This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The housingmarket in 2024 was about as frustrating for the real estate industry as you can imagine. Thats the highest share for new sales since 2005, which was during the building boom driven by cheaper housing, looser credit requirements and high demand for mortgage-backed securities. of all transactions. million.

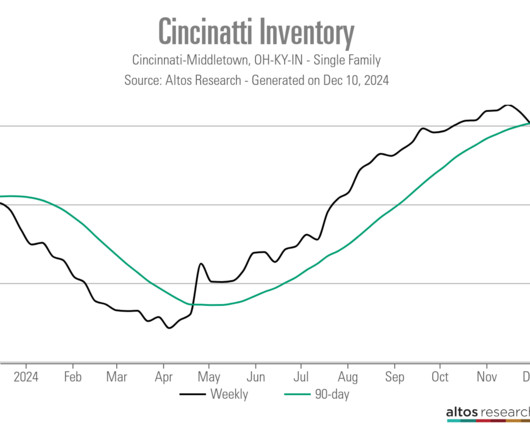

The housingmarket got some much needed relief in the fall when mortgage rates began to drop, but it was short lived. The turbulence in rates has trickled down to individual markets like Cincinnati, where real estate agents say they dont know what to expect from sale to sale.

has experienced two decades of slow but steady housingmarket growth, paired with inventory growth that has suffered through both the Great Recession and the pandemic. In 2023, total inventory hit 144 million housing units, a 16.7% increase from 2005. Americas Boomtowns: Which Cities Grew Housing Inventories the Fastest?

As we close out 2022, it’s time to reflect on a historic year for the housingmarket, which was even crazier than the COVID-19 year of 2020. A few months ago, I was asked to go on CNBC and talk about why I call this a housing recession and why this year reminds me a lot of 2018, but much worse on the four items above.

When you hear people say that the current housingmarket is like 2008 all over again, you may want to remind them of the huge differences between this market and that one. The previous economic expansion, from 2010-2019, wasn’t a housing bubble. Because of this I am calling this the unhealthiest housingmarket post-2010.

Nevertheless, some supposedly erudite thinkers on the housingmarket are saying this, so I thought I should investigate. If the housingmarket was in the grips of some mass hysteria of irrational purchasing, we would expect to see certain hallmarks in the data. The post Is the housingmarket really 20% overbuilt?

The March gain is also the largest since December 2005 and is one of the largest in the index’s 30-year history, said Craig Lazzara, managing director and global head of index investment strategy at S&P DJI. ” The post Home prices haven’t risen this fast since 2005 appeared first on HousingWire. .

Census Bureau data to analyze housing inventory changes across 489 cities between 2005 and 2023. StorageCafe categorized inventory changes by housing type — including single-family, multifamily, middle housing, mobile homes, boats, RVs and vans. ” Nationally, middle housing grew by 11.3% The report used U.S.

The June housing starts data beat estimates with positive revisions, however, this doesn’t change the housingmarket recession call that I made last month. We never saw the credit sales boom as we did from 2002-2005, so the builders themselves are in a better position to manage their future.

Just when I thought days on market were returning to normal, that number for existing homes fell back down to 22 days. If the days on the market are at a teenager level or even lower, it’s never a good sign for the housingmarket. housingmarket inventory channels have changed due to how the U.S.

As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. What I mean by a credit bust is that after the housing bubble burst in 2005 into 2006, we saw a massive increase in supply. Mortgage rates went from a low of 2.5%

To get the housingmarket to be sane and normal again, we need inventory to get back in a range between 1.52 – 1.93 million ; this is still historically low, but this gives the housingmarket a breather from the madness that we see today. Housing is the cost of shelter to own the debt; it’s not an investment.

This was the last thing we needed to see for the HousingMarket , which went from unhealthy to savagely unhealthy. What I am hoping for is that higher rates create more days on the market, cool price growth down, and at some point this year, we stop being negative and be positive on a year-over-year basis.

A bullish housingmarket. economic recovery was a false story and that we were about to embark on a second housing bubble crash due to forbearance. The housingmarket didn’t crash at all, in fact, more Americans bought homes with mortgages in 2021 than in 2020. What a year 2021 has been. The excellent.

However, the real story of 2022 is that the savagely unhealthy housingmarket continues as inventory is still lower than last year, sending home prices growth into double digits again. housingmarket; the 10-year is above 1.94%, something that didn’t happen in 2020 or 2021. From NAR : Total existing-home sales dipped 2.7%

This data line lags the current housingmarket as it’s a few months old. Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. million, the housingmarket can be sane again, even though those levels were the historically low levels of inventory going back to 1982.

The days on market are back to a teenager level in the existing home sales market, which means I can officially say we are back to a savagely unhealthy housingmarket! Nothing good happens in the housingmarket when the days on market are at a teenager level or lower.

I’m talking about housingmarket crash headlines. The housing data has been wild this year. These dramatic peaks and valleys in the data have fed the demons of greed and fear that infest the minds our extreme housing bulls and the fierce housingmarket bears – leading to equally wild speculations about the future of U.S.

million , with double-digit home-price growth driving a housingmarket that is still savagely unhealthy. This is something that I said would change the tone of housing, and we are seeing that result this year as sales decline and inventory picks up. We are not taking the unhealthy housingmarket theme off this marketplace.

The 2022 housingmarket was savagely unhealthy , with all-time lows in inventory leading to massive bidding wars and price spikes until the Fed put a screeching halt to all of it with rate hikes that resulted in the most significant one-year spike in mortgage rate history. Housing recession. That would be a positive for demand.

housingmarket and compare those to where we are today — in the middle of one of the most epic years in our country’s history, due to COVID-19. No doubt about it, the COVID crisis has taken some juice out of the 2020 housingmarket. The February housing data, pre-COVID, was juicy indeed. Context is key!

The “ silver tsunami ” — a colloquialism referring to aging Americans changing their housing arrangements to accommodate aging — could have more of an impact on the housingmarket this year, according to analyst Meredith Whitney in a conversation with Yahoo Finance. “[T]he And people over 50 are 74% of total U.S. homeowners.

We’ve all been wondering what 5% plus mortgage rates would do to the hot housingmarket, and now we’ve got that and a bag of chips. As a result, I’ve been rooting for mortgage rates to rise to create a balancing impact on this housingmarket. The post What 5% mortgage rates mean for the housingmarket?

The spring housingmarket music is playing, and purchase application data and active listing inventory rose together last week. This proves that the mass supply growth we saw from 2005-2007 was due to credit stress, not because the economy was in a recession; the U.S. didn’t go into recession until 2008.

The rise of active listings in this spring housingmarket reminds me of a zombie slowly rising from its grave. Yes, we found the seasonal bottom for housing inventory on April 14, but this year’s rise in active listings has been tepid at best. Can you imagine the housingmarket at that point?

This proves that the mass supply growth we saw from 2005-2007 was due to credit stress, not because the economy was in a recession; the U.S. Even though the labor market is currently showing signs of getting softer , there is no job-loss recession yet. Mortgage rates in a regular market should be 5.25% today but are at 6.5%.

For agents navigating and servicing the American housingmarket , acknowledging its profound evolution over recent decades is crucial. Looking back to the 2005 and 2006 real estate peak, lofty home prices reached a then staggering-sounding high of $230,200 in July 2006. year-over-year increase to 70,829.

Today’s housingmarket suffers from affordability issues due to mortgage rates in the 7s and high home prices. People are quick to panic over any part of the housingmarket that looks stressed, fearing we’ll see 2008 levels of destruction all over again. Why choose 2011?

Traditionally, housing starts, permits, and completions would move together, like what we saw in 2002-2005. In the chart below you can see more evidence of the housing recession; permits are falling as expected with demand getting weaker. From 2002-2005 it was a steady rise to the top of the housing bubble, and then it burst.

According to multiple real estate agents and mortgage brokers, low interest rates and a high percentage of “essential” jobs in their town has kept the housingmarket and local economy strong. rise in houses sold in the same timeframe – from 670 to 940. The post Why is the El Paso housingmarket so hot right now?

One of the reasons that I moved into the “team higher mortgage rate” camp is that what I saw in January, February, and March of this year was so unhealthy that I labeled the housingmarket savagely unhealthy. million — once that happens, I can take the unhealthy label off the housingmarket.

Due to this reality, I have downgraded the housingmarket from unhealthy housing to a savagely unhealthy housingmarket. HousingWire: Switching gears really quickly, have you received any feedback on your savagely unhealthy housingmarket piece ? The days on the market to sell a home is too low.

With the banking crisis spurring more talk of a recession, the question now is: What would housing credit look like in a recession? housingmarket would crash during the pandemic. One of the main reasons for that fear was that housing credit was about to get tight, meaning fewer people could buy homes with mortgages.

It’s an excellent time to discuss housing inventory. The housingmarket shifted in March of this year. As the 10-year yield broke above 1.94% and mortgage rates rose, we saw the impact on housing data. Yes, crazy to think, but this is a survey trend data line, and the housingmarket was in free-fall at that time.

The online reaction was immediate — housing must be about to crash. That’s not to say that the data points the Fed used are incorrect — in fact, we are in a savagely unhealthy housingmarket , but it’s not a bubble. First, because there is no speculative debt demand going on today, there can’t be a housing bubble.

It goes to show what the failure to build enough homes from 2006 to the present combined with ultra-low, unrealistic mortgage rates and massive amounts of fiscal stimulus can do to the housingmarket. This is something that housing industry leaders should be thinking about — carefully. The history of housing.

trillion in 2005 — but sees refinances decreasing to $971 billion. The housingmarket has seen a meaningful rebound since the onset of the pandemic,” said Mike Fratantoni, MBA chief economist. trillion, the highest since 2005. by the end of 2020, rising to 3.3% by Q4 2021. That includes an expected 91.5%

Let’s just say this is the final nail in the coffin for the housing bear troll camps that were so sure that this time, housing would finally crash. COVID didn’t get the housingmarket, but it did pull a fast one on those pesky bears. We saw hints of a flourishing housingmarket prior to the COVID crisis.

This, combined with the 2005 Bankruptcy Reform law and the most prolonged economic and job expansion in our nation’s history before COVID-19, has created a favorable financial environment for American homeowners. The housingmarket doesn’t have an underwater home problem, but that doesn’t mean there isn’t risk for homeowners.

But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. Understanding this data line and what it is trying to tell you will be more valuable than erroneously thinking the market is crashing and we’ll see a wave of foreclosures.

This was the case for housing during the lead-up to the bubble years as housing data went criminally insane in the years 2002-2005. As we close in on Thanksgiving, we can be grateful for the recent excellent jobs report, which shows that the housing crash fanatics have failed once again in 2021. Regarding the U.S.

Last week was wild, and not just for the housingmarket. Inventory grew during the housing bubble years because housing credit was much looser back then, and people could move more freely. Mortgage rates fell even though the jobs report was stronger than anticipated.

One of the unsung heroes of the most prolonged economic and job expansion ever recorded in history was the passing of the 2005 Bankruptcy Reform Act and the 2010 qualified mortgage rule under Dodd-Frank. As we can see below, the bankruptcy levels were extremely high before the bankruptcy law was passed in 2005. Today, we are at 1.25

Because housing data and all economics are so violent lately, we created the weekly HousingMarket Tracker , which is designed to look forward, not backward. This is the wild housing action I have talked about for some time and why the HousingMarket Tracker becomes helpful in understanding this data.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content