This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

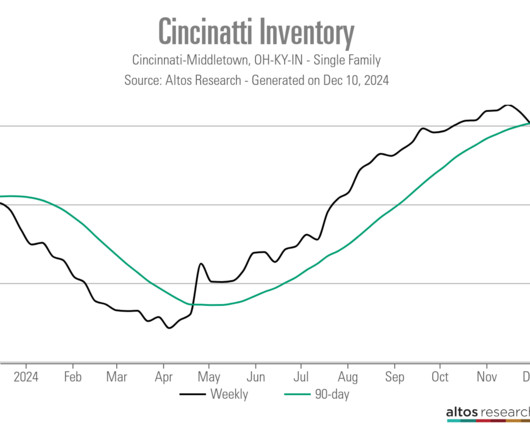

Ive been doing this since 2005 and I tell clients that Ive never seen a market like this, so we have to navigate it together. Its a symptom of a market thats transitioning away from sellers. A substantial drop in newlistings is a contributing factor. Its unpredictable, said Teena Jackson, a Redfin agent in Cincinnati.

There’s a showdown at the housing market corral between homebuyers and sellers. This means the housing boom period of 2002-2005 had major credit tightening, which won’t happen this time around when the next recession hits. Home prices ebb and flow, pricing was working in the sense that sellers met homebuyers to a degree.

But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. This time around, we have not seen the kind of housing credit boom that we did from 2002-2005. Newlisting data is down 5% year to date, as you can imagine.

You can see the drastic change this made in the Mortgage Bankers Association Credit Availability index , below, which skyrocketed in 2005 and 2006 before an epic collapse in 2008. Since most sellers are buyers, inventory should be stable if demand is stable. So you can see why we have so few stressed sellers.

.” One of the housing economic realities that I have been trying to stress this year is that a traditional seller of a home is typically a buyer as well. This explains why total active listing inventory data has been stable over the decades, with the exception of 2006-2011, when those forced distressed credit home sellers couldn’t buy.

As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. What I mean by a credit bust is that after the housing bubble burst in 2005 into 2006, we saw a massive increase in supply. Total inventory levels. NAR: Total Inventory levels 1.22

However, we haven’t had a credit sales boom like the one we saw from 2002-2005. Total Inventory had been growing from 2001-2005; total listings data in 2005 was at the higher historical range of 2.5 million listings. Today, we stand at 1,310,000 active listings. Newlistings are declining now.

The lack of sellers is also a demand problem and what we saw after June of 2022 is that sellers called it quits earlier and faster in the year than usual, resulting in total existing home sales totaling 5,030,000 to end 2022. During that period, we saw newlisting data decline.

However, what is different this year from 2023 is that we have more sellers that will be buyers. As you can see in our newlisting data, we are showing growth. Of course, the housing market didn’t have the credit sales boom it had from 2002-2005, but it lacked inventory.

Weekly housing inventory Since newlisting data was trending at all-time lows in 2023, some feared we wouldn’t see the typical spring inventory increase. After the last few weeks , we can put that fear aside: we are finally getting the seasonal increase in active listing. didn’t go into recession until 2008.

Seasonal impacts are the norm with housing, and newlisting data is negative 6% year to date. We saw newlisting data decline when rates got to 6.25% the first time. A traditional seller is primarily a homebuyer, so not only do we lose the inventory for sale when this happens, but we also lose a buyer.

Yes, we found the seasonal bottom for housing inventory on April 14, but this year’s rise in active listings has been tepid at best. Here’s a quick rundown of the last week: Total active listings grew 662 weekly, and newlisting data is still trending at all-time lows. This doesn’t appear to be the case for 2023.

If sales are working from an elevated number, like what we saw from 2003-2005, it’s a different subject altogether. Homebuilders’ for-sale inventory and months’ supply The seasonally-adjusted estimate of new houses for sale at the end of January was 439,000. To get more inventory you need more Americans to list their homes.

If we are trending below 4 million — a possibility with newlisting data trending at all-time lows — then we have much weaker demand than people think. million before we saw the massive stress spike in supply from 2005 to 2007. We have a workable range for 2023 sales in the existing home sales market between 4 million and 4.6

Homebuilders are efficient sellers of homes because it’s like a commodity to them; they don’t have to look for shelter after they sell or have a 3% mortgage rate they have to give up after they sell. Just look at the chart below and how bad credit looked from 2005 to 2008, then the job loss recession happened. months and above.

However, weeks after that call, the newlisting data started to decline noticeably, which makes that call much harder to happen in 2023. However, I acknowledge that the housing dynamics have changed a lot since that forecast in June as newlisting data declined. million in 2023. million for 2023. Housing recession.

Sales were down in all three categories: Single family sales down by 22.1%: 40,828 in 2023 from 52,397 in 2022 Condo sales down by 18.7%: 19,199 in 2023 from 23,616 in 2022 Multi-family sales down by 28.5%: 5,739 in 2023 from 8,031 in 2022 Below is a graph that illustrates home sales per year since 2005. from 2022 when there were 75,173.

Many sellers were reluctant to list due to low pre-pandemic mortgage rates, but increased activity emerged from necessity and life changes , with competitive pricing becoming essential. The market began as a sellers market but shifted toward buyers with a burst of activity later in the year, and a rebound is expected in 2025.

Inventory of homes listed reached a record low by July of 2023 , and mortgage rates increased dramatically, diminishing buyer affordability. Many sellers are holding the line, and buyers continue to face competition. If a home has been listed and isn’t selling, that means the list price may be too high.

In 2024, the New Hampshire real estate market experienced slightly more sales and higher prices compared to 2023, aligning with national trends fueled by strong demand and constrained inventory. The market initially favored sellers at the start of the year but later saw a surge in activity that benefited buyers. increase in listings.

To get a real price crash, we would need to see a surge of housing inventory and distressed sellers. Where I disagree with Yun is this: We have more inventory because demand has been softer, and we have more newlistings this year compared to last. from August to a seasonally adjusted annual rate of 3.84 million in September.

Homes Listed – All of NH. Newlistings in 2021 followed a less treacherous trendline in 2021 than 2020 but still couldn’t quite keep up with pre-pandemic markets. decrease in the state of New Hampshire brought listings to 27,131 from 28,127 the previous year. Seller Resources. Cheshire moved 15.8%

Developed over time with the guidance of prominent designer John Saladino initially and then later with the legendary architect Peter Marino who reimagined the structure back in 2005 and oversaw a 10,000 square foot addition to the house. We are seeing more newlistings across the country, and it’s something we’re also seeing locally.

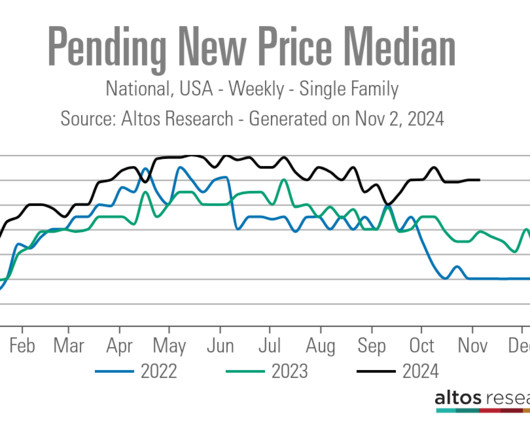

NAR total inventory since 1982: I prefer the Altos Research weekly single-family data to the NAR data because it gives us a fresh look at not only active listing data but newlisting data. The Altos Research newlisting data is essential in tracking the supply aspect of housing, which is why I include it as part of the Tracker.

As you can see in the chart below, the credit markets broke in 2005, 2006, 2007 and 2008, and then the job-loss recession of 2008 started, which made things much worse. The newlistings data we track with Altos Research is trending at the lowest levels ever during the past few years, while back then it was running at accelerated levels.

There were many years of housing data in the early to mid-1980s and mid to late 1990s, and even from 2000 to 2005, where we have seen rising inventory and sales. Newlistings data had a slight increase this week from 60,066 to 60,819. You can have rising inventory, increasing sales and rising prices.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content