This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

For the builders, they have a new problem: they had homes under contract and then mortgage rates jumped in the biggest fashion ever recorded in history. If the builders could, they would take some of the past contracts back, but they’re just stuck with these homes. I personally wouldn’t do it.

Record-low inventory is pushing home-price growth at double the rate from a year ago, and even above the 10% growth rates seen in 2005,” Kan said. “The housing market is in desperate need of more inventory to cool price growth and preserve affordability.

is the highest reading for May since 2005. Contract signings rose in all regions in May compared to the prior month and one year ago. From the National Association of Realtors : “Pending home sales rose 8% in May from the prior month and 13.1% from one year ago. The May 2021 Pending Home Sales Index of 114.7

can’t have a credit sales boom like we saw from 2002-2005. This means we won’t be working from record-breaking demand of high sales like we did at the peak of 2005. The builders are in a better position to manage their inventory glut than when they were working from a credit boom in 2005 that took new home sales up to 1.4

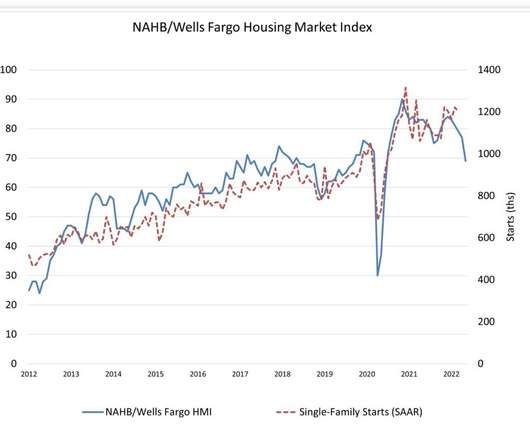

As you can see below, the housing demand data from 2002 to 2005 was never apparent in any housing data lines from 2018 to 2022. It takes forever to finish a home, and now the builders are dealing with the reality of borrowers who went into contract with sub-4% rates and are now dealing with 5%+ rates. percent (±7.7

As you can see, sales levels were never elevated like what we saw from 2002-2005. This housing cycle is and will always be based on real demand, versus the credit boom we saw from 2002 to 2005. The new home sales sector is much different — it’s a contract to purchase a home that isn’t built yet. Slow and steady wins the race.

Pending home sales reached its highest mark for the month of May since 2005, up 8% from the previous month of April as low inventory continues driving buyers to snatch up available real estate. ” Contract signings on new homes increased 13.1% ” Contract signings on new homes increased 13.1% year over year. .

Austin, who joined Cenlar in 2005, will be responsible for managing and mitigating default costs for the wholesale bank’s loans and mortgage servicing rights (MSR) portfolio. Keith Austin has been promoted to director of asset management and valuation services.

That means that our weekly pending sales contract data is showing growth year over year. Of course, the housing market didn’t have the credit sales boom it had from 2002-2005, but it lacked inventory. However, what is different this year from 2023 is that we have more sellers that will be buyers.

An index of 100 is equal to the average level of contract activity during 2001, the first year examined. May’s 8% increase was the highest jump for that month since 2005, according to NAR. The overall pending home sales index fell 1.9% in June, according to the National Association of Realtors , which tracks the metric. (An

Plaintiff Alexander took out a mortgage to purchase a property in Baltimore, Maryland, in 2005. The other plaintiff, Bishop, refinanced his property in Gaithersburg, Maryland, in 2010, with the contract saying payments should be made at an address in Irvine, California, or other places as the lender designated in writing.

An index of 100 is equal to the average level of contract activity during 2001, the first year examined. May’s 8% increase was the highest jump for that month since 2005, according to NAR. The overall pending home sales index fell 1.9% in June, according to the National Association of Realtors , which tracks the metric. (An

This means we don’t have enough housing inventory available because with lending standards back to normal we can’t replicate the credit demand we saw in housing from 2002-2005. The Federal Reserve did not like the homebuying atmosphere during COVID-9, especially the non-contingent buying contracts.

Last week in 2011, 396,955 homes hit the market without a contract. We had a massive credit bust starting in 2005, which continued from 2006 to 2008 — all before the job loss recession began in 2008. For the same week this year, the number was 70,606 new listings. The background to this difference in new listings is important.

.” “Because of this price forecasting volatility, we have had to reconsider what the business might look like at a larger size,” added Barton, who also co-founded Zillow in 2005. In short, Barton lamented that iBuying was too risky a way to spearhead Zillow monetizing its 220 million average monthly unique users. billion.

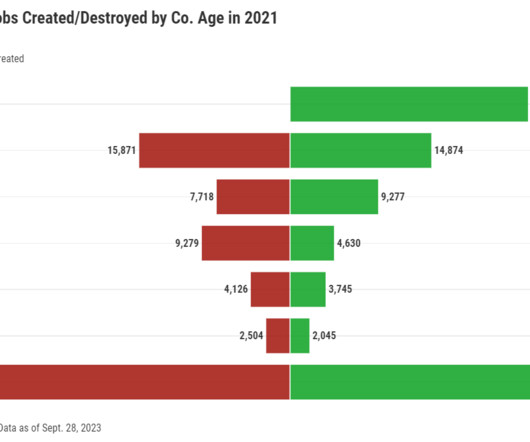

Business Dynamic Statistics data reveal that 2021 was a year of major growth for homebuilders but steep contraction for landlords (called “lessors” in the BDS). gain in 2005. The effects on each industry segment were disparate, the most recently available data for 2021 shows. There were 102,235 firms in 2021, surging 11.5%

Between 2002-2005 in many markets, the real estate market was scorching, much like it is today. Almost daily, there is some story on social media about being “turned in” to the state by a disgruntled agent, buyer, or seller for appraising a property below the contract price. We are seeing that as a profession again.

Due to how HomeServices and its affiliates handle their client contracts, if a dispute arises, each client is entitled to individual arbitration of their claims. HomeServices of America, along with its Berkshire Hathaway subsidiary Long & Foster , filed motions to strike the class-action allegations in favor of arbitration.

Many single-family housing contracts would not have been started if mortgage rates at the day of signing were at 6%-7%. As you can see in the chart below, today’s data looks different from the massive run-up in 2005 and the collapse. With rates spiking so much so soon, the builders are working off that backlog today. percent (±8.9

If the homebuilders and homebuyers knew rates would hit 7% in 2022, many would not have taken those contracts they’re canceling now. Just look at the chart below and how bad credit looked from 2005 to 2008, then the job loss recession happened. Let me be honest here: we got lucky as a country.

In fact, considering the drop in builders’ confidence, now we have to watch for whether some people will cancel their building contracts because rates have jumped so much while they’ve been waiting for their new home to be built. The February rate for units in buildings with five units or more was 501,000.

The higher the number of days between newly listed and accepted contract, the more likely it is for a price to need adjusting to attract more buyers. Pending sales are a key indicator of the number of closings the following month or two, due to the time between an accepted contract and the closing table. It will also cost you.

The mortgage appraisal forms we use today were designed in 2005 using technology and mortgage processes in place at the time. Consider all the technological advances since 2005: Apple released the iPhone, the first touchscreen smartphone. What exactly does this mean?

This report breaks down sales, average prices, the number of active listings, and how many listings went under contract for 2023 compared to 2022 and discusses what is predicted to unfold in 2024. The number of homes placed under contract (pending), decreased by 17.7% Average prices for closed sales increased by 3.4%

This report breaks down sales, average prices, the number of active listings, and how many listings went under contract for 2024 compared to 2023 and discusses what is predicted to unfold in 2024. The number of homes placed under contract (pending) increased by 4.2% Average prices for closed sales increased by 7.4%

Below is a graph that illustrates home sales per year since 2005. Below is a graph that illustrates monthly home prices since 2005. Pending Home Sales (contracts accepted). Both sales and prices were up significantly over recent years- prices are the highest they’ve ever been. 2021 Sales by Month.

I am so glad I quit doing residential lender appraisals in 2005! = The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) increased to 6.80 The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $766,550) decreased to 6.88

40 acre lot, Built in 2005 “The village of Highlands is some of the most expensive real estate in the Carolinas,” Jackson (listing agent) says. “It The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) increased to 7.01 baths, 14,450 sq.ft., percent from 0.5 percent from 6.91

Developed over time with the guidance of prominent designer John Saladino initially and then later with the legendary architect Peter Marino who reimagined the structure back in 2005 and oversaw a 10,000 square foot addition to the house. It tells us more about the trend one month ago when the property got into contract.

I never had more than one assistant and no appraisers after that, and finally quit doing lender residential appraisals in 2005. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($726,200 or less) increased to 7.31 The average contract interest rate for 5/1 ARMs decreased to 6.42

I finally quit doing residential lender appraisals in 2005. ” I was fortunate when I used to do lender appraisals, both residential (quit in 2005) and commercial (quit in 2013). The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($726,200 or less) remained unchanged at 7.61

This report breaks down sales, average prices, the number of active listings, and how many listings went under contract for 2024 compared to 2023 and discusses what is predicted to unfold in 2024. The number of homes placed under contract (pending) increased by 3.4% 2024 was the first growth year since 2020.

Current forms date back to 2005. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) decreased to 6.87 The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $766,550) decreased to 7.07 percent from 7.00

I quit residential lender appraising in 2005. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) decreased to 7.00 The average contract interest rate for 30-year fixed-rate mortgages with jumbo loan balances (greater than $766,550) increased to 7.13

NOTE: Please scroll down to read the other topics in this long blog post on real estate market, USPAP and contracts, unusual homes, mortgage origination stats, etc. ==. USPAP and the Contract. Excerpt: But USPAP and the contract have a very unique relationship. Some appraisers do not like having a copy of the contract.

This class is required before this new UAD material can be taught to other appraisers, under contract with the GSEs. I have not done any residential lender appraisals since 2005. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) decreased to 6.13 percent from 6.15

This can be as simple as implementing digital signature forms for student housing contracts, or as complex as building tech-centric study lounges for students. Campus Paper Waste” 2005. The best place to start is by streamlining processes you already have, then focusing on new tech amenities for comfort and convenience.

Homes Pending (contract accepted) – All of NH. In 2021 there were 27,131 homes listed for all of NH and 26,354 homes marked pending with accepted contracts. Again, right when the pandemic hit, the number of homes that went pending decreased significantly for a few months until it ended up rising above 2019 in August.

For Massachusetts, I had predicted in my 2021 Predictions that it would be the biggest year for overall home sales since 2005 and even though the final numbers aren’t in yet, it looks like my prediction will be right on. It’s not just about how to protect the client with MLS disclosures and contingencies in the contract.

When I did lender res appraisals for direct lenders before 2005, I was usually only contacted if I had a typo: address, no value, etc. Do you really need an expensive support contract? I never buy support contracts. A lot cheaper than a contract. Some good tips for reviewing your non-lender appraisals. percent from 5.47

It is unclear how much they paid for the land, but one batch of parcels was purchased in 2005 for $14.7 The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($766,550 or less) increased to 6.52 The average contract interest rate for 15-year fixed-rate mortgages increased to 5.94

Trying to use the 2005 URAR form is sometimes like trying to put a square peg in a round hole! The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) decreased to 5.46 The average contract interest rate for 30-year fixed-rate mortgages backed by the FHA increased to 5.36

Below is a graph that illustrates home sales per year since 2005. Pending Home Sales (contracts accepted) In the chart below, you’ll see that the amount of homes pending in 2022 was finally lower than year’s past. You can see 2021 exhibited an outlying rise in sales, and 2022 exhibited a significant decrease.

Of course, I gave up residential lender appraising in 2005, before AMCs took over but I liked lender appraising except for the huge ups and downs in business. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($726,200 or less) decreased to 6.48 Every appraisal is a challenge.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content