This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

High mortgage rates, low inventory and sky-high prices resulted in historically low sales at a time when agents are already wrestling with the changes related to the $418 million antitrust settlement signed by the National Association of Realtors (NAR). In the current climate, homebuilders have advantages over existing-home sellers.

Housing credit channels directly impact housing inventory channels. Home prices escalated out of control after 2020 and when we look at why that happened, we can see that housing credit mattered more to inventory data than most people realize. This matters because inventory was already heading toward all-time lows before COVID-19.

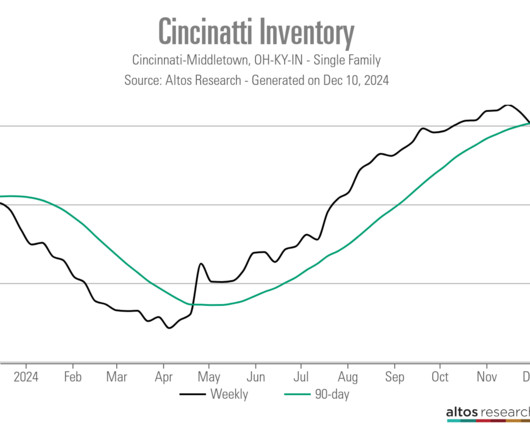

Ive been doing this since 2005 and I tell clients that Ive never seen a market like this, so we have to navigate it together. Its a symptom of a market thats transitioning away from sellers. According to data from Altos Research, for-sale inventory has risen from 1,864 on a 90-day rolling basis in May to 3,019 today.

There’s a showdown at the housing market corral between homebuyers and sellers. Inventory, which has been falling for years, broke to all-time lows in 2020. We didn’t have a seasonal push in inventory in 2020, and things worsened in 2021. Image by Brandon Johnson/HW Media.). million active listings, but at just 1.28

It’s an excellent time to discuss housing inventory. That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. How can housing inventory be so low today when it skyrocketed back in 2009? I don’t believe housing inventory below 1.52 What is going on here? housing market.

Given the current housing inventory crisis, it might surprise people to realize this: we built too many homes during the housing bubble years. Yes, but this is where my work is much different from other housing economists and why we need to think of inventory in a new, modern 21st-century mindset. Wait, what?

On Friday NAR reported that total housing inventory levels broke under 1 million in December, dropping to 970,00 units for a population of 330 million people. million in January down to about 4 million in December, We now have total inventory levels near all-time lows again. Unsold inventory sits at a 2.9-month months in Nov.

months’ worth of housing inventory in the U.S. NAR: Total housing inventory registered at the end of March was 980,000 units, up 1.0% Unsold inventory sits at a 2.6-month Total housing inventory, while up year over year, is still near all-time lows, and monthly supply is also up year over year. We only have 2.6

Both existing housing inventory and home prices have been rising together year over year, which might seem odd at first glance since existing home sales are trending near all-time lows. When you connect the dots, this is a short and simple answer to why housing inventory and home prices are both rising. Sales descended 2.8%

The spring housing market music is playing, and purchase application data and active listing inventory rose together last week. The fear of not having an increase in inventory this spring should be put to rest. Since 2020, the seasonal inventory bump has happened later than usual — not until March or April.

Given the current housing inventory crisis, it might surprise people to realize this: we built too many homes during the housing bubble years. Yes, but this is where my work is much different from other housing economists and why we need to think of inventory in a new, modern 21st-century mindset. Wait, what?

The National Association of Realtors (NAR) reported today on two trends in existing home sales that we have seen for many months now: sales are declining while total inventory data has fallen directly for the three straight months. Total housing inventory fell in this report, the third report in a row that shows total inventory has decreased.

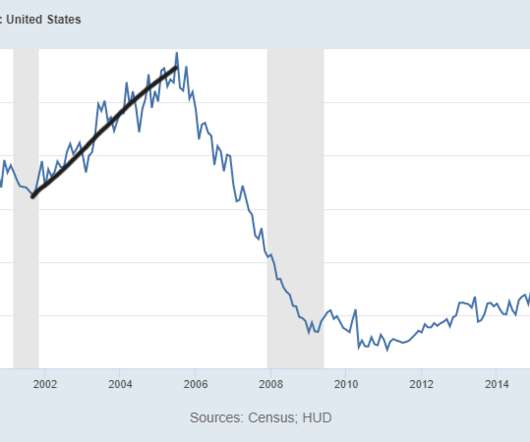

The housing market of 2002-2005 had four years of sales growth facilitated by credit. As we can see below, the purchase application data had four years of growth, peaking in 2005 and then collapsing. However, what isn’t identical is that we have not had a massive sales boom like we saw from 2002-2005. Housing inventory.

As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. What I mean by a credit bust is that after the housing bubble burst in 2005 into 2006, we saw a massive increase in supply. Total inventory levels. NAR: Total Inventory levels 1.22

But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. Inventory levels broke to all-time lows and thus created massive housing inflation quickly, which broke my model. Traditionally, inventory levels have been between 2 million to 2.5

In addition, this is the fourth straight month of inventory declining, while days on the market are growingl! Plus, available housing inventory remains near historic lows.” ” One of the housing economic realities that I have been trying to stress this year is that a traditional seller of a home is typically a buyer as well.

Inventory has broken to all-time lows, but it doesn’t look like the year-over-year data will be positive at all this year unless demand softens up. NAR Research : Unsold inventory sits at a 1.7-month NAR Research : Unsold inventory sits at a 1.7-month However, negative year-over-year inventory is not what we want to see.

Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. The housing market can’t replicate the type of massive credit expansion we saw from 2002-2005, so the price-growth story has more to do with inventory collapsing to all-time lows. For some time now, I have been focusing on that 1.52-1.93

While the growth rate is cooling monthly, we are still in a savagely unhhealthy housing market trying to get national inventory levels back to pre-COVID-19 levels. Housing inventory issue with no booming demand. However, we haven’t had a credit sales boom like the one we saw from 2002-2005. million listings.

Second, because of the downtrend in inventory since 2014 and the demand pick-up we will see in the years 2020-2024, we had a risk of home prices accelerating too much. As you can see below, the new home sales market from 2018-2022 doesn’t look like the housing market we had from 2002-2005. First, total home sales should be 6.2

I know some people don’t agree with me on this, but the price gains in both the existing home and new home sales sector show that homebuilders and sellers had too much pricing power and needed to be checked. As you can see, sales levels were never elevated like what we saw from 2002-2005. The only way this happens is by higher rates.

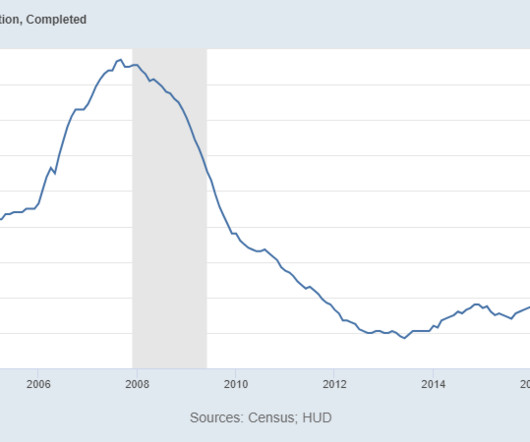

That’s right — for all the hype of massive housing inventory coming from the builders, today we sit here still trying to work back to pre-COVID-19 levels with just 76,000 completed homes ready to be moved. This is why I have called them efficient home sellers. But they still only have 76,000 completed units for sale today.

If sales are working from an elevated number, like what we saw from 2003-2005, it’s a different subject altogether. Homebuilders’ for-sale inventory and months’ supply The seasonally-adjusted estimate of new houses for sale at the end of January was 439,000. However, this isn’t how inventory grows in America.

million level we saw in 2005. However, it does show that the builders are in a much better spot to deal with their massive supply, compared to the 2005-2008 period. They are good at selling their inventory much quicker than existing home sellers, who might still be stingy on prices. months of supply, 5.36

Homebuyers’ median household income increased by $19,000 this year from 2022, reaching $107,000, according to the National Association of Realtors ’ 2023 Profile of Homebuyers and Sellers. The report is an annual survey of homebuyers and sellers who closed transactions between July 2022 and June 2023.

Looking at the housing market in the years 2020-2024, one risk i identified early on was that home prices could accelerate more in this period than we saw in the previous expansion if inventory channels broke to all-time lows. This problem is much different than the housing credit bubble of 2002-2005. NAR: Total Inventory.

They’re effective sellers and don’t want to create a backlog of completed units for sale because that would ruin their business model. Some people prefer something other than the current active existing inventory. Also, in the chart below, we can all agree it isn’t housing 2005 or housing 2008 with new home sales.

Yes, we found the seasonal bottom for housing inventory on April 14, but this year’s rise in active listings has been tepid at best. Weekly housing inventory Well, the best thing I can say for spring 2023 inventory is that we found the seasonal bottom a few weeks ago. This link explains the difference.

You know, the one that says we have too much inventory and millions of vacant homes in the U.S.? However, the people who say low inventory is fake news don’t realize that housing credit channels are very different from 2008, which has prevented total active listings from looking anything like 2008. percent (±15.2 percent (±12.7

The home-price growth from 2020 through 2022 has been so unhealthy that I’ve labeled this a savagely unhealthy housing market as inventory has once again collapsed on a year-over-year basis in 2022. Inventory is still showing negative year-over-year data. 2014 was the very last year total housing inventory grew in America.

can’t have a credit sales boom like we saw from 2002-2005. This means we won’t be working from record-breaking demand of high sales like we did at the peak of 2005. The builders are in a better position to manage their inventory glut than when they were working from a credit boom in 2005 that took new home sales up to 1.4

Last year we had monthly existing home sales collapse back to 2007 levels, except this time around, NAR has total inventory at 970,000 and not over 4 million. However, to my first point, the builders are lucky that total housing inventory is near all-time lows because this means their product holds more value. months and above.

The 2022 housing market was savagely unhealthy , with all-time lows in inventory leading to massive bidding wars and price spikes until the Fed put a screeching halt to all of it with rate hikes that resulted in the most significant one-year spike in mortgage rate history. Housing Inventory. Home price s. million in 2023.

As you can see below, we don’t have a booming credit housing market as we saw from 2002-2005; we have steady replacement buyer demand. More choices are better for homebuyers and sellers who need to buy a home typically as well. Seasonality has kicked in with inventory already, which is expected every year.

Not the best of news as we start year three of that time period with a solid possibility of new all-time lows in inventory this spring. Home sellers strive to get the highest price from the best offers and homebuilders have the pricing power over consumers. Well, it looks like my five-year growth model has been taken out in two years.

The one thing that has happened in 2022 that has been worse is that national inventory levels have worsened in 2022 to start the year. Inventory has been falling for years. Logan Mohtashami: People know that I haven’t been a big fan of this housing market since inventory levels broke under 1.52

The truth here that nobody wants to talk about is that we didn’t have a massive sales credit boom in housing from 2020-2021 like we saw from 2002-2005. We must remember that the builders don’t operate like existing home sellers; they treat their products as commodities. The monthly supply data did fall in this report to 8.6

The one thing housing has going for it now is that we don’t have the speculative booming demand as we saw from 2002 to 2005. The builders have pricing power and they — along with home sellers — have pushed it very hard since 2020. From Census: For Sale Inventory and Months’ Supply: The seasonally?adjusted

“Our goal is always to make our clients as appealing as possible to a seller to help increase their conversion of getting their offer accepted. trillion in cash-out refis in 2021, up 20% compared to the prior year, the highest volume since 2005. ” Others that leaned purchase in 2021 included depository U.S.

It kept inventory down, which propped up prices, but sales are down nearly 22%, and buyers are hungry. A year later, still no crash, which had more to do with the decrease in inventory than the decrease in sales. A lot of it had to do with anemic inventory. Average prices for closed sales increased by 3.4% Sales Decline by 21.7%

The 2021 Massachusetts Year in Review Housing Report breaks down average prices, sales, inventory, new active listings, and pending sales for 2021 compared to 2020 and illustrates what that means for the current market. Below is a graph that illustrates home sales per year since 2005. Inventory of Homes for Sale. That’s a 37.4%

In 2024, the Massachusetts real estate market saw slightly more sales and higher prices than 2023, reflecting national trends driven by strong demand and limited inventory. The market began as a sellers market but shifted toward buyers with a burst of activity later in the year, and a rebound is expected in 2025. Sales Rise by 1.5

The inventory of homes for sale and the number of homes being listed for sale were not nearly enough to satisfy the buyer demand. Even though the inventory of homes for sale at any given time all year stayed lower than ever, it did not decrease sales overall. 2021 Recap. Yes, you read that correctly, worse. It is a real problem.

Inventory of homes listed reached a record low by July of 2023 , and mortgage rates increased dramatically, diminishing buyer affordability. Furthermore, potential sellers with covid-era mortgage rates of around 3% weren’t listing because they’d have to give up that historic rate and trade it for one that is likely two times higher or more.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content