This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Thats the highest share for new sales since 2005, which was during the building boom driven by cheaper housing, looser credit requirements and high demand for mortgage-backed securities. In the current climate, homebuilders have advantages over existing-home sellers.

Ive been doing this since 2005 and I tell clients that Ive never seen a market like this, so we have to navigate it together. Its a symptom of a market thats transitioning away from sellers. Altos considers anything above 30 to be indicative of a seller’s market. A substantial drop in new listings is a contributing factor.

There’s a showdown at the housing market corral between homebuyers and sellers. This means the housing boom period of 2002-2005 had major credit tightening, which won’t happen this time around when the next recession hits. Home prices ebb and flow, pricing was working in the sense that sellers met homebuyers to a degree.

The housing market of 2002-2005 had four years of sales growth facilitated by credit. As we can see below, the purchase application data had four years of growth, peaking in 2005 and then collapsing. However, what isn’t identical is that we have not had a massive sales boom like we saw from 2002-2005. million in 2005.

As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. What I mean by a credit bust is that after the housing bubble burst in 2005 into 2006, we saw a massive increase in supply. Total inventory levels. NAR: Total Inventory levels 1.22

But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. This time around, we have not seen the kind of housing credit boom that we did from 2002-2005. Purchase application data is now below 2008 levels! This means less demand for housing.

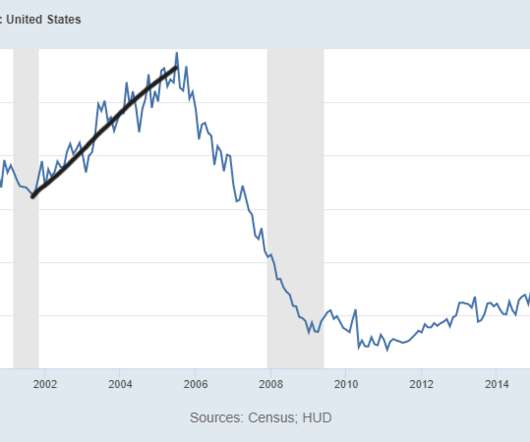

You can see the drastic change this made in the Mortgage Bankers Association Credit Availability index , below, which skyrocketed in 2005 and 2006 before an epic collapse in 2008. Since most sellers are buyers, inventory should be stable if demand is stable. So you can see why we have so few stressed sellers.

That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. However, the spike in inventory that we saw from 2006 to 2011 can be attributed to the massive credit bubble we had from 2002 to 2005. Credit stress was evident from 2005 to 2008. What is going on here?

Homebuyers’ median household income increased by $19,000 this year from 2022, reaching $107,000, according to the National Association of Realtors ’ 2023 Profile of Homebuyers and Sellers. The report is an annual survey of homebuyers and sellers who closed transactions between July 2022 and June 2023.

million level we saw in 2005. However, it does show that the builders are in a much better spot to deal with their massive supply, compared to the 2005-2008 period. They are good at selling their inventory much quicker than existing home sellers, who might still be stingy on prices. below the August 2021 estimate of 686,000.

.” One of the housing economic realities that I have been trying to stress this year is that a traditional seller of a home is typically a buyer as well. This explains why total active listing inventory data has been stable over the decades, with the exception of 2006-2011, when those forced distressed credit home sellers couldn’t buy.

Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. The housing market can’t replicate the type of massive credit expansion we saw from 2002-2005, so the price-growth story has more to do with inventory collapsing to all-time lows. Even today, the MBA purchase application index is below 2008 levels.

can’t have a credit sales boom like we saw from 2002-2005. This means we won’t be working from record-breaking demand of high sales like we did at the peak of 2005. The builders are in a better position to manage their inventory glut than when they were working from a credit boom in 2005 that took new home sales up to 1.4

However, we haven’t had a credit sales boom like the one we saw from 2002-2005. Total Inventory had been growing from 2001-2005; total listings data in 2005 was at the higher historical range of 2.5 However, not to the degree we saw from 2005-2008. million listings. Today, we stand at 1,310,000 active listings.

I know some people don’t agree with me on this, but the price gains in both the existing home and new home sales sector show that homebuilders and sellers had too much pricing power and needed to be checked. As you can see, sales levels were never elevated like what we saw from 2002-2005. The only way this happens is by higher rates.

My concern now is that some sellers are feeling stressed about this market, which should never happen because this is the best seller market ever. However, a seller is also a natural homebuyer, unless they’re an investor. You can see why some sellers are stressed now. People who sell need to live somewhere.

And the peak in existing home sales was 2005 when you had around 7 million transactions.” Last October, FHA introduced a proposed seller credit for the H4P program. “And people over 50 are 74% of total U.S. homeowners. So if you just take half of that, you’ve got about 30 million homes that should be coming on the market.

They’re effective sellers and don’t want to create a backlog of completed units for sale because that would ruin their business model. As we can see in the chart below, new home sales aren’t booming like what we saw at the peak of 2005 but are getting back to trend sales growth from the bottom we saw when rates got 5% in 2018.

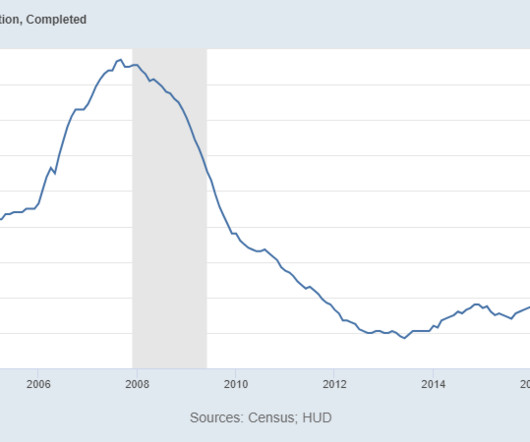

If you look at the monthly supply for new homes from 1996 to 2005, it was always lower than what we saw from 2008 to 2019. New home sales were much more substantial, of course, heading toward the bubble peak of 2005, so as long as sales rose, the homebuilders would build. Once total inventory can get back into the range of 1.52

However, what is different this year from 2023 is that we have more sellers that will be buyers. Of course, the housing market didn’t have the credit sales boom it had from 2002-2005, but it lacked inventory. Just as they did in 2023, higher rates took the winds out of the growing sales numbers.

If sales are working from an elevated number, like what we saw from 2003-2005, it’s a different subject altogether. Credit standards are still looking great, and we don’t have to worry about credit getting so tight that it will kill demand, as we saw from 2005 to 2008. And we have a lot more workers now than we did then.

The lack of sellers is also a demand problem and what we saw after June of 2022 is that sellers called it quits earlier and faster in the year than usual, resulting in total existing home sales totaling 5,030,000 to end 2022. I have often said that anytime days on the market are at a teenager level, nothing good will happen.

This is why I have called them efficient home sellers. As we can see in the chart below, sales levels aren’t exactly booming like they were from 2002-2005. The builders sell homes as a commodity, and they had a big spike in monthly supply last year, forcing them to make some deals to move product.

Between 2002-2005 in many markets, the real estate market was scorching, much like it is today. As appraisers, we faced tremendous pressure from buyers, sellers, real estate agents, and loan officers during the previous run-up. We are seeing that as a profession again. Is this any different than last time? How do we combat this?

District Court for the Western District of Missouri , the lawsuit is named after its lead plaintiff, Maryland home seller Daniel Umpa. According to the motion, at least some of the putative class members in the suit would be bound by their seller agreements to arbitrate claims, similar to HomeServices’ claims.

As you can see below, the new home sales market from 2018-2022 doesn’t look like the housing market we had from 2002-2005. Like home sellers, they try to make as much money as possible. First, as you can see from the chart below, the market we had from 2002-2005 never existed in housing from 2014-2022. percent (±11.9

If you look at the monthly supply for new homes from 1996 to 2005, it was always lower than what we saw from 2008 to 2019. New home sales were much more substantial, of course, heading toward the bubble peak of 2005, so as long as sales rose, the homebuilders would build. Once total inventory can get back into the range of 1.52

Home sellers strive to get the highest price from the best offers and homebuilders have the pricing power over consumers. Since housing tenure is now over 11 years, the built-in equity position is much higher today without a massive credit boom like what we saw from 2002-2005. In short, we made American mortgage debt great again !

million before we saw the massive stress spike in supply from 2005 to 2007. Stable demand, low housing inventory, and no forced sellers are why we created the weekly Tracker, to focus on accurate data and what matters most to housing economics and the U.S. Also, demand has stabilized since Nov. economy.

Homebuilders are efficient sellers of homes because it’s like a commodity to them; they don’t have to look for shelter after they sell or have a 3% mortgage rate they have to give up after they sell. Just look at the chart below and how bad credit looked from 2005 to 2008, then the job loss recession happened. months and above.

A traditional seller is primarily a homebuyer, so not only do we lose the inventory for sale when this happens, but we also lose a buyer. However, as we can see, the inventory data looks much different than what we saw in 2000, 2005, 2008, 2012, 2015 and 2018. This is not a positive for the housing market.

As we can see in the chart below, it’s not like the new home sales market is booming at all; we aren’t anywhere near the top of sales in 2005 or in 2020. percent (±15.2 percent)* above the revised February rate of 623,000, but is 3.4 percent (±12.7 percent)* below the March 2022 estimate of 707,000. When did this all happen?

The only period when the median sale price was greater than house-buying power was from 2005 through 2007, indicating an overvaluation of housing, or a “housing bubble.” Some buyers will pull back from the market and sellers will adjust their price expectations, which will prompt house prices to adjust.

percent)* below the December 2020 estimate of 943,000 Slow and steady wins the race and the market that we had from 2002-2005 doesn’t exist today. This is also a factor why I don’t believe in the housing construction boom premise, because when builders and sellers have pricing power they push it to the limits. This is 11.9

From the Wall Street Journal Editorial Board, “the commission on home sales has stayed basically flat for decades at 6%, split evenly between the buyer and seller agents.” Our data is good enough for the DOJ and the FTC to use for their own report on competition in the industry in their 2005-2006 report.

The truth here that nobody wants to talk about is that we didn’t have a massive sales credit boom in housing from 2020-2021 like we saw from 2002-2005. We must remember that the builders don’t operate like existing home sellers; they treat their products as commodities.

This problem is much different than the housing credit bubble of 2002-2005. Home sellers and builders had too much pricing power, pushing prices to the extreme. After 2021 ended and my price-growth model was broken after only two years and we started 2022 at all-time lows in inventory, I labeled the U.S.

Round one with the DOJ According to an antitrust lawsuit the DOJ filed against NAR in September 2005, the hesitancy and suspicion some brokers expressed over moving MLS listings online led to the creation of NAR’s “Initial VOW Policy.” You can also potentially increase your business by marketing your services to off-MLS sellers.”

Similarly, companies like Zillow and Trulia launched in 2005 and 2006 as “real estate search engines” to help buyers more easily find a home online. Having everything in-house enables iBuyers to lower closing costs for buyers and sellers, offer real-time, 24/7 customer support and provide unique financing solutions for buyers.

As you can see below, we don’t have a booming credit housing market as we saw from 2002-2005; we have steady replacement buyer demand. More choices are better for homebuyers and sellers who need to buy a home typically as well. A positive outcome for me in 2022 would be to see days on the market grow above the teenager age.

The only thing that I believe creates balance in the housing market is higher rates because the sellers and builders have too much pricing power in this low inventory environment. . This is much different from the marketplace we saw from 2002-2005, a massive credit bubble. The days on the market to sell a home is too low.

When you consider that a home seller is a natural homebuyer as well, you can see why the housing market broke after mortgage rates went on a roller coaster last year. However, 30, 60, and 90-day lates are near all-time lows, and it took many years to build up the credit stress we saw from 2005 to 2008, before the job-loss recession.

The one thing housing has going for it now is that we don’t have the speculative booming demand as we saw from 2002 to 2005. The builders have pricing power and they — along with home sellers — have pushed it very hard since 2020. From Census: The median sales price of new houses sold in March 2022 was $436,700.

We have to remember that a conventional seller is usually also a traditional buyer, so new listings growing toward their seasonal peak throws cold water on the idea that no one will list their homes because they already have a low mortgage rate (the mortgage rate lockdown theory). didn’t go into recession until 2008.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content