This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

has experienced two decades of slow but steady housing market growth, paired with inventory growth that has suffered through both the Great Recession and the pandemic. In 2023, total inventory hit 144 million housing units, a 16.7% increase from 2005. Americas Boomtowns: Which Cities Grew Housing Inventories the Fastest?

High mortgage rates, low inventory and sky-high prices resulted in historically low sales at a time when agents are already wrestling with the changes related to the $418 million antitrust settlement signed by the National Association of Realtors (NAR). of all transactions.

has focused on single-family and multifamily inventory growth to boost supply and affordability. But StorageCafe found that in 2023, most states overlooked one key solution to the affordability crisis: more inventory of “middle housing.” The report draws considerable attention to middle housing inventory growth.

Housing credit channels directly impact housing inventory channels. Home prices escalated out of control after 2020 and when we look at why that happened, we can see that housing credit mattered more to inventory data than most people realize. This matters because inventory was already heading toward all-time lows before COVID-19.

The March gain is also the largest since December 2005 and is one of the largest in the index’s 30-year history, said Craig Lazzara, managing director and global head of index investment strategy at S&P DJI. Higher material costs , a lack of inventory and labor continue to drive demand, pushing up home prices. Presented by: MCT.

It’s an excellent time to discuss housing inventory. That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. How can housing inventory be so low today when it skyrocketed back in 2009? I don’t believe housing inventory below 1.52 What is going on here? housing market.

Given the current housing inventory crisis, it might surprise people to realize this: we built too many homes during the housing bubble years. Yes, but this is where my work is much different from other housing economists and why we need to think of inventory in a new, modern 21st-century mindset. Wait, what?

Early in 2021, when I was talking about how people should worry about home prices overheating, I had a glimmer of hope that maybe toward the end of 2021 we would be spared another seasonal collapse of inventory. Inventory always falls in the fall and winter, but I hoped it wouldn’t be a repeat of 2020.

2 million , we could be at risk of housing inventory falling to such low levels that I would have to categorize this housing market as unhealthy. We can see that inventory falling to such low levels has created unhealthy home-price growth in both 2020 and 2021. Inventory fades in the fall and winter and picks up in summer and spring.

months’ worth of housing inventory in the U.S. NAR: Total housing inventory registered at the end of March was 980,000 units, up 1.0% Unsold inventory sits at a 2.6-month Total housing inventory, while up year over year, is still near all-time lows, and monthly supply is also up year over year. We only have 2.6

Both existing housing inventory and home prices have been rising together year over year, which might seem odd at first glance since existing home sales are trending near all-time lows. When you connect the dots, this is a short and simple answer to why housing inventory and home prices are both rising. Sales descended 2.8%

On Friday NAR reported that total housing inventory levels broke under 1 million in December, dropping to 970,00 units for a population of 330 million people. million in January down to about 4 million in December, We now have total inventory levels near all-time lows again. Unsold inventory sits at a 2.9-month months in Nov.

The spring housing market music is playing, and purchase application data and active listing inventory rose together last week. The fear of not having an increase in inventory this spring should be put to rest. Since 2020, the seasonal inventory bump has happened later than usual — not until March or April.

Prices are up sharply as housing inventory continues to plateau , leaving 40% fewer homes on the market compared to last year, according to a report prepared by Black Knight. Year-over-year, new listing volumes were down 16% in January and 21% in February — amounting to a 125,000 deficit in inventory compared to the same time in 2020.

If there’s one sector of the economy that benefits from the very low levels of total housing inventory , it’s the homebuilders , but for a reason you might not think. If national housing inventory were back to normal, we would have 2 to 2.5 That will be a much better environment for the builders. his represents a supply of 8.2

Just when I thought it was safe to say we were getting more traditional spring housing inventory , we hit a snag last week, as active inventory and new listings declined. Weekly housing inventory The numbers this week are unfortunate: inventory should be growing like it does at this time every year.

Homes remain much more affordable in 2021 than they were during the home price runup in 2005 and 2006, but the seven-month trend in deteriorating affordability is starting to gradually slow demand. Renovated Inventory to the Rescue. Top Markets for Renovated Inventory. Homebuyers Losing Heart. Home sales in August decreased 1.5%

Given the current housing inventory crisis, it might surprise people to realize this: we built too many homes during the housing bubble years. Yes, but this is where my work is much different from other housing economists and why we need to think of inventory in a new, modern 21st-century mindset. Wait, what?

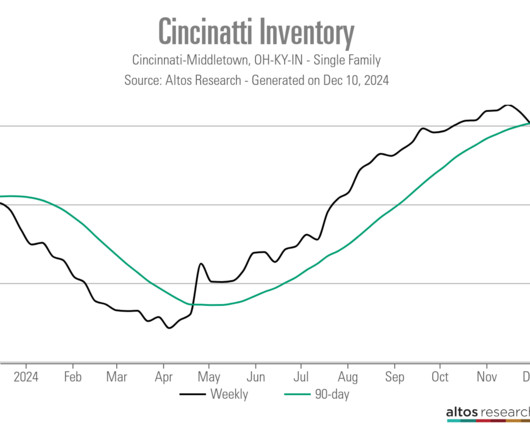

Ive been doing this since 2005 and I tell clients that Ive never seen a market like this, so we have to navigate it together. According to data from Altos Research, for-sale inventory has risen from 1,864 on a 90-day rolling basis in May to 3,019 today. Its unpredictable, said Teena Jackson, a Redfin agent in Cincinnati.

Lack of inventory coupled with pent-up demand for homes – plus low mortgage rates – has resulted in home price appreciation surging to new historical highs. home prices continued to surge in March, rising 1.5% on an adjusted basis compared with February and jumping a whopping 13.2%

The National Association of Realtors (NAR) reported today on two trends in existing home sales that we have seen for many months now: sales are declining while total inventory data has fallen directly for the three straight months. Total housing inventory fell in this report, the third report in a row that shows total inventory has decreased.

I always try to focus people on the total inventory data until we get inventory back into a range of 1.52-1.93 HousingWire: To add to that, since housing is in an inventory shortage, the market has changed, so the good news is inventory is growing. What levels should we be hoping for? Then this happened. Ghost Supply 2.2

The housing market of 2002-2005 had four years of sales growth facilitated by credit. As we can see below, the purchase application data had four years of growth, peaking in 2005 and then collapsing. However, what isn’t identical is that we have not had a massive sales boom like we saw from 2002-2005. Housing inventory.

One of the unsung heroes of the most prolonged economic and job expansion ever recorded in history was the passing of the 2005 Bankruptcy Reform Act and the 2010 qualified mortgage rule under Dodd-Frank. As we can see below, the bankruptcy levels were extremely high before the bankruptcy law was passed in 2005. Today, we are at 1.25

But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. Inventory levels broke to all-time lows and thus created massive housing inflation quickly, which broke my model. Traditionally, inventory levels have been between 2 million to 2.5

Its unclear how effective Prop 19 has been at freeing up housing inventory. Tight inventory only pushes home prices up more, and adds to the generational homeownership divide. years in 2005, then tenure gradually increased over the next 15 years. The typical homeowner stayed put for 6.5

While the growth rate is cooling monthly, we are still in a savagely unhhealthy housing market trying to get national inventory levels back to pre-COVID-19 levels. Housing inventory issue with no booming demand. However, we haven’t had a credit sales boom like the one we saw from 2002-2005. million listings.

Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. The housing market can’t replicate the type of massive credit expansion we saw from 2002-2005, so the price-growth story has more to do with inventory collapsing to all-time lows. For some time now, I have been focusing on that 1.52-1.93

As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. What I mean by a credit bust is that after the housing bubble burst in 2005 into 2006, we saw a massive increase in supply. Total inventory levels. NAR: Total Inventory levels 1.22

In addition, this is the fourth straight month of inventory declining, while days on the market are growingl! Plus, available housing inventory remains near historic lows.” Housing inventory. Today, inventory is almost 900,000 active listings below the lowest level of the four-decade average between 2 million and 2.5

This typically happens in a recession, however, the notion that credit lending in America will collapse as it did from 2005 to 2008 couldn’t be more incorrect, as we haven’t had a credit boom in the period between 2008-2022. Look, no massive foreclosures are happening to send inventory skyrocketing. Why is this? Far from the 10.4

Housing data started to soften in 2005 after an overheated market. Here is another precedent: Back in 2012, our housing bear buddies kept insisting that the housing market had 4 million to 5 million homes in what they called shadow inventory. Shadow inventory refers to homes in foreclosure that banks are holding off the market.

At the end of October, housing inventory totaled 1.42 Housing inventory is now at a record low of 2.5 million unit sales pace was the highest since November 2005, and on an annual basis, sales were up a robust 26.6%,” Kan said. ” Yun forecasts existing-home sales to rise by 10%, to 6 million in 2021. million units, down 2.7%

Especially in a year when inventory has crashed to all-time lows and demand for those houses is still so high. I’m going to take their talking points and explain in detail why this isn’t the housing bubble of 2002-2005. “ This got smashed in two years, and inventory levels broke to all-time lows this year.

No, this is not a new home sales housing bubble as we are far from total new home sales being where they were in 2005. The monthly supply of new homes was mostly higher every month in the previous expansion (2008-2019) than any period from 1996-2005. At that time, the new home sales sector got so bad that I put it in the penalty box.

Inventory has broken to all-time lows, but it doesn’t look like the year-over-year data will be positive at all this year unless demand softens up. NAR Research : Unsold inventory sits at a 1.7-month NAR Research : Unsold inventory sits at a 1.7-month However, negative year-over-year inventory is not what we want to see.

Seasonal inventory is about to rise, so let’s hope for the best. However, the demand curve of what we have in housing too doesn’t resemble the speculation demand curve of what we saw from 2002-to 2005. Housing peaked in 2005 and then declined for many years.

We don’t have a massive credit boom as purchase application data is at historical lows; we haven’t had the same run-up in credit as we saw from 2002-2005. If we had a massive credit boom-to-bust, inventory would have skyrocketed in 2022. NAR Total Inventory Data going back to 1982. million, up from 1.03 million last year.

Record-low inventory is pushing home-price growth at double the rate from a year ago, and even above the 10% growth rates seen in 2005,” Kan said. “The housing market is in desperate need of more inventory to cool price growth and preserve affordability. The FHA share of total mortgage applications decreased to 11.3%

Of course, housing starts today aren’t collapsing in the way they did from the peak of 2005 because we haven’t had a sales credit boom in recent years as we did from 2002-2005, which inflated new home sales toward 1.4 Currently, we are in a much different housing recession than what we had from 2005-2011.

However, the real story of 2022 is that the savagely unhealthy housing market continues as inventory is still lower than last year, sending home prices growth into double digits again. Housing demand has been stable for the past few years; we have never had a credit boom in demand since 2002-2005. Unsold inventory sits at a 2.0-month

I first used the term savagely unhealthy in March of 2022 because we had solid demand while inventory was at all-time lows. Credit channels and inventory channels both changed after 2010 because of the qualified mortgage laws and the 2005 bankruptcy reform laws. Unsold inventory sits at a 3.0-month million units, up 3.8%

We simply don’t have enough products for homebuyers, creating forced bidding in a low-inventory environment. Look at the Inventory data below. From NAR: Total housing inventory registered at the end of February was 980,000 units, identical to January & up 15.3% Unsold inventory sits at a 2.6-month

Active inventory above pre-COVID-19 levels The new home sales market doesn’t provide millions of active completed homes for sale, but we are currently back above the pre-COVID-19 levels. months For Sale Inventory and Months’ Supply: The seasonally-adjusted estimate of new houses for sale at the end of June was 476,000.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content