This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

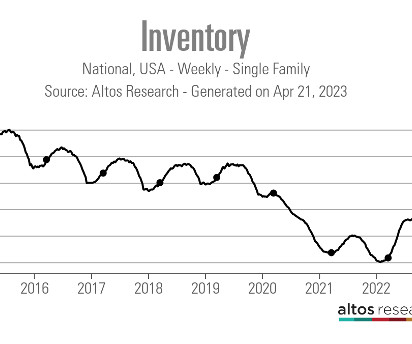

You can see the drastic change this made in the Mortgage Bankers Association Credit Availability index , below, which skyrocketed in 2005 and 2006 before an epic collapse in 2008. Just look how lousy credit looked below in 2005, 2006 and 2007 — all before the job-loss recession in 2008. Demographics also play a role here.

Here’s a quick rundown of the last week: Active listings rose by 8,546 , and newlisting data showed some growth. If that is the case, then this week’s gain in active inventory and newlistings needs to be taken with a grain of salt until we get next week’s data. However, I will take what I can now.

What I mean by a credit bust is that after the housing bubble burst in 2005 into 2006, we saw a massive increase in supply. Since they were distressed forced sellers, inventory skyrocketed in 2006 and stayed very elevated in 2007 and 2008. Only from 2006-2011 did we see this break due to forced sellers who couldn’t buy homes.

But since we have such low active listings today, even with 2024 being another year of low home sales, the days on the market are still under 30 days, which means homes that are priced right are selling quickly. Newlistings The most significant and glaring difference between 2011 and 2024 is the weekly newlistings data for the peak season.

The one period where this didn’t happen was from 2006-2011, when credit forced Americans to sell, to rent or to be homeless. During that period, we saw newlisting data decline. Total housing costs for American homeowners versus their wages are meager, and most will buy a home right away when they sell.

This explains why total active listing inventory data has been stable over the decades, with the exception of 2006-2011, when those forced distressed credit home sellers couldn’t buy. Mortgage rates spiked in March, and then the newlisting data started to decline at the end of June.

metropolitan areas in February 2022, based on year-over-year growth in median listing price according to the residential real estate listing website, Realtor.com. The table also reports the year-over-year percent change in newlistings for each market. Table 1, below, reports the 10 hottest U.S. Bellingham, WA 51.7% -8.3%

In February, the number of homes available for sale fell for the fifth consecutive month, and newlistings ran 27% below pre-pandemic levels. In addition, 47 of 50 markets saw their active listing count decline that month. On the bright side, homeowners with mortgages still had $9.3 In February, it took 33.2%

I don’t need to see total active listing get back to the historical range of 2-2.5 Newlistings are declining now. Inventory is always seasonal, but the decline in newlistings this year was not what I wanted to see. This is not encouraging news at all, in my view. From Redfin.

However, weeks after that call, the newlisting data started to decline noticeably, which makes that call much harder to happen in 2023. However, I acknowledge that the housing dynamics have changed a lot since that forecast in June as newlisting data declined. million in 2023. million for 2023. Housing recession.

The only time this happened was 2006-2011 — the housing bust years. However, 5%-6% mortgage rates did change the marketplace and now 6%-7% mortgage rates are changing behavior so that we see newlisting data declining even more as sellers are calling it quits on their plan to list.

Moreover, 30% of El Paso shoppers are looking at local homes from out-of-state, with top views coming from New York, Albuquerque, and Los Angeles.”. A Redfin statistical study of the El Paso housing market showed a 2% year-over year rise in newlistings (936 from September 2019 to 956 in September 2020) and a gigantic 40.3%

While there is no doubt it is a seller’s market in Peoria, Van Cleve said many potential sellers are hesitant to list. Although housing market conditions may be challenging heading into the spring season, agents in the inventory-strapped state are optimistic that newlistings will soon be coming to market.

What can’t happen is mortgage rates above 7%, since that level hasn’t fueled newlistings, which means less demand, and the builders simply are done building anything new with rates that high. The housing market getting some stabilization will be a plus as we saw some buyers come into the marketplace with rates at 5%.

The reasons it will avoid a crash, according to Zandi, are that overall housing-inventory levels remain relatively tight by historical measures; mortgages overall have and continue to benefit from solid underwriting and oversight; and we are not seeing the kind of speculation that marked the housing market in the run-up to the 2006/07 crash. “I

The housing market is entering the ‘most significant contraction in activity since 2006,’ says Freddie Mac economist” (Fortune). Consequently, prices of new homes should follow a similar downward path, although the trajectory is the question. The number of home listings remains low nationally.

Consequently, we’re witnessing the lowest number of newlistings since 2000. The hesitation to lose rates in the 3% range, coupled with concerns about higher monthly payments upon buying again, has resulted in a scarcity of newlistings.

Therefore, we are in a market with the lowest amount of newlistings since 1994. The lack of listings is a major factor in how low inventory is, so buyers are still competing, and this is why prices haven’t fallen. It’s a misconception that rates only impact buyers and 2023 is a perfect example of that.

2023 Sees the Lowest Number of Homes Listed in Twenty-Two Years In 2023, there was an 12% decrease in listings compared to 2022, with 20,546 homes listed compared to 23,342 in the previous year. Contrary to popular belief, interest rates don’t just impact buyers, they impact sellers as well as demonstrated in 2023.

First a look at September’s numbers: A wave of last-chance listings for the year hit the market after Labor Day. That increased newlistings by 7.5% (2884 units) and available homes on the market by 12% (3602) from Sept. Seattle alone saw a 29% (1213) monthly increase in newlistings. bath , 5546 sq.

The rate of homes hitting the market was also about one-third stronger than in January 2024 and, at 2533 newlistings, it is the most of any January in four years. That is quite a rebound from late 2024 when only 950 listings hit the market for all home types single-family, townhomes and condos combined. bath , 6290 sq.

The 323,465 flipped single-family, condo and townhomes in 2021 is the highest number since 2006 and represented 5.5% That includes 621 fewer Pending contracts in April 2022 than the previous April, as the net number of newlistings remains on average lower than in years past. of all home sales last year.

This was the fastest pace for combined single-family and multi-family construction since June 2006. The county saw newlistings and end-month Active listings rise but Pending sales slip, suggesting buyers are no longer snatching every listing on the Northwest MLS as they become available. million units.

“Last month, existing home sales recorded their best bottom line in any April since 2006,” Speakman said. “Newlistings volume got a decent bump in March and April, and more people believe it’s a good time to sell a home than at any time since the pandemic began.”

Lawrence Yun also said this figure will be the highest rate of sales since 2006. Some highlights from the Northwest Multiple Listing Service (through July): The combined number of condo, townhome and single-family homes on the market as of Aug. The number of newlistings for all home types (4428) fell 7.8%

As proof of the impact of the country’s low inventory and high cost of building materials , newlistings fell 16% – the second-largest decline on record since Redfin’s data began in 2012, only passed by the drop in April 2020. “This is the strongest seller’s market since at least 2006,” Fairweather said.

As you can see in the chart below, the credit markets broke in 2005, 2006, 2007 and 2008, and then the job-loss recession of 2008 started, which made things much worse. The newlistings data we track with Altos Research is trending at the lowest levels ever during the past few years, while back then it was running at accelerated levels.

The longest such streak occurred for over 12-years, notching 153 consecutive all-time highs from July 1993 to March 2006. In fact, listing prices have eased in recent months as sellers look to attract buyers and more small, affordable homes come up for sale. In December, the Case-Shiller index shows home prices up 5.6%

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content