This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

High mortgage rates, low inventory and sky-high prices resulted in historically low sales at a time when agents are already wrestling with the changes related to the $418 million antitrust settlement signed by the National Association of Realtors (NAR). In the current climate, homebuilders have advantages over existing-home sellers.

The housing market got some much needed relief in the fall when mortgage rates began to drop, but it was short lived. Despite two interest rate cuts by the Federal Reserve, mortgage rates rose again and remain stubbornly high. Its a symptom of a market thats transitioning away from sellers.

There’s a showdown at the housing market corral between homebuyers and sellers. To top it all off, we started 2022 at all-time lows, forcing bidding action everywhere until mortgage rates rose. And we aren’t talking about your grandfather’s mortgage rates rising; we went from 2.5% Image by Brandon Johnson/HW Media.).

Since the weaker CPI data was released in November, bond yields and mortgage rates have been heading lower. The question then was: What would lower mortgage rates do to this data? However, mortgage rates have fallen more than 1% since the recent highs, so it’s time to look at the data to explain how to interpret it.

The housing sector — especially real estate and mortgage — has seen significant layoffs , while the general economy will create more than 4 million jobs in 2022. Then we had the biggest mortgage rate shock in recent history and yet even with that, we will have over 5 million total home sales this year. Production falls. Home sales.

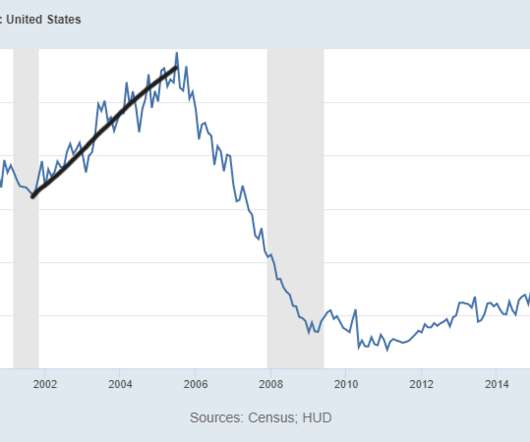

After 2010, qualified mortgage laws were in place, meaning everyone getting a mortgage has to be able to repay the loan. You can see the drastic change this made in the Mortgage Bankers Association Credit Availability index , below, which skyrocketed in 2005 and 2006 before an epic collapse in 2008.

But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. In the summer of 2020, I talked about how the housing market would change, but it needed the 10-year yield to break over 1.94%, which roughly means 4% plus mortgage rates.

We finally got mortgage rates to rise, and for people like me who have been concerned about how unhealthy the housing market was last year — and it got a lot worse this year — it’s a blessing that was much needed. million line in the sand has been this: Home prices grow above that 23% level: check Mortgage rates spike higher: check.

. “The principal factor was the rapid increase in mortgage rates, which hurt housing affordability and reduced incentives for homeowners to list their homes. ” One of the housing economic realities that I have been trying to stress this year is that a traditional seller of a home is typically a buyer as well.

As the 10-year yield broke above 1.94% and mortgage rates rose, we saw the impact on housing data. That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. Credit stress was evident from 2005 to 2008. It’s an excellent time to discuss housing inventory. What is going on here?

And the peak in existing home sales was 2005 when you had around 7 million transactions.” If this came to pass as Whitney predicts, then some seniors may not have as much of a need for a product like a traditional reverse mortgage through the Federal Housing Administration (FHA)’s Home Equity Conversion Mortgage (HECM) program.

We’ve all been wondering what 5% plus mortgage rates would do to the hot housing market, and now we’ve got that and a bag of chips. As a result, I’ve been rooting for mortgage rates to rise to create a balancing impact on this housing market. 2018 was the last time mortgage rates got to 5%, and sales trended from 5.72

Buying a house was obtainable only for the haves in 2023 as home prices and mortgage rates soared. Homebuyers’ median household income increased by $19,000 this year from 2022, reaching $107,000, according to the National Association of Realtors ’ 2023 Profile of Homebuyers and Sellers. Meanwhile, in September, one-third of U.S.

We had a period this summer when mortgage rates moved from 6.25% back down to 5% and some of the new home sales activity picked up. million level we saw in 2005. However, it does show that the builders are in a much better spot to deal with their massive supply, compared to the 2005-2008 period. months of supply, 5.36

Imagine if mortgage rates didn’t rise this year. We are still showing double-digit home-price growth trends in the recent data as it takes time for higher mortgage rates to really increase supply back to normal levels. Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005.

You can see why I have been on team higher mortgage rates for some time now because we don’t have any other way to get off this madness. You can’t have the best housing demographics ever, with the lowest mortgage rates and the best loan profiles with falling inventory for eight years, and not be concerned about this during 2020-2024.

Tuesday’s new home sales report missed expectations and had negative revisions, which isn’t surprising given this sector of our economy simply can’t handle higher mortgage rates. can’t have a credit sales boom like we saw from 2002-2005. Over the years, I have tried to emphasize that the housing market in the U.S.

Consolidation in the mortgage industry is likely in 2022, analysts and lending executives said. Justin Woodward has experienced the best and the worst of the mortgage industry in only 18 months. “I had not done first mortgage lending before, but I was familiar with the basics of real estate lending.

9 up until the early part of February as mortgage rates fell from 7.37% to 5.99%. To combat higher mortgage rates, builders have been cutting prices and buying down rates to move product. If sales are working from an elevated number, like what we saw from 2003-2005, it’s a different subject altogether.

The lack of sellers is also a demand problem and what we saw after June of 2022 is that sellers called it quits earlier and faster in the year than usual, resulting in total existing home sales totaling 5,030,000 to end 2022. During that period, we saw new listing data decline. Also, this is what the Federal Reserve wants.

They’re effective sellers and don’t want to create a backlog of completed units for sale because that would ruin their business model. This means new homes — with all the bells and whistles — can peel some buyers from the existing home sales market, especially if they pay down mortgage rates. Now on to the report.

A few months ago, I wrote that the new home sales sector is at risk because of rising mortgage rates. I know some people don’t agree with me on this, but the price gains in both the existing home and new home sales sector show that homebuilders and sellers had too much pricing power and needed to be checked.

Existing home sales When mortgage rates started to rise earlier this year, existing home sales trended lower. However, what is different this year from 2023 is that we have more sellers that will be buyers. However, if mortgage rates went lower and stayed lower, everyone would be selling more homes today.

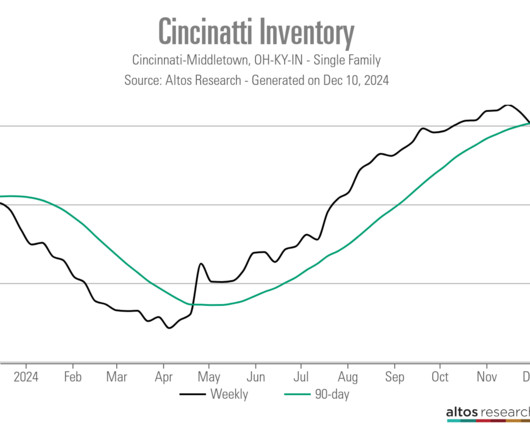

However, we haven’t had a credit sales boom like the one we saw from 2002-2005. Total Inventory had been growing from 2001-2005; total listings data in 2005 was at the higher historical range of 2.5 However, not to the degree we saw from 2005-2008. million listings. Today, we stand at 1,310,000 active listings.

New home sales missed estimates today but had three months of positive revisions, which continues the story of the builders managing the higher mortgage rate environment. This is why I have called them efficient home sellers. However, higher mortgage rates make it harder and harder to pull some of those deals off.

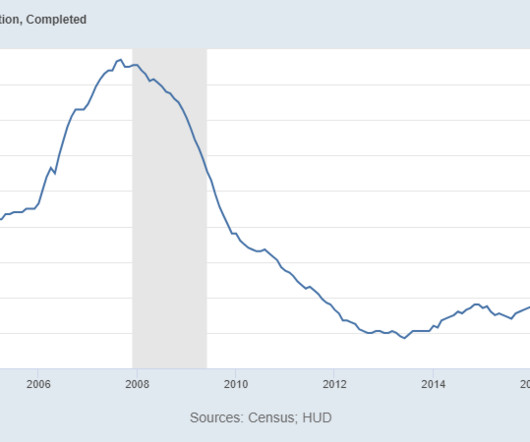

If you look at the monthly supply for new homes from 1996 to 2005, it was always lower than what we saw from 2008 to 2019. Then in 2018, when mortgage rates got to 5%, we had a supply shock for the builders, which in essence stalled out construction for 30 months.

The housing market didn’t crash at all, in fact, more Americans bought homes with mortgages in 2021 than in 2020. mortgage rates, so on the mortgage rate side of the equation, it’s never been better. Home sellers strive to get the highest price from the best offers and homebuilders have the pricing power over consumers.

The truth is that if mortgage rates fell below 5.875% and kept going lower, everyone’s housing predictions would need to be revised this year because the builders can sell their homes with lower mortgage rates. economy isn’t in recession today, and mortgage rates have risen almost 1% from the recent lows.

During the 2007-10 mortgage default meltdown, appraisals were a target of complaints and allegations by lenders, the GSEs, some state appraisal boards, and a few unscrupulous entrepreneurs. Between 2002-2005 in many markets, the real estate market was scorching, much like it is today. We are seeing that as a profession again.

This problem is much different than the housing credit bubble of 2002-2005. Mortgage rates of 4%-5% weren’t doing the amount of demand destruction I thought they would. Mortgage rates closer to 6% for sure are driving bigger year-over-year decline data. housing market as savagely unhealthy. Jobs and incomes will be lost.

If you look at the monthly supply for new homes from 1996 to 2005, it was always lower than what we saw from 2008 to 2019. Then in 2018, when mortgage rates got to 5%, we had a supply shock for the builders, which in essence stalled out construction for 30 months.

As mortgage rates rose more and more, the October to January data was going to show big negative prints. A traditional seller is primarily a homebuyer, so not only do we lose the inventory for sale when this happens, but we also lose a buyer. NAR Research : Total existing-home sales decreased 5.9% million in October. months to 3.3

A housing bubble can generally be defined as an unsustainable period of house price growth generated by artificial demand, as was the case in the mid-2000s when demand surged because of wider access to mortgage financing. Tighter mortgage underwriting : Lending standards are much tighter today than during the mid-2000s.

As we can see in the chart below, it’s not like the new home sales market is booming at all; we aren’t anywhere near the top of sales in 2005 or in 2020. Imagine what the total housing market would look like if mortgage rates were at 5% today. percent (±15.2 percent)* above the revised February rate of 623,000, but is 3.4 percent (±12.7

Mortgage rates fell last week as we started the week at 6.65% and got as low as 6.49% to end the week at 6.55%. When you consider that a home seller is a natural homebuyer as well, you can see why the housing market broke after mortgage rates went on a roller coaster last year. This link explains the difference.

million before we saw the massive stress spike in supply from 2005 to 2007. One thing higher mortgage rates have done for sure is that home-price growth is cooling down noticeably since the big spike in rates. As we can see below, from 2000, total active housing inventory rose from 2 million to 2.5 economy.

One of the realities of COVID-19 has been the lag to build homes in a business that requires stable mortgage rates because of the traditional time to complete a home. Mortgage rates jumped from 3% to 7.375% this year. That would reverse the problem the housing market has had selling homes with mortgage rates above 7%.

The 2022 housing market was savagely unhealthy , with all-time lows in inventory leading to massive bidding wars and price spikes until the Fed put a screeching halt to all of it with rate hikes that resulted in the most significant one-year spike in mortgage rate history. Mortgage rates. So where does all that drama leave us for 2023?

The new home sales market is doing its slow and steady dance upward, which is typically the case as long as mortgage rates stay low. percent)* below the December 2020 estimate of 943,000 Slow and steady wins the race and the market that we had from 2002-2005 doesn’t exist today. From Census: New Home Sales Sales of new single?

The other focus should be where mortgage rates go; only a little happened last week. Mortgage rates, once again, didn’t move too much this last week; the bottom level range was 6.50%, while the top was 6.67%; we ended the week at 6.59%. The fear of not having an increase in inventory this spring should be put to rest.

It’s the same reason I have given for many years: the American bears who are typically housing crash addicts can’t read data correctly, and the mortgage purchase application data just proved my point once again. million level for three straight months, aligning with the better mortgage demand growth that we saw for four months.

That data shows how housing was still on pace to have another solid year before mortgage rates got over 5%. The housing world is much different at 5% plus mortgage rates versus the 3% mortgage world we had last year. The builders have pricing power and they — along with home sellers — have pushed it very hard since 2020.

However, since I had the possibility of the 10-year yield getting to 2.42% and 4% plus mortgage rates, I accounted for that in the range. For now, it’s ok, but this is one sector that people need to keep their eye out on because it’s tied to mortgage buyers more than the existing home sales market.

As of late, Home Owners Association (HOA) dues often rival or exceed mortgage payments, then factor in higher interest rates, and taxesthough some potential tax relief may be on the horizon-and condo ownership is almost out of reach for some. This happens because of pricing. This is why the number of days of market rises.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content