This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

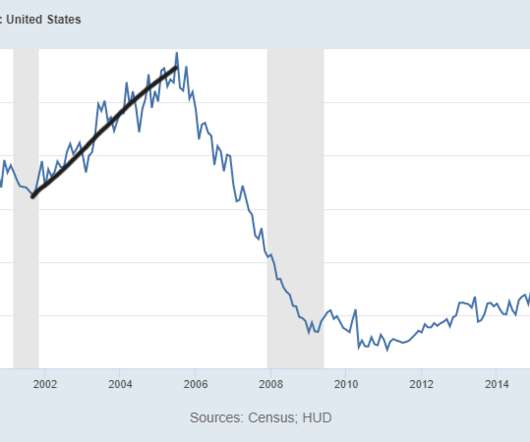

The housing market of 2002-2005 had four years of sales growth facilitated by credit. As we can see below, the purchase application data had four years of growth, peaking in 2005 and then collapsing. However, what isn’t identical is that we have not had a massive sales boom like we saw from 2002-2005. million in 2005.

That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. However, the spike in inventory that we saw from 2006 to 2011 can be attributed to the massive credit bubble we had from 2002 to 2005. Credit stress was evident from 2005 to 2008. What is going on here?

million level we saw in 2005. However, it does show that the builders are in a much better spot to deal with their massive supply, compared to the 2005-2008 period. They are good at selling their inventory much quicker than existing home sellers, who might still be stingy on prices. months are under construction, 1.86

So for now, the builders will take their time with the homes under construction and make sure they offer enough incentives to unload the new home supply they’re dealing with. can’t have a credit sales boom like we saw from 2002-2005. This time, we have less production of homes and more multifamily construction. months and above.

They’re effective sellers and don’t want to create a backlog of completed units for sale because that would ruin their business model. As we can see in the chart below, new home sales aren’t booming like what we saw at the peak of 2005 but are getting back to trend sales growth from the bottom we saw when rates got 5% in 2018.

If sales are working from an elevated number, like what we saw from 2003-2005, it’s a different subject altogether. months of the supply is active listings, 68K 5 months of the supply is still under construction, 280K 1.6 The builders will pull back on construction when the supply is 6.5 When supply is 4.3 When supply is 4.4

This is why I have called them efficient home sellers. As we can see in the chart below, sales levels aren’t exactly booming like they were from 2002-2005. months, the builders will pause construction. months, and we had a big miss on housing starts last week , mostly coming from multifamily construction. We are at 7.8

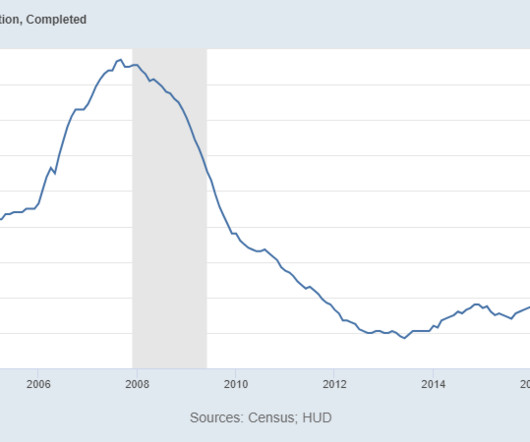

In an odd twist of fate, the delays due to COVID-19 are currently an infrastructure and jobs program for Americans in the construction industry. As you can see below, housing completions are slowly moving along; the homebuilders have more new homes under construction that they haven’t even started yet than active new homes for sale.

I know some people don’t agree with me on this, but the price gains in both the existing home and new home sales sector show that homebuilders and sellers had too much pricing power and needed to be checked. As you can see, sales levels were never elevated like what we saw from 2002-2005. The only way this happens is by higher rates.

According to this theory, we have more homes under construction than any time in history. As we can see in the chart below, it’s not like the new home sales market is booming at all; we aren’t anywhere near the top of sales in 2005 or in 2020. months and above, the builders will pull back on construction. percent (±15.2

As you can see below, the new home sales market from 2018-2022 doesn’t look like the housing market we had from 2002-2005. months and above, the builders will pull back on construction. It’s taking forever to build a home and that has created a huge number of homes under construction. percent (±11.9 percent (±13.7

If you look at the monthly supply for new homes from 1996 to 2005, it was always lower than what we saw from 2008 to 2019. Then in 2018, when mortgage rates got to 5%, we had a supply shock for the builders, which in essence stalled out construction for 30 months. Once total inventory can get back into the range of 1.52 million to 1.93

Housing permits are growing and this is a good thing for the economy and construction jobs. While I have never been a housing construction boom guy because mature economies typically don’t have a construction boom, the fact that permits are keeping their uptrend is a big positive for the United States of America.

months and above, the builders will pull back on construction. It is an embarrassment, but construction productivity — which has been terrible for decades — is now also dealing with shortages that delay finishing homes. When supply is 4.4 months, this is an OK market for the builders. When supply is 6.5 This is 11.9 percent (±20.3

If you look at the monthly supply for new homes from 1996 to 2005, it was always lower than what we saw from 2008 to 2019. Then in 2018, when mortgage rates got to 5%, we had a supply shock for the builders, which in essence stalled out construction for 30 months. Once total inventory can get back into the range of 1.52 million to 1.93

It didn’t help the builders that they had a global pandemic and we still have many new homes either in construction or that haven’t been started yet. months 290,000 new homes are still under construction, about 5.5 We must remember that the builders don’t operate like existing home sellers; they treat their products as commodities.

Even though multifamily construction has boosted housing starts recently, the slowdown in single-family purchases hasn’t been anything too dramatic yet. The one thing housing has going for it now is that we don’t have the speculative booming demand as we saw from 2002 to 2005. percent (±12.9 percent (±11.3 When supply is 4.4

This problem is much different than the housing credit bubble of 2002-2005. Home sellers and builders had too much pricing power, pushing prices to the extreme. From BLS : The downside of higher rates Housing construction will slow. housing market as savagely unhealthy.

HousingWire: How will rising rates affect new home construction? Housing construction will be impacted if the monthly supply for new homes breaks above 6.5 The only thing that I believe creates balance in the housing market is higher rates because the sellers and builders have too much pricing power in this low inventory environment.

Similarly, companies like Zillow and Trulia launched in 2005 and 2006 as “real estate search engines” to help buyers more easily find a home online. Having everything in-house enables iBuyers to lower closing costs for buyers and sellers, offer real-time, 24/7 customer support and provide unique financing solutions for buyers.

Existing home sales fell very fast in 2022 due to higher mortgage rates and a lack of new listing growth, which meant the number of traditional sellers who bought a home was much lower in 2022. months with many homes still under construction or haven’t even started being built yet. We are at 8.6 months, which makes the job harder.

is skilled in many facets of real estate including both Buyer & Seller Representation, Commercial, Investment, Relocation & Luxury Properties. Licensed in NH since 2005 and MA since 2007, she brings a deep passion for real estate, a strong work ethic, and expert market knowledge. To learn more about her, click here.

In it I included a year over year chart of all sales through the local MLS back to 2005. This information clearly shows a declining trend from the 2005 data down to a low point between 2009 and 2011. Houses in blue, condominium units in orange, new construction included. Year to year trends. What happens if it only tops 15%?

NOTE: Please scroll down to read the other topics in this long blog post on non-lender appraisals, using new construction comps for existing homes, master planned communities, unusual homes, mortgage origination stats, etc. I was lucky to have never had to use new construction as a comp on an existing home. baths, 14,450 sq.ft.,

From offering dramatically over asking price, putting down massive deposits, waiving home inspection contingencies or not doing home inspections at all, waiving mortgage contingencies, agreeing to close whenever sellers want, and more. Home sellers are usually motivated to list when they see homes on the market that they want to buy.

Buyers will continue to outstrip sellers by a significant margin but less extreme than in 2021. New construction across King is projected to decline a surprising 11% in dollar terms in 2022. Even in the housing bubble of 2005, prices rose “only” 12% nationally.) What will the 2022 Seattle/King County housing market offer?

Since then, she has taken off running and has helped her buyers and sellers reach their goals. Cyndi thrives to make her buyers and sellers her top priority. Licensed in NH since 2005 and MA since 2007, she brings a deep passion for real estate, a strong work ethic, and expert market knowledge.

Heidi is a stellar real estate agent who, since 2005, has been helping her clients buy and sell homes with ease and friendliness. And has quickly became a key figure, known for her expertise with buyers, sellers, and investors. She joined Lamacchia Realty in July 2024 after their merger with Berkshire Dream Home.

I am so glad I quit doing residential lender appraisals in 2005! = single-family homes for sale in the fourth quarter were new construction. Construction also jumped during the pandemic as builders responded to surging homebuyer demand fueled by record-low mortgage rates. Nationwide, 31.8% That’s comparable with 31.9%

A buyer gets a seller’s disclosure statement for that information. Tomorrow, I’m supposed to become a data scientist and try to decipher the value of a property I’ve never seen, bought and sold by buyers and sellers I’ve never met. I purchased a large house on the water with a dock in 1995 for $375,000 with 100% seller financing.

Developed over time with the guidance of prominent designer John Saladino initially and then later with the legendary architect Peter Marino who reimagined the structure back in 2005 and oversaw a 10,000 square foot addition to the house. The setting is unique as are the coastline views to the east and west. Don’t get me wrong.

What’s in This Newsletter (in Order) Confirming Construction Progress The New UAD: “Don’t Borrow Trouble.” Current forms date back to 2005. The seller, an investor who had purchased the home in an estate sale, was unaware of the system’s location. The seller agreed to pump the tanks so the area could be determined.

The frame is built with 60 tons of steel and construction took over 6 years utilizing artisans from all over the world. 31% of women and 27% of men signed up for Social Security at age 62 in 2018, down from around 54% of women and 50% of men in 2005, according to Social Security Administration data. Excerpts: Built 1990 | 6,106 Sq.

In 2005 I finally quit all residential lender work due to the huge ups and downs in business. Modern and contemporary styles still have a stronghold on new construction, but as we found, they have spawned many offshoots, each of which has bloomed into a distinct aesthetic in its own right. In the early 1990s, my market crashed.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content