This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

High mortgage rates, low inventory and sky-high prices resulted in historically low sales at a time when agents are already wrestling with the changes related to the $418 million antitrust settlement signed by the National Association of Realtors (NAR). This is particularly true for builders with in-house mortgage businesses.

trillion in cash-out refis in 2021, up 20% compared to the prior year, the highest volume since 2005. Despite the withdrawal, tappable equity available to homeowners with a mortgage grew by $446 billion in the fourth quarter. in 2021, highest level since 2005 appeared first on HousingWire. The post Cash-out refis reach $1.2T

The March gain is also the largest since December 2005 and is one of the largest in the index’s 30-year history, said Craig Lazzara, managing director and global head of index investment strategy at S&P DJI. ” Mortgage rates continue to hover around 3%, keeping prospective homebuyers interested, Speakman said.

Lack of inventory coupled with pent-up demand for homes – plus low mortgage rates – has resulted in home price appreciation surging to new historical highs.

The Mortgage Bankers Association on Tuesday released revised estimates for the third and fourth quarter of 2020 as well as predicting record purchase volume for 2021. The rebounding economy is also likely to mean higher mortgage rates , with the MBA forecasting 2.9% trillion in 2005 — but sees refinances decreasing to $971 billion.

Tuesday’s housing starts report clearly shows that homebuilders are going to be done with single-family construction until mortgage rates fall. Currently, we are in a much different housing recession than what we had from 2005-2011. The credit cycle looks much different now than the build-up from 2002-2005.

As recession talk becomes more prevalent, some people are concerned that mortgage credit lending will get much tighter. One of the biggest reasons home sales crashed from their peak in 2005 was that the credit available to facilitate that boom in lending simply collapsed. The short (and long) answer is no, not a chance.

One of the most unloved American economic success stories has been how spectacular American households with mortgage debt look today. We can see a slow and steady positive downtrend in stressed financial data, unlike in the 2005-2008 period where people filed for bankruptcies and foreclosures without a job loss recession.

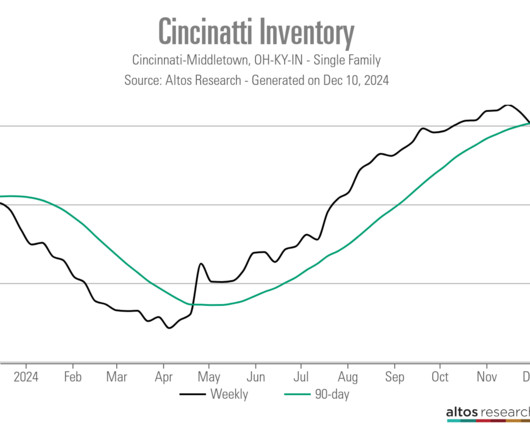

The housing market got some much needed relief in the fall when mortgage rates began to drop, but it was short lived. Despite two interest rate cuts by the Federal Reserve, mortgage rates rose again and remain stubbornly high. Its unpredictable, said Teena Jackson, a Redfin agent in Cincinnati.

From 1998 to 2006, according to Freddie Mac , the median annual mortgage rate was 6.45%. Mortgage rates today are not much higher than they were then. One challenging historical fact is that while mortgage rates fell from 13.24% in 1983 to 7.81% in 1996, it took that long for housing sales to reach the levels they did in 1978 to 1979.

Ginnie Mae , the government-owned corporation that securitizes loans backed by the Veterans Administration and the Federal Housing Administration , said it won’t accept adjustable-rate mortgages benchmarked to the London Interbank Offer Rate, or LIBOR, starting in January. For regular ARMs, the cut-off date is Jan.

The average 30-year fixed-rate mortgage fell four basis points from the week prior to 2.98%, according to data released Thursday by Freddie Mac ‘s PMMS. Within the past almost three months, mortgage rates have only peaked above 3% one time. More recently, however, mortgage applications dipped 6.9%

Swiss bank UBS Group AG has decided to sell Credit Suisse ’s mortgage servicing company, Select Portfolio Servicing (SPS), to a group of investors led by Sixth Street , HousingWire has learned. Banks have reduced their exposure to mortgage servicing rights (MSRs) due to expected higher capital requirements and risks.

Banks moved to ease lending standards for most mortgage loan products during the second quarter, according to a loan officer opinion survey published this week by the Federal Reserve Board. Banks also reported stronger demand for residential real estate loans over the second quarter, with significant demand for QM and non-QM jumbo mortgages.

Since the weaker CPI data was released in November, bond yields and mortgage rates have been heading lower. The question then was: What would lower mortgage rates do to this data? However, mortgage rates have fallen more than 1% since the recent highs, so it’s time to look at the data to explain how to interpret it.

The housing sector — especially real estate and mortgage — has seen significant layoffs , while the general economy will create more than 4 million jobs in 2022. Then we had the biggest mortgage rate shock in recent history and yet even with that, we will have over 5 million total home sales this year. Production falls. Home sales.

The average 30-year fixed-rate mortgage declined slightly to 2.86% for the week ending in August 19, according to mortgage rates data released Thursday by Freddie Mac ‘s PMMS. The week prior, mortgage rates rose to 2.87% , after six consecutive weeks of mortgage rate declines. Last week, mortgage applications decreased 3.9%

9, when mortgage rates started to fall from 7.37% to 5.99%. In 2022, it was all about affordability as mortgage rates had a historical rise. Even though mortgage rates were falling in November and December, positive purchase application data takes 30-90 days to hit the sales data. Year-over-year, sales fell 22.6% (down from 5.92

However, the demand curve of what we have in housing too doesn’t resemble the speculation demand curve of what we saw from 2002-to 2005. So the type of boom and bust we would need to see to reflect bubble speculation demand isn’t in this market like we saw from 2002-to 2005. Have more questions for Logan?

Mortgage applications decreased for the fourth straight week – this time down 2.2%, according to the latest report from the Mortgage Bankers Association. Record-low inventory is pushing home-price growth at double the rate from a year ago, and even above the 10% growth rates seen in 2005,” Kan said. from the week prior.

mortgage rate remained essentially unchanged last week, rising by just one basis point to 3.18%, according to Freddie Mac’s Primary Mortgage Market Survey. Overall, homebuyer demand slipped from 25% above pre-COVID levels at the start of the year, when mortgage rates hit record lows, to 8% above pre-COVID levels recently. “We

UMortgage , a growing nationwide mortgage platform, announced last week the addition of MC Mortgage Group to its network. MC Mortgage Group, a mortgage brokerage based in Wilmington, North Carolina, serves homebuyers across North and South Carolina.

The data, from Black Knight’s “Mortgage Monitor” report , shows that rate lock activity in the first half of October was up 4% from September, with purchase locks up 6% and refinance locks up 3%. million home owners still meet broad-based underwriting criteria to shave about 75 bps off their mortgage through a refinancing.

Quite the opposite: In that cycle we had the weakest housing recovery ever, even with the lowest mortgage rates during the longest economic expansion ever. There are several important reasons why the market today is materially different then the bubble-forming market of 2005. Speculation demand.

The mortgage world is fast-paced and constantly evolving, driven by shifts in laws and economic conditions. Both lenders and borrowers need to grasp these changes to skillfully move through the maze of mortgage regulations. Adapting to changes Success in the mortgage industry hinges on your ability to adapt.

One of the unsung heroes of the most prolonged economic and job expansion ever recorded in history was the passing of the 2005 Bankruptcy Reform Act and the 2010 qualified mortgage rule under Dodd-Frank. As we can see below, the bankruptcy levels were extremely high before the bankruptcy law was passed in 2005.

announced the acquisition of LoanLogics , a digital mortgage solutions provider and fellow Jacksonville-based company. The LoanLogics platform provides technology automation for mortgage document processing and data-driven audit software that improves efficiency, enhances transparency, streamlines commerce, and reduces risk.

One of the main reasons for that fear was that housing credit was about to get tight, meaning fewer people could buy homes with mortgages. It means certain mortgage products might not be offered, FICO score requirements might be raised, and it can mean pricing for certain loans goes up to account for the risk.

Regina Lowrie, the first female chair of the Mortgage Bankers Association , died suddenly on Jan. With nearly 40 years of experience in the real estate finance industry, Lowrie is widely known for making history in 2005 as the first female elected chair of the MBA. She was 68. billion with revenues of more than $100 million.

As you can see below, during the housing bubble years, housing starts, permits, sales, credit, prices and housing completions moved together in 2005 to form the peak of the housing bubble. The new home sales market gets hit harder by higher mortgage rates than the existing home market. Traditionally, mortgage rates have to head lower.

But its exacerbated by the rapid rise in mortgage rates over the last three years. Many California homeowners are locked in not just by low property taxes, but by low mortgage rates. Mortgage rates hovered between 3% and 5% from 2010 to the start of 2022, dropping to a record low of under 3% at the height of the pandemic moving frenzy.

The fact is that the FHFA is applying a form of risk-based pricing to the exercise based on their expectations of long-term performance of mortgages going forward. 80% LTVs (no mortgage insurance required) and 80.01-85% 85% LTVs (with mortgage insurance) by credit score. Therein lies some of the confusion.

Special purpose acquisition companies’ appetite for real estate and mortgage businesses apparently isn’t dead yet , despite recent problems involving Better.com that pushed a merger with Aurora Acquisitions Corp. trillion and mortgage originations to $3.8 to next year, if at all. trillion in 2020 in the United States.

We had some good news this week for the housing market : purchase application data is up , the builder’s confidence index rose to beat estimates, and the 10-year yield and mortgage rates have fallen. This is bullish for America and for mortgage rates to head lower. There are 943,000 apartments currently under construction.

What is the best news for mortgage rates long-term? More supply of apartments coming on line will be good news for mortgage rates going forward. As you can see in the chart below, this looks nothing like the housing peak in 2005 and the crash toward 2008. This is key for mortgage rates looking out for years to come.

However, the sting of higher mortgage rates is hitting the single-family construction data, and the real story is that the housing completion data, which has been bad for a long time, is still terrible. We simply cannot finish homes in America promptly, and now that mortgage rates are over 5%, some buyers won’t be able to purchase a home.

housing credit looks very different than in 2005, 2006, 2007 or 2008. Bankruptcies and foreclosures After 2010, the qualified mortgage laws came into play and all the exotic loan debt structures in the system, especially in the run-up in demand from 2002 to 2005, disappeared. The truth is, U.S.

How is today’s housing starts data , which beat expectations, good for mortgage rates ? Regarding mortgage rates and bonds, since the banking crisis started with a run on Silicon Valley bank last week , bond yields have been heading lower and are now testing my Gandalf line in the sand of 3.42%. That isn’t happening right now.

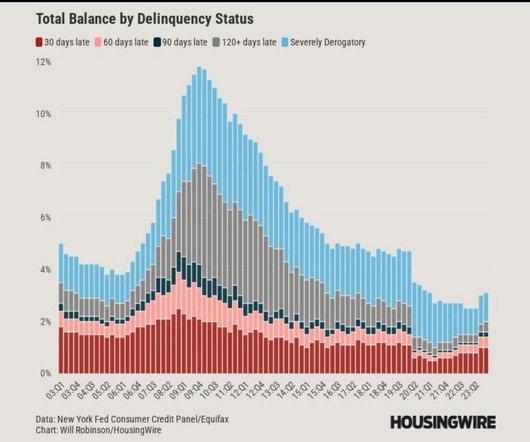

of homes with mortgages were underwater, totaling just over 11 million homes. However, the situation has significantly improved since then, thanks to the Qualified Mortgage rule (QM) that was implemented in 2010. of homes that have a mortgage. of homes that have a mortgage. What a difference a cycle makes, right?

After 2010, qualified mortgage laws were in place, meaning everyone getting a mortgage has to be able to repay the loan. You can see the drastic change this made in the Mortgage Bankers Association Credit Availability index , below, which skyrocketed in 2005 and 2006 before an epic collapse in 2008.

But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. In the summer of 2020, I talked about how the housing market would change, but it needed the 10-year yield to break over 1.94%, which roughly means 4% plus mortgage rates.

We finally got mortgage rates to rise, and for people like me who have been concerned about how unhealthy the housing market was last year — and it got a lot worse this year — it’s a blessing that was much needed. million line in the sand has been this: Home prices grow above that 23% level: check Mortgage rates spike higher: check.

Home prices were growing at an unsustainable level from 2002-2005, leading to some excess risk-taking on inadequate loan debt structures. In the 2020 market, on the other hand, refinances were not driven just by an increase in equity but lower mortgage rates. The rest of this content is for HW+ members. Already a member?

As we enter the second quarter of 2021, it’s time for the mortgage industry to reflect on the past 12 months and think about how to plan for the same period ahead. Low mortgage rates, driven by quantitative easing by the Federal Reserve helped fuel a boom in both mortgage refinancing and purchases, making 2020 the second-best year in U.S.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content