–09 financial crisis.” That percentage was last seen in September 2007 – yes, at the start of the housing crisis (as the chart shows). ” The increased number of listings and slight slow-down of the market have helped boost inventory numbers.

The excess of inventory that occurred in 2007, 2008 and ’09, was an anomaly,” said Marci Rossell, former chief economist for CNBC. The county saw newlistings and end-month Active listings rise but Pending sales slip, suggesting buyers are no longer snatching every listing on the Northwest MLS as they become available.

There are at least five factors that make this housing environment far different – and more stable – than roughly a decade ago: Low inventory and lack of supply – There were some 4 million homes on the market nationally in July 2007 compared with about 1.1 The average King County single-family listing sold in May 9.5% lodge home.

As you can see in the chart below, the credit markets broke in 2005, 2006, 2007 and 2008, and then the job-loss recession of 2008 started, which made things much worse. The newlistings data we track with Altos Research is trending at the lowest levels ever during the past few years, while back then it was running at accelerated levels.

This year was mostly disappointing for buyers and sellers hoping to find a new home. Please have a look for a deeper dive and I encourage prospective buyers and sellers to discuss 2025 real estate goals with a seasoned broker (like me!) The number of newlistings tumbled 48% from October and was down 2.7%

We built a new garage and completely did the heavy work with a $50,000 new roof, new drainage, new retaining walls, landscaping (including removal of alder trees), interior was completely redone, new lighting, new skylights, you name it. In fact, we had about 3,500 more newlistings than 2023 in the region.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content