This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Economists and housing experts say mortgage lending standards will likely loosen in 2021, despite the increased risk of delinquencies ahead. The post Why mortgage lending standards will ease in 2021 appeared first on HousingWire. Such a scenario illustrates the growing disparities in the U.S. housing market.

That is how the director of the Consumer Financial Protection Bureau (CFPB), Rohit Chopra , began his remarks marking the 15th anniversary of the collapse of Lehman Brothers , the first proverbial domino to fall in the financial crisis of 2007-08 that ultimately gave rise to the establishment of the CFPB.

mortgage insurance market in 2023 to deteriorate. That will be offset by stable insurance in force, driven by increased persistency — a percentage that indicates the number of clients that an insurance company retained, the credit rating agency said in a separate report. mortgage insurance sector, according to the report.

Those loans, originated between 2007 and 2011, defaulted and led to claims to the FHA for mortgage insurance. The lawsuit, brought initially in 2016, alleged that Guild knowingly originated and underwrote mortgages that didn’t meet the program requirements of the FHA.

His senior executive management positions include nine years as president and COO of the nation’s largest title insurance company, Chairman and Co-CEO of a software company, and CEO of a real estate data and information company. The post The Week Ahead: Preparing for 2025 appeared first on Appraisal Buzz.

As bank regulators conduct a major CRA rulemaking, an honest assessment of CRA is that it has not been effective when it comes to bank mortgage lending. Instead, there are more effective ways to increase mortgage lending to underserved and minority borrowers. So why would we extend it to IMBs? These are all laudable social objectives.

In 2007, when sales were down big, total active listings peaked at over 4 million. We had high inventory levels while the unemployment rate was still excellent in 2007. This proves that the mass supply growth we saw from 2005-2007 was due to credit stress, not because the economy was in a recession; the U.S.

Data from John Burns Real Estate Consulting shows that student loan debt has increased 100% since 2007, keeping many renters in place. FHA loans are insured by the Federal Housing Administration and have less stringent down payment and credit requirements. Jeff Ball is CEO of Viseo Lending. Here’s one data point for you.

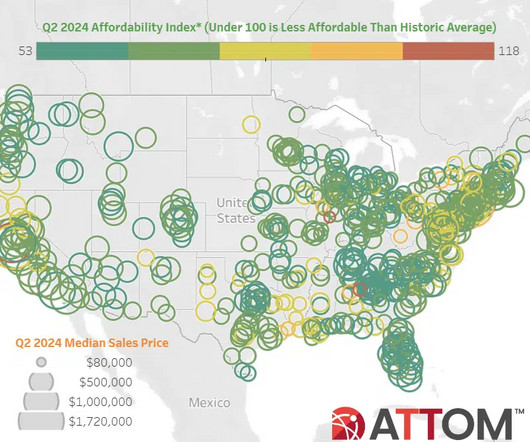

Major homeownership expenses – including mortgage payments, property taxes and insurance – now consume about 35% of the average wage nationwide, according to ATTOM’s U.S. of the average national wage in the second quarter – marking the high point since 2007 and standing well above the common 28% lending guideline. annually.

During this webinar, Fitch Ratings will present a cross-section of industry stakeholders discussing the drivers of housing economy expansion, factors impacting homebuilder credit, the home loan lending environment, and mortgage delinquency expectations. He joined Fitch in 2007, and has held various roles since then.

In its most recent annual report to Congress, November 2020, the Federal Housing Administration ( FHA ) published its “capital ratio,” a measure of capital reserves to insurance-in-force held within the Mutual Mortgage Insurance Fund (MMI Fund). The same report revealed FHA had amassed capital reserves in the amount of $78.9

Morgan in Hong Kong from 2007-2009, after serving that company in various capacities in New York for 22 years. FHLBank products and resources help support community lending, housing, and economic development. Previously, he was COO of FHLBank Pittsburgh, a position that he assumed in November 2009.

Switzerland-based global lender Credit Suisse Group AG had a rough start this week after its stock was beaten down by 11%, the value of its riskiest debt fell more than 10% and the cost of purchasing derivatives insuring against the bank defaulting rose sharply. We believe the U.S. this year through September.

In her role as CEO, Priya leads NHT’s engagement in public policy, lending, and energy sustainability. Since 2007, Palmer has overseen an experienced leadership team in several key national homebuilding markets. He also created the Center’s latest household growth projections.

NOTE: Please scroll down to read the other topics in this long blog post on non-lender appraisals, VA, flood and fires no insurance, retirement, few lender appraisals, unusual homes, mortgage origination $22M Modern Mansion on 130 Acres in Napa Has Its Own Cabernet Vineyard Excerpts: 6 bedrooms, 6.5+ The GSEs started keeping track in 71.

“A lot of them are here to stay because they’ve seen what Florida has to offer,” said Ronald Pietkewicz, Bank of America preferred lending market leader for Palm Beach County and the Treasure Coast. “We Landlords note that their costs are going up also with non-homesteaded properties getting hit with tax hikes and higher insurance premiums.

I) Relaxing of lending standards and predatory lending activity (non-prime is just another word for sub-prime). So many appraisers missed the early signs in the last boom’s bust that resulted in claims (valid or not) of over-valuations followed by lawsuits, E&O insurance claims, and regulatory disciplinary actions.

Heaslet is a retired Marine Corps veteran and a second-generation appraiser who began his valuation career as a trainee at his father’s office in 2007. VA is the only lending organization I recommend for appraisers, except for direct lenders. I have expensive, and limited, earthquake insurance. Big Mistake. Are values affected?

Lenders rely on reviews to ensure the accuracy and reliability of appraisals before making lending decisions. Insurance companies use them for verifying property values in underwriting and claims. It was my last review for lending purposes. Investors use them to evaluate the value and risk of potential investments.

In 2007, he started appraising conservation easements, which are specified areas of land earmarked for environmental conservation. . … Roberts faces a maximum of five years in prison and will be sentenced in six months. The fraud started in 2008, one year after Roberts became a licensed appraiser, according to court documents and statements.

of the average national wage, which is higher than the standard lending guideline of 28 percent and represents the highest level since 2007. The average cost of homeowner insurance, mortgage insurance, property taxes, and mortgage payments ($2,114) in the country set a new record last quarter, accounting for 35.1%

While investors of mortgaged securities help dictate their interest rates, the Federal Reserve is behind the scenes influencing the overall lending environment. Waller went on to say this adjustment is in no way like the horrific housing/financial crises of 2007-2010. That’s the first time a Fed official has acknowledged the U.S.

There has been a flurry of recent articles prognosticating a decrease to Federal Housing Administration (FHA) insurance premiums. At least 137,000 of those borrowers have FHA-insured loans. FHA’s Mutual Mortgage Insurance Fund (MMI Fund) is there to be the primary buffer against these inevitable shifts in housing and the economy.

Congress has opportunities to address some of the challenges financial technology firms face in the lending sector. The pace of financial technology innovation in the alternative lending space is nothing short of phenomenal, but it has meant headaches for lenders and vendors waiting for regulation to play catch-up.

According to her LinkedIn profile, she worked at the Center for Responsible Learning from 2007 to 2011, at the Federal Housing Finance Agency from 2011 to 2012 and at the Center for American Progress from 2012 to 2015. In March 2021, Fudge said that the agency had “no near-term plans” to change FHA’s mortgage insurance premium pricing.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content