This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As housing affordability reached its lowest point since 2006, one group stood out in defying market trendssingle women. Each mortgage payment serves as a form of forced savings, helping homeowners build wealth over time. housing trends. This modest increase continues a recovery from its 2016 low of 49.3%

Employment data for October is set to be released Friday, and it will go a long way in determining the path for mortgage rates, which have surged upward in the past month. At HousingWire’s Mortgage Rates Center on Tuesday, the average rate for 30-year conforming loans was 6.72%. This equated to homes being 9.2% renter population.

Low mortgage rates and incredible buyer demand won out over pressure from soaring lumber prices in March as single-family new home sales rose 20.7% million seasonally adjusted annual rate, according to the Department of Housing and Urban Development and the U.S. This is the fastest sales pace since September 2006. .

Since the weaker CPI data was released in November, bond yields and mortgage rates have been heading lower. The question then was: What would lower mortgage rates do to this data? Now, with five weeks of data in front of us, we can say they have stabilized the market. Mortgage rates went from a low of 2.5%

in February, which was the first month to see price growth greater than 20%, according to Black Knight ’s monthly mortgage monitor report. housing was the least affordable ever back in July 2006 when it took 34.1% Since the start of 2022, rates have gone up 200 basis points and housing prices have surged 5.9%.

That’s up 37% from a year ago, but it’s important to take into account that the COVID-19 virus first took hold of the housingmarket in March 2020, said Doug Duncan, chief economist at Fannie Mae. “The March pace was the second strongest since 2006, surpassed only by this past December’s reading,” Duncan said.

The deadliest pandemic in more than a century has failed to derail the housingmarket because of the lowest mortgage rates ever recorded coupled with a shift in how people use their homes. rate for a 30-year fixed mortgage has been under 3% since late July, as measured weekly by Freddie Mac. The average U.S.

Existing home sales came in at a whopping 6,850,000 , beating estimates with the highest print since 2006. Days on market fell from 36 days to 21 days on a year-over-year basis. The housingmarket is hot. You may be told that future moderation indicates “cracks in the housingmarket, but don’t buy into it.

Forecasts for the housingmarket in 2025 are not that rosy, but Ryan McKeveny and Brian Hale see this as a good thing for the years ahead. With some improvement in mortgage rates and affordability, both home sales and refinance can come back pretty quickly. But, in order to get there, mortgage spreads must improve.

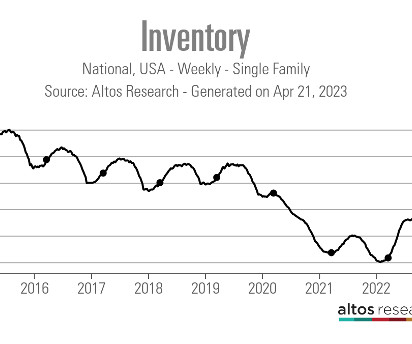

Can we now say that the housingmarket ‘s spring selling season is finally underway? Since 2020, the seasonal bottom for housing inventory has arrived several months later than normal, making it more complicated to track housing inventory data. months shows how far we are from 2008 housing economics.

housingmarket , trailing only married couples. That was only seven years after women were legally allowed to obtain a mortgage without a cosigner. “The highest share of single women buyers was in 2006, when the share stood at 22%. Between 2016 and 2024, the share of single women was between 17% and 20%.”

The 2022 housingmarket was savagely unhealthy , with all-time lows in inventory leading to massive bidding wars and price spikes until the Fed put a screeching halt to all of it with rate hikes that resulted in the most significant one-year spike in mortgage rate history. Mortgage rates. Home price s.

million , with double-digit home-price growth driving a housingmarket that is still savagely unhealthy. However, this year has seen one big game-changer: the 10-year yield finally cracked over 1.94%, which drove mortgage rates over 4%. As we can see below clearly, the market worsened before the job-loss recession happened.

As we close out 2022, it’s time to reflect on a historic year for the housingmarket, which was even crazier than the COVID-19 year of 2020. Housing permits and starts are falling now, even with the backlog of homes in the system. With less transaction volume , general incomes in the housing sector are falling.

Bringing together some of the top economists and researchers in housing, the event will provide an in-depth look at the top predictions for this year, along with a roundtable discussion on how these insights apply to your business. In addition, more for-sale inventory will likely be available on the market.

The June housing starts data beat estimates with positive revisions, however, this doesn’t change the housingmarket recession call that I made last month. The smart thing to do is go with the builder sentiment trend until it reverses, and most likely, we will need to see lower mortgage rates for that to happen.

Recent market trends — including an improvement in mortgage rates, housing affordability and potential refinance opportunities — suggest positive signs for the real estate market this year, according to February’s Mortgage Monitor report from Intercontinental Exchange (ICE). Mortgage rates held at 6.71% as of Jan.

From 1998 to 2006, according to Freddie Mac , the median annual mortgage rate was 6.45%. Therefore, there were more housing sales in 1996 than there will be this year. Mortgage rates today are not much higher than they were then. This is something that housing industry leaders should be thinking about — carefully.

RealTrends has been tracking housingmarket data since 1979, including households, home sales, average mortgage rates , etc. Even during the downturn of 2006-2010, this factor only hit a low of 3.84% (2010). Mortgage rates are not likely to return to the 3.0% How bad was last year? The factor for 2023 was 3.58%.

One of the reasons that I moved into the “team higher mortgage rate” camp is that what I saw in January, February, and March of this year was so unhealthy that I labeled the housingmarket savagely unhealthy. However, a cool-down in prices is not the same thing as a housing crash. before COVID) stage.

Local markets spotlights 5 different areas across the country, showcasing what is uniquely happening in those housingmarkets. Local real estate agents, loan officers and appraisers share what characteristics are currently defining their housingmarkets. Annapolis, Maryland. Become a member today. Already a member?

Prices have risen every month in 2024, even as mortgage rates have remained stubbornly high and as housing affordability has reached an all-time low. Berner continued: Purchasing a home is especially difficult right now because of high mortgage rates. Measuring Year-Over-Year Gains, Cities With the Highest Growth The U.S.

June saw both record-low home price appreciation and the largest single-month increase of for-sale inventory in 12 years, resulting in a cool down in the housingmarket. And the housingmarket would likely slow further in the coming months if mortgage rates remain persistently high.

Today’s housingmarket suffers from affordability issues due to mortgage rates in the 7s and high home prices. People are quick to panic over any part of the housingmarket that looks stressed, fearing we’ll see 2008 levels of destruction all over again. Why choose 2011?

Rising interest rates and a slowing economy overall are already taking some of the air out of the rapid home-price appreciation the housingmarket has experience over the past year, according to the recently released Federal Reserve Beige Book for July. Overall, annual mortgage origination levels are expected to be $2.8

A few months ago, the United States housingmarket failed Econ 101. The table also reports the year-over-year percent change in new listings for each market. The table also reports the year-over-year percent change in new listings for each market. Table 1, below, reports the 10 hottest U.S. Bellingham, WA 51.7% -8.3%

According to multiple real estate agents and mortgage brokers, low interest rates and a high percentage of “essential” jobs in their town has kept the housingmarket and local economy strong. rise in houses sold in the same timeframe – from 670 to 940. The post Why is the El Paso housingmarket so hot right now?

After 2010, qualified mortgage laws were in place, meaning everyone getting a mortgage has to be able to repay the loan. You can see the drastic change this made in the Mortgage Bankers Association Credit Availability index , below, which skyrocketed in 2005 and 2006 before an epic collapse in 2008.

Does this mean the Federal Reserve needs to hike rates even more to get the recession they’re looking for, or is there a case for mortgage rates to go below 6% over the next six months? After the GDP report came out, the bond market rallied, sending yields lower, which some people were confused about. was in a recession.

For the third consecutive week, mortgage rates managed to remain under 3%, dropping three basis points last week to an average of 2.96%, according to Freddie Mac ‘s PMMS. Despite consistent forecasts of a market with rising rates, the 30-year fixed rate mirrored more closely numbers borrowers saw back in February.

Mortgage demand continues to decline amid surging home loan rates, according to the latest survey from the Mortgage Bankers Association (MBA). . The mortgage composite index for the week ending Oct. According to Mortgage News Daily, the 30-year fixed rate mortgage on Tuesday was 7.14% on average. two weeks prior.

While we may be ready to firmly plant our feet in 2021, we shouldn’t leave the past 12 months behind without taking a critical look at how the COVID-19 pandemic has impacted the housingmarket, and how it will pave the way for 2021 and beyond.

housingmarket was the single best outperforming economic sector globally during the COVID-19 pandemic in 2020. The reasons for that are solid demographics and low mortgage rates , which will not change much in 2021. Due to the solid demand for homes, housing supply for both new and existing homes are at all-time lows.

soared 18% year-over-year in March 2021 to a median of $356,000, according to a report Redfin released Friday that provided stark evidence of a housingmarket where demand greatly exceeds supply. Homes sold in March were on the market for 21 days, per the report, the shortest period between listing and sale since 2012.

It’s an excellent time to discuss housing inventory. The housingmarket shifted in March of this year. As the 10-year yield broke above 1.94% and mortgage rates rose, we saw the impact on housing data. Yes, crazy to think, but this is a survey trend data line, and the housingmarket was in free-fall at that time.

Mortgage rate buydowns and a limited supply of existing homes have buoyed housing demand for many months despite elevated interest rates. Meanwhile, homeowners who bought in January 2000, January 2006 and January 2013 have received boosts of $414,000, $338,000, and $343,000, respectively. Overall, U.S. homeowners held $31.8

Home price growth slowed in May, showing signs of a cooling housingmarket. But housing is the least affordable it has been since the mid-1980s as mortgage rates rise and home values soar, driven by low housing inventory, a new Black Knight report suggests. in May from a revised 20.4% in May from a revised 20.4%

Despite what they promised, we sit here today with the United States housingmarket outperforming all other economic sectors in the world during the pandemic. In order for the housingmarket to crash due to too many loans going into default when forbearance programs end, the number of loans in these programs needs to grow.

housingmarket , we just experienced an event that most people never thought could happen. Total housing costs for American homeowners versus their wages are meager, and most will buy a home right away when they sell. Looking at housing this way, the last four decades make sense. The days on market were too low.

“This is about the same rate of price growth that occurred during the 2002 through 2006 period when subprime lending drove exuberant housing demand. “But that is where the similarities end. Mortgage holders are well-qualified and subprime loans are rare. ”

I already hear murmurs from the fear-mongering housing bears that once the forbearance plans expire, we can expect to see a collapse of the housingmarket in America like we haven’t seen since the bubble years. The post Here’s why we won’t see a housing crisis after COVID-19 appeared first on HousingWire.

At CoreLogic, Nothaft headed the office of the economist, providing analysis, commentary and forecasting trends in global real estate, insurance and mortgagemarkets. Most people knew Frank as one of the nation’s premier housing economists,” said Robin Wachner, a CoreLogic spokesperson. Henry Wallich.

HW Media , publisher of HousingWire , RealTrends and Reverse Mortgage Daily , announced today that it has closed on the strategic acquisition of Altos Research , the premier resource for real-time real estate data, providing weekly market statistics, analysis and reporting for 99% of the zip codes in the U.S.

The data and analytics firm singled out mortgage rates, which were around 5.5% Following June’s surge in mortgage rates and the resulting dampening effect on housing demand, price growth is taking a decisive turn,” said Selma Hepp, interim lead of the Office of the Chief Economist at CoreLogic. “And by July 2023.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content