This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The housingmarket in 2024 was about as frustrating for the real estate industry as you can imagine. Thats the highest share for new sales since 2005, which was during the building boom driven by cheaper housing, looser credit requirements and high demand for mortgage-backed securities. million and Bright MLS expecting 4.4

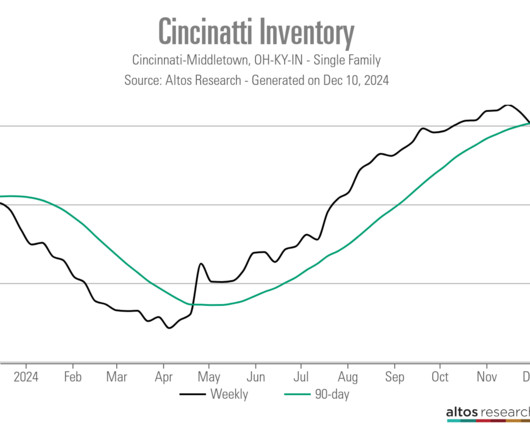

The housingmarket got some much needed relief in the fall when mortgage rates began to drop, but it was short lived. The turbulence in rates has trickled down to individual markets like Cincinnati, where real estate agents say they dont know what to expect from sale to sale. It’s just become a more common theme.

As we close out 2022, it’s time to reflect on a historic year for the housingmarket, which was even crazier than the COVID-19 year of 2020. A few months ago, I was asked to go on CNBC and talk about why I call this a housing recession and why this year reminds me a lot of 2018, but much worse on the four items above.

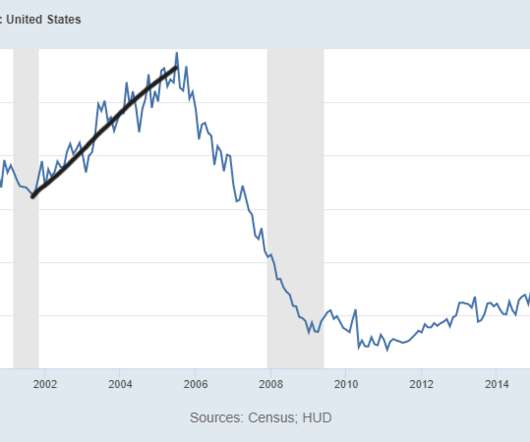

As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. What I mean by a credit bust is that after the housing bubble burst in 2005 into 2006, we saw a massive increase in supply. Total inventory levels.

To get the housingmarket to be sane and normal again, we need inventory to get back in a range between 1.52 – 1.93 million ; this is still historically low, but this gives the housingmarket a breather from the madness that we see today. However, a seller is also a natural homebuyer, unless they’re an investor.

There’s a showdown at the housingmarket corral between homebuyers and sellers. When I came up with the “ savagely unhealthy housingmarket ” label in February of this year, it was based on the premise that the housing inflation story that we have had to deal with since 2020 was a historical event.

This data line lags the current housingmarket as it’s a few months old. Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. million, the housingmarket can be sane again, even though those levels were the historically low levels of inventory going back to 1982.

A bullish housingmarket. economic recovery was a false story and that we were about to embark on a second housing bubble crash due to forbearance. The housingmarket didn’t crash at all, in fact, more Americans bought homes with mortgages in 2021 than in 2020. What a year 2021 has been. The excellent.

The 2022 housingmarket was savagely unhealthy , with all-time lows in inventory leading to massive bidding wars and price spikes until the Fed put a screeching halt to all of it with rate hikes that resulted in the most significant one-year spike in mortgage rate history. Housing recession. That would be a positive for demand.

The “ silver tsunami ” — a colloquialism referring to aging Americans changing their housing arrangements to accommodate aging — could have more of an impact on the housingmarket this year, according to analyst Meredith Whitney in a conversation with Yahoo Finance. “[T]he And people over 50 are 74% of total U.S. homeowners.

We’ve all been wondering what 5% plus mortgage rates would do to the hot housingmarket, and now we’ve got that and a bag of chips. As a result, I’ve been rooting for mortgage rates to rise to create a balancing impact on this housingmarket. Have higher rates worked? Some data to consider: 1.

The spring housingmarket music is playing, and purchase application data and active listing inventory rose together last week. This proves that the mass supply growth we saw from 2005-2007 was due to credit stress, not because the economy was in a recession; the U.S. didn’t go into recession until 2008.

The rise of active listings in this spring housingmarket reminds me of a zombie slowly rising from its grave. Yes, we found the seasonal bottom for housing inventory on April 14, but this year’s rise in active listings has been tepid at best. Can you imagine the housingmarket at that point?

Due to this reality, I have downgraded the housingmarket from unhealthy housing to a savagely unhealthy housingmarket. HousingWire: Switching gears really quickly, have you received any feedback on your savagely unhealthy housingmarket piece ? The days on the market to sell a home is too low.

But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. Understanding this data line and what it is trying to tell you will be more valuable than erroneously thinking the market is crashing and we’ll see a wave of foreclosures.

It’s an excellent time to discuss housing inventory. The housingmarket shifted in March of this year. As the 10-year yield broke above 1.94% and mortgage rates rose, we saw the impact on housing data. Yes, crazy to think, but this is a survey trend data line, and the housingmarket was in free-fall at that time.

.” One of the housing economic realities that I have been trying to stress this year is that a traditional seller of a home is typically a buyer as well. Since the credit standards have improved post-2010, we shouldn’t see distressed sellers until a job loss recession happens, even if sales fall noticeably.

You can see the drastic change this made in the Mortgage Bankers Association Credit Availability index , below, which skyrocketed in 2005 and 2006 before an epic collapse in 2008. Since most sellers are buyers, inventory should be stable if demand is stable. So you can see why we have so few stressed sellers.

housingmarket , we just experienced an event that most people never thought could happen. If you believe people sell to become homeless, then you’re in the group of people that have simply not read housing data for decades. The days on market were too low. And existing home sales crashed in 2022 from a peak of around 6.5

A lot of the housing data was lagging the rate move, so it wasn’t apparent that higher rates impacted the data yet. Going back to the summer of 2020, the one factor that I said could change the housingmarket was the 10-year yield getting above 1.94%. However, the housingmarket changed once the 10-year yield broke over 1.94%.

The big theme of my housing work since 2010 has been that the housingmarket would have its weakest recovery from 2008 to 2019 because we simply built too many homes versus the real demand curve, and monthly supply proves that. million total housing starts until 2020-2024, when demand would warrant that many housing starts.

Homebuyers’ median household income increased by $19,000 this year from 2022, reaching $107,000, according to the National Association of Realtors ’ 2023 Profile of Homebuyers and Sellers. The report is an annual survey of homebuyers and sellers who closed transactions between July 2022 and June 2023.

We finally got mortgage rates to rise, and for people like me who have been concerned about how unhealthy the housingmarket was last year — and it got a lot worse this year — it’s a blessing that was much needed. As you can see below, the new home sales market from 2018-2022 doesn’t look like the housingmarket we had from 2002-2005.

The housingmarket is in a recession, something that the homebuilders and the National Association of Realtors now agree with me on, as this recent CNBC clip shows. Over the years, I have tried to emphasize that the housingmarket in the U.S. can’t have a credit sales boom like we saw from 2002-2005. This is 12.6

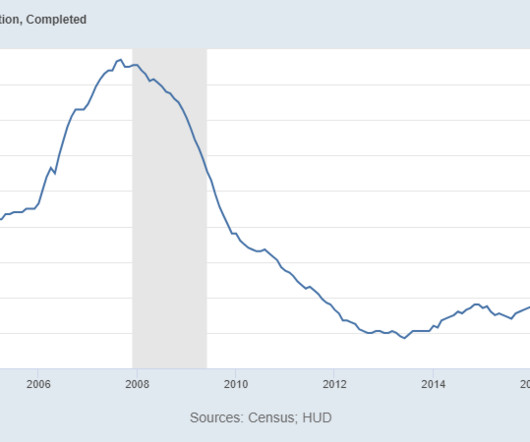

million level we saw in 2005. However, it does show that the builders are in a much better spot to deal with their massive supply, compared to the 2005-2008 period. They are good at selling their inventory much quicker than existing home sellers, who might still be stingy on prices. below the August 2021 estimate of 686,000.

However, what is different this year from 2023 is that we have more sellers that will be buyers. The existing home sales print is catching up to our data, and this, to me, is the best story for housing in 2024 because when the housingmarket was savagely unhealthy in 2022, the NAR total active listings data was below 1 million.

While the growth rate is cooling monthly, we are still in a savagely unhhealthy housingmarket trying to get national inventory levels back to pre-COVID-19 levels. However, we haven’t had a credit sales boom like the one we saw from 2002-2005. However, not to the degree we saw from 2005-2008. million listings.

This is why I have called them efficient home sellers. As we can see in the chart below, sales levels aren’t exactly booming like they were from 2002-2005. From Census: For sale inventory and months’ supply : The seasonally‐adjusted estimate of new houses for sale at the end of August was 436,000.

Just like in the existing home sales market, when sales are low, anything positive on the rate side can move the market in a positive direction. This goes into my low housing bar theme for 2023 and why we need context with sales data. The housingmarket story is about where the 10-year yield is going.

On a positive note, however, the days on the market are no longer a teenager anymore: that metric grew from 18 days to 21 days. I cheer because the savagely unhealthy housingmarket theme I talked about back in February of this year was the same premise of the housing reset talking point the Federal Reserve uses.

Looking at the housingmarket in the years 2020-2024, one risk i identified early on was that home prices could accelerate more in this period than we saw in the previous expansion if inventory channels broke to all-time lows. housingmarket as savagely unhealthy. million homes, using the NAR data.

The big theme of my housing work since 2010 has been that the housingmarket would have its weakest recovery from 2008 to 2019 because we simply built too many homes versus the real demand curve, and monthly supply proves that. million total housing starts until 2020-2024, when demand would warrant that many housing starts.

However, the people who say low inventory is fake news don’t realize that housing credit channels are very different from 2008, which has prevented total active listings from looking anything like 2008. In their haste, they miss the bigger picture of the housingmarket. percent (±15.2 percent (±12.7

As we can see below, from 2000, total active housing inventory rose from 2 million to 2.5 million before we saw the massive stress spike in supply from 2005 to 2007. The NAR data looks a bit backward, so if you want more fresh weekly data, I write the HousingMarket Tracker every week on Sunday night to give you that information.

Looking at the latest NAHB/Wells Fargo homebuilder confidence data and builder stock prices, I can say the homebuilders got very lucky this time around in the middle of a housing recession. They have less competition as they are working from low sales levels in today’s housingmarket. Today, homeowners look great on paper.

This article is part of our housingmarket economic update series. At the end of this series, you can join us on May 10 for a HousingMarket Update webinar. Homes that reach the market sell quickly, bidding wars are the new normal and the investor share of sales continues to rise.

Knowing that the housing crash addicts on YouTube , Twitter , Facebook , and Clubhouse would incorrectly push the negative year-over-year data spin, I wanted to get ahead of that narrative. Then everyone went crazy on investors and iBuyers , suggesting that these people were holding up the entire housingmarket.

They have no emotional ties to houses and don’t need to sell a home to buy another one. They’re effective sellers and don’t want to create a backlog of completed units for sale because that would ruin their business model. Also, in the chart below, we can all agree it isn’t housing2005 or housing 2008 with new home sales.

Between 2002-2005 in many markets, the real estate market was scorching, much like it is today. As appraisers, we faced tremendous pressure from buyers, sellers, real estate agents, and loan officers during the previous run-up. We are seeing that as a profession again. Is this any different than last time?

The truth here that nobody wants to talk about is that we didn’t have a massive sales credit boom in housing from 2020-2021 like we saw from 2002-2005. That would reverse the problem the housingmarket has had selling homes with mortgage rates above 7%.

The one thing housing has going for it now is that we don’t have the speculative booming demand as we saw from 2002 to 2005. From Census: The median sales price of new houses sold in March 2022 was $436,700. The builders have pricing power and they — along with home sellers — have pushed it very hard since 2020.

In reality, as we talked about many times on HousingWire, housing data was going to moderate, find a base and work from that COVID-19 surge in the data. However, with that said, it’s still just an OK housingmarket for me based on how I view the new home sales market. This is 11.9 percent (±20.3 percent (±16.6

Aggregate data from the housingmarket would confirm this. From the Wall Street Journal Editorial Board, “the commission on home sales has stayed basically flat for decades at 6%, split evenly between the buyer and seller agents.” What a truly wrong statement for which is there ample evidence to prove that it is incorrect.

For the past few years, with inventory at historically low levels , sellers were coming pretty close to naming their price and buyers were paying. The low rates made it possible to offer more on a home as the cost of borrowing was lower and therefore, sellers weren’t the ones competing, buyers were. The same will be true for sellers.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content