This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As recession talk becomes more prevalent, some people are concerned that mortgage credit lending will get much tighter. One of the biggest reasons home sales crashed from their peak in 2005 was that the credit available to facilitate that boom in lending simply collapsed. The short (and long) answer is no, not a chance.

One of the most unloved American economic success stories has been how spectacular American households with mortgage debt look today. Post-2010, lending standards in America became normal again, and while I still believe they’re very liberal, they’re sane. The most important factor is that debt structures are vanilla. Already a member?

As we enter the second quarter of 2021, it’s time for the mortgage industry to reflect on the past 12 months and think about how to plan for the same period ahead. Low mortgage rates, driven by quantitative easing by the Federal Reserve helped fuel a boom in both mortgage refinancing and purchases, making 2020 the second-best year in U.S.

Banks moved to ease lending standards for most mortgage loan products during the second quarter, according to a loan officer opinion survey published this week by the Federal Reserve Board. The post Mortgage lenders are loosening standards on jumbos appeared first on HousingWire.

A former Quicken Loans executive, Booth has over 15 years of experience working in state and federal government bodies, focusing on transforming the mortgage industry through technology. Planet Home Lending has promoted four people to vice president positions, supporting the company’s continual growth.

The mortgage world is fast-paced and constantly evolving, driven by shifts in laws and economic conditions. Both lenders and borrowers need to grasp these changes to skillfully move through the maze of mortgage regulations. Adapting to changes Success in the mortgage industry hinges on your ability to adapt.

The data, from Black Knight’s “Mortgage Monitor” report , shows that rate lock activity in the first half of October was up 4% from September, with purchase locks up 6% and refinance locks up 3%. “Indeed, total lending in 2020 is well on its way to easily eclipse the $4 trillion mark for the first time in history.”.

From 1998 to 2006, according to Freddie Mac , the median annual mortgage rate was 6.45%. Mortgage rates today are not much higher than they were then. One challenging historical fact is that while mortgage rates fell from 13.24% in 1983 to 7.81% in 1996, it took that long for housing sales to reach the levels they did in 1978 to 1979.

Mortgage applications decreased for the fourth straight week – this time down 2.2%, according to the latest report from the Mortgage Bankers Association. Record-low inventory is pushing home-price growth at double the rate from a year ago, and even above the 10% growth rates seen in 2005,” Kan said. from the week prior.

One of the unsung heroes of the most prolonged economic and job expansion ever recorded in history was the passing of the 2005 Bankruptcy Reform Act and the 2010 qualified mortgage rule under Dodd-Frank. Both these laws paved the way for more responsible lending and a more responsible consumer. Today, we are at 1.25

The housing sector — especially real estate and mortgage — has seen significant layoffs , while the general economy will create more than 4 million jobs in 2022. Then we had the biggest mortgage rate shock in recent history and yet even with that, we will have over 5 million total home sales this year. Production falls. Home sales.

First, the refinance boom’s main driver in the 2000s was unhealthy because of the marketplace’s speculative unhealthy lending standards. Home prices were growing at an unsustainable level from 2002-2005, leading to some excess risk-taking on inadequate loan debt structures. The rest of this content is for HW+ members. Already a member?

Consolidation in the mortgage industry is likely in 2022, analysts and lending executives said. Justin Woodward has experienced the best and the worst of the mortgage industry in only 18 months. “I had not done first mortgagelending before, but I was familiar with the basics of real estate lending.

One of the main reasons for that fear was that housing credit was about to get tight, meaning fewer people could buy homes with mortgages. It means certain mortgage products might not be offered, FICO score requirements might be raised, and it can mean pricing for certain loans goes up to account for the risk.

of homes with mortgages were underwater, totaling just over 11 million homes. However, the situation has significantly improved since then, thanks to the Qualified Mortgage rule (QM) that was implemented in 2010. of homes that have a mortgage. of homes that have a mortgage. What a difference a cycle makes, right?

” The notion that educated homeowners with positive cash flow — who aren’t showing any stress in making their low payments thanks to historically low mortgage rates — would sell at 50%, 60% to 70% off current values and go back to renting, doesn’t seem realistic. Home prices have grown 108.3% Our evidence points to abnormal U.S.

Guaranteed Rate made two significant executive appointments, the Chicago -based mortgage lender announced on Monday. CJ Rose was promoted to the role of executive vice president of growth and acquisition, while Chris Hutchens was hired as producing area manager for North Carolina and senior vice president of mortgagelending.

We finally got mortgage rates to rise, and for people like me who have been concerned about how unhealthy the housing market was last year — and it got a lot worse this year — it’s a blessing that was much needed. million line in the sand has been this: Home prices grow above that 23% level: check Mortgage rates spike higher: check.

That belief, however, assumes that one does not understand the two main drivers of housing: demographics and mortgage rates. As it happens, these fabulous demographics are accompanied by the lowest mortgage rates ever recorded in history. All that other stuff, my friends, is just stamp collecting.

Encompass Lending Group , a subsidiary of real-estate services platform Fathom Holdings, has acquired Austin, Texas-based Elite Financing Group, the company announced Thursday. Elite brings local market expertise which should help strengthen Fathom’s mortgage business in Texas, he added. Terms of the deal were not disclosed.

To say that mortgage lenders are facing challenging times would be a considerable understatement. The last time that the rate reached 3.25% was in 2005 — and we all know how that story unfolded. The substantial increases this year present challenges in the mortgage sector, as the note rates produced can become illiquid if not hedged.

A reverse mortgage loan has first-priority status in a Pennsylvania foreclosure dispute, after initially being rejected by the trial court according to court documents reviewed by HousingWire s Reverse Mortgage Daily (RMD), and an analysis by attorneys at law firm Wilentz, Goldman & Spitzer, P.A. with a traditional mortgage.

The creation of the Home Mortgage Disclosure Act (HMDA) in 1975 required lenders to track and report loan-level data to the Consumer Financial Protection Bureau (CFPB) in an effort to reduce redlining, and finally, in 1988, amendments made to the Fair Housing Act of 1968 deemed it illegal. Per Redfin, 58.1% and Chicago.

Due to the loosey-goosey lending standards of the time, many of these delinquent loan holders had little to negative equity. Mortgage demand, too, is at an 11-year high. Housing data started to soften in 2005 after an overheated market. And third — mortgage rates are very low.

Mortgage industry participants may disagree a great deal on several different topics. However, I expect that you would find no argument with the following statement: Mortgagelending is a highly competitive business. Make no mistake: the mortgage market has become more competitive.

The new home sales market is doing well as it really benefits from lower mortgage rates. Good housing demographics, housing tenure at 10 years and low mortgage rates are a perfect recipe for unhealthy home-price growth. Mortgage rates are one of the primary drivers of demand. It is not out of the question that we can get to 6.2

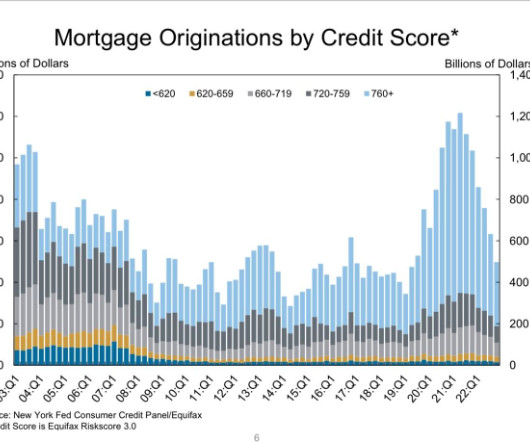

Well, it isn’t 2008, but this type of loan does have risk — and it’s the risk that is traditional among all late economic cycle lending in America when the loan requires low or no downpayment. As you can see below, we haven’t had the mortgage credit boom like we saw during the housing bubble years.

However, we haven’t had a credit sales boom like the one we saw from 2002-2005. Nor can we ever have a credit sales boom again with lending standards back to normal. Total Inventory had been growing from 2001-2005; total listings data in 2005 was at the higher historical range of 2.5 million listings.

In 2021, more than 90% of borrowers who closed a loan with fintech mortgage lender Neat Loans opted for a 30-year fixed-rate mortgage. The way ARMs work is lenders offer lower mortgage rates for the initial three, five, seven years. in 2005, the MBA said. The mortgage industry is different from 14 years ago.

Mozilo was a pioneer of the mortgage industry, though a deeply controversial figure. “Independent of how people outside of the industry may perceive this man, insiders know what an incredible force he was,” his son Eric Mozilo wrote in a LinkedIn post. Mozilo was president of the Mortgage Bankers Association (MBA) in 1991-1992.

From NAR : “December was another difficult month for buyers, who continue to face limited inventory and high mortgage rates ,” said NAR Chief Economist Lawrence Yun. However, expect sales to pick up again soon since mortgage rates have markedly declined after peaking late last year.” Also, this is what the Federal Reserve wants.

John Ashley: I’ve collaborated with PRMG since late 2005 and my background was network infrastructure and security. SW: What’s been the biggest change since you started at PRMG in 2005? Now every mortgage that’s recorded has a lender name and it’s got the originator’s NMLS number on every single loan.

At least two financial institutions brought back adjustable-rate mortgage (ARM) products this week amid surging mortgage rates and double-digit home price growth. this month, a 14-year high, compared to just 3% at the beginning of the year, according to the Mortgage Bankers Association. Applications for ARMs rose 10.8%

Cenlar FSB , the second-largest mortgage servicer and largest subservicer in the U.S., With over 25 years of experience in portfolio management, he brings to the role an extensive expertise in default mortgage servicing. Its client base includes banks, credit unions, and mortgage bankers. territories.

Retail lender Guild Mortgage announced Monday that Mary Ann McGarry is retiring from the CEO position in late June, remaining on the California-based lender’s board of directors after retirement. McGarry has also led the lender through several acquisitions of late, including Cherry Creek Mortgage , Inlanta Mortgage and Legacy Mortgage.

The lenders, Homepoint and United Wholesale Mortgage , say Fannie Mae and Freddie Mac started tacking on an extra 15 basis point charge for third-party originated, or wholesale, loans in mid-2021. A United Wholesale Mortgage spokesperson said the extra surcharge is part of an “old school 2007/2008 viewpoint that has become outdated.”.

A housing bubble can generally be defined as an unsustainable period of house price growth generated by artificial demand, as was the case in the mid-2000s when demand surged because of wider access to mortgage financing. Tighter mortgage underwriting : Lending standards are much tighter today than during the mid-2000s.

Recently, Intercontinental Exchange (ICE) announced a plan to acquire Black Knight in a reported $13 billion deal that, if approved by federal regulators, would certainly be one of the largest acquisitions ever in the mortgage technology space. Mortgage competition is critical. This is already a significant amount of data to own.

We had a lot of drama over the week between Federal Reserve meetings and banking stress, and mortgage rates and purchase applications both fell. Mortgage rates fell last week as we started the week at 6.73%, got as low as 6.43% to end the week at 6.5%. Mortgage rates fell to a low of 6.43% then ended the week at 6.5%.

Although the number of flips last year was the highest since at least 2005, ATTOM reports that “profit margins on the typical flip in 2022, which took an average of 5 ½ months to complete, slumped to just 26.9%.” A year ago, we were offering to lend 85% loan-to-cost or 90% loan-to-cost, and that’s down to like 75% loan-to-cost.

During the 2007-10 mortgage default meltdown, appraisals were a target of complaints and allegations by lenders, the GSEs, some state appraisal boards, and a few unscrupulous entrepreneurs. Between 2002-2005 in many markets, the real estate market was scorching, much like it is today. It is not our job to kill or make deals.

One of the reasons that I moved into the “team higher mortgage rate” camp is that what I saw in January, February, and March of this year was so unhealthy that I labeled the housing market savagely unhealthy. housing market, and we should never ease lending standards to try to facilitate demand. We had a credit boom.

Industry newsletters are reporting that mortgage lenders are tightening their belts as the cost to manufacture a loan peaks at a decade high of $9,299. mortgage loan originations, the largest annual volume on record since 2005. mortgage loan originations, the largest annual volume on record since 2005.

This roundtable offers the opportunity to engage in critical discussions that examine the current state of the single-family rental (SFR) industry, covering topics from lending strategies to property management, tech tools, build-for-rent demand, and much more. Set for Wednesday, September 25 from 1:30 p.m.-4:45

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content