This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The March gain is also the largest since December 2005 and is one of the largest in the index’s 30-year history, said Craig Lazzara, managing director and global head of index investment strategy at S&P DJI. ” Mortgage rates continue to hover around 3%, keeping prospective homebuyers interested, Speakman said.

Tuesday’s housing starts report clearly shows that homebuilders are going to be done with single-family construction until mortgage rates fall. If it wasn’t for solid rental demand boosting multifamily construction this year — 18% year to date —this data line would have looked much worse.

Census Bureau released their construction report for February, showing a positive trend in housing construction data with a lovely print in housing permits at 1,859,000 and housing starts at 1,769,000. So far, housing construction has done well during 2020-2022 considering the economic drama. Today, the U.S.

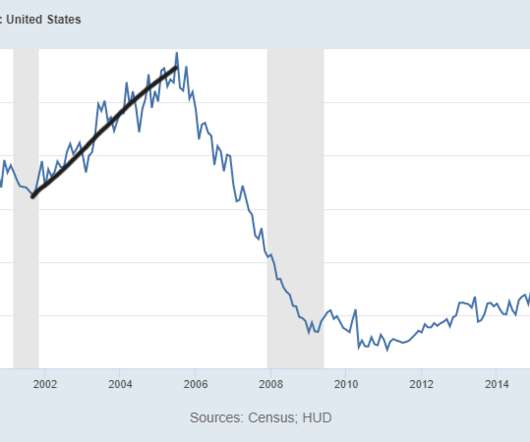

As you can see below, during the housing bubble years, housing starts, permits, sales, credit, prices and housing completions moved together in 2005 to form the peak of the housing bubble. The new home sales market gets hit harder by higher mortgage rates than the existing home market. When supply is 4.4 months and above. months to 8.1

What is the best news for mortgage rates long-term? More supply of apartments coming on line will be good news for mortgage rates going forward. As you can see in the chart below, this looks nothing like the housing peak in 2005 and the crash toward 2008. This is key for mortgage rates looking out for years to come.

However, the demand curve of what we have in housing too doesn’t resemble the speculation demand curve of what we saw from 2002-to 2005. So the type of boom and bust we would need to see to reflect bubble speculation demand isn’t in this market like we saw from 2002-to 2005. Have more questions for Logan?

Census Bureau released their new residential construction report for April, showing a miss on the estimate and a negative revisions data line, which I believe is lagging behind the current market reality. We simply cannot finish homes in America promptly, and now that mortgage rates are over 5%, some buyers won’t be able to purchase a home.

We had some good news this week for the housing market : purchase application data is up , the builder’s confidence index rose to beat estimates, and the 10-year yield and mortgage rates have fallen. million until 2020-2024, when demand would finally warrant that type of construction. percent (±16.9 percent (±11.2

For this reason, the number of housing units “under construction” is the largest ever recorded in history because they were taking so long to finish. For the builders, they have a new problem: they had homes under contract and then mortgage rates jumped in the biggest fashion ever recorded in history.

How is today’s housing starts data , which beat expectations, good for mortgage rates ? What we see in this latest starts report is encouraging, as a record number of 5-units are still in construction and anything that gets finished is positive against inflation. Like most recessions, when demand falls, so does production.

The housing sector — especially real estate and mortgage — has seen significant layoffs , while the general economy will create more than 4 million jobs in 2022. Then we had the biggest mortgage rate shock in recent history and yet even with that, we will have over 5 million total home sales this year. Production falls. Home sales.

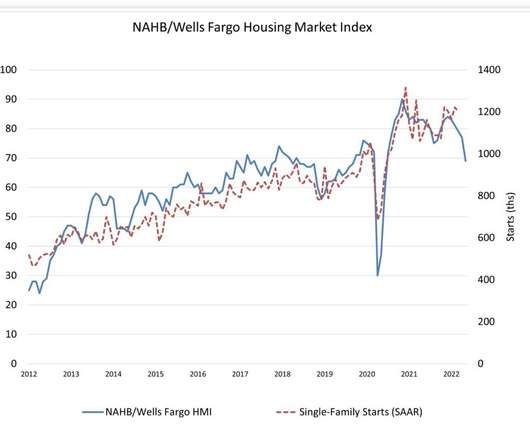

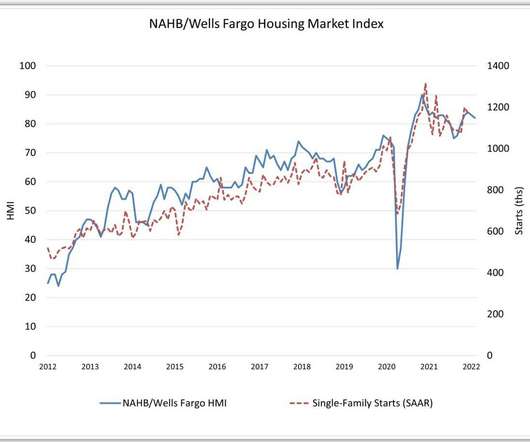

The smart thing to do is go with the builder sentiment trend until it reverses, and most likely, we will need to see lower mortgage rates for that to happen. From the National Association of Home Builders : Looking at the housing starts report, the numbers came in slightly better than anticipated, driven by multifamily construction.

Housing construction in the U.S. Just to give you some perspective here, at the peak of 2005, we had about 2.24 months of homes they have under construction or have not even started yet. Now that mortgage rates have spiked up so much, the housing construction growth we have seen in single-family construction is done.

Will the Federal Reserve pivot in time to save construction workers? This is key because, traditionally, residential construction workers are the first to lose their jobs before every recession since higher mortgage rates hit housing first. months , the builders will pause construction. percent (±14.6 percent (±15.2

As the 10-year yield broke above 1.94% and mortgage rates rose, we saw the impact on housing data. That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. Credit stress was evident from 2005 to 2008. We have more housing starts under construction now than in recent history!

However, demand has construction playing catch-up , as the estimate of new houses for sale at the end of October was just 278,000. Sales are increasingly being driven from homes not yet under construction. And more sales means more construction means more sales: A large share (38.5%, up from 28.5% This represents a supply of 3.3

We finally got mortgage rates to rise, and for people like me who have been concerned about how unhealthy the housing market was last year — and it got a lot worse this year — it’s a blessing that was much needed. million line in the sand has been this: Home prices grow above that 23% level: check Mortgage rates spike higher: check.

Tuesday’s new home sales report missed expectations and had negative revisions, which isn’t surprising given this sector of our economy simply can’t handle higher mortgage rates. can’t have a credit sales boom like we saw from 2002-2005. This time, we have less production of homes and more multifamily construction.

Construction of single-family homes dropped 2.3% from November to 1.172 million units, the construction of multifamily units again posted a sizable increase of 13.7% 2021 was a strong year for construction.”. But while this is good news for new housing construction, homebuilders still have plenty of obstacles to overcome.

9 up until the early part of February as mortgage rates fell from 7.37% to 5.99%. To combat higher mortgage rates, builders have been cutting prices and buying down rates to move product. If sales are working from an elevated number, like what we saw from 2003-2005, it’s a different subject altogether. When supply is 4.3

We had a period this summer when mortgage rates moved from 6.25% back down to 5% and some of the new home sales activity picked up. million level we saw in 2005. However, it does show that the builders are in a much better spot to deal with their massive supply, compared to the 2005-2008 period. When supply is 4.4

This data line confirms what we all know to be the case: The housing market, at least as it relates to construction, is in a recession. We talked about this in March , and even last year, when I wrote about the problem with the housing construction boom premise. “I don’t expect a boom in housing construction.

As we enter the second quarter of 2021, it’s time for the mortgage industry to reflect on the past 12 months and think about how to plan for the same period ahead. Low mortgage rates, driven by quantitative easing by the Federal Reserve helped fuel a boom in both mortgage refinancing and purchases, making 2020 the second-best year in U.S.

NAR total active listings data going back to 1982 : This explains why the builders and new homes are doing better than the existing home sales market, which deals with higher mortgage rates and low active listings. Also, in the chart below, we can all agree it isn’t housing 2005 or housing 2008 with new home sales. When supply is 4.4-6.4

This is the reason construction workers still have jobs, and that backlog needs to be finished; this is a positive outcome. The bigger story here is that if we want to see mortgage rates fall, we need more rental units, and right now we have a massive backlog of 2-unit homes under construction — over 900,000. percent (±12.3

New home sales missed estimates today but had three months of positive revisions, which continues the story of the builders managing the higher mortgage rate environment. However, higher mortgage rates make it harder and harder to pull some of those deals off. months, the builders will pause construction. When supply is over 6.5

The new home sales market is doing well as it really benefits from lower mortgage rates. I have said for many years that we wouldn’t see total housing construction start a year at 1.5 I have said for many years that we wouldn’t see total housing construction start a year at 1.5 The median sales price is now 11.4%

The truth is that if mortgage rates fell below 5.875% and kept going lower, everyone’s housing predictions would need to be revised this year because the builders can sell their homes with lower mortgage rates. This is why construction workers haven’t been laid off while other jobs in the housing market have been.

It gives an idea of what to expect for housing construction. months and above, the builders will pull back on construction. The real question is how much higher mortgage rates will bite the most sensitive sector to rates: new homes. The builders will pull back on construction growth if new homes sales start to head lower.

At its Annual event Wednesday, Mortgage Bankers Association Chief Economist Mike Fratantoni forecast that interest rates could rise in the year to come, but that they will remain near all-time lows. The chart below shows interest rates for the 30-year fixed-rate mortgage will end this year at about 3% and could hit around 3.3%

In addition, employment in the construction industry is now 21,000 jobs above its pre-pandemic level after the sector added 2,000 jobs. of its pre-pandemic level,” Mike Fratantoni, the Mortgage Bankers Association’s SVP and chief economist, said in a statement. had another strong month in April. recorded in February 2020.

Construction continued to play catch-up also as Novembers new-home inventory rose nearly 14% to a 4.1-month How the mortgage industry is working together to make housing more affordable. Eager buyers have been snapping up available new homes, an increasing share of which have not even begun construction, at their highest pace in years.

They can cut prices, pay down mortgage rates for their buyers, and do what they need to to make it work for them to move their products. We didn’t have the credit stress issue from 2010-2023 like we did from 2005 through 2008. The builders will pull back on construction when the supply is 6.5 When supply is 4.3

The housing market didn’t crash at all, in fact, more Americans bought homes with mortgages in 2021 than in 2020. mortgage rates, so on the mortgage rate side of the equation, it’s never been better. Housing permits are growing and this is a good thing for the economy and construction jobs. These households got sub-3.5%

years in 2005, according to a Redfin analysis of median U.S. Older Americans also have financial incentives attached to staying in their homes, since 54% of the baby boomer cohort own their homes free and clear without making monthly mortgage payments. years last year, up from 6.5 homeowner tenure by year using county records.

According to this theory, we have more homes under construction than any time in history. As we can see in the chart below, it’s not like the new home sales market is booming at all; we aren’t anywhere near the top of sales in 2005 or in 2020. months and above, the builders will pull back on construction. percent (±15.2

A few months ago, I wrote that the new home sales sector is at risk because of rising mortgage rates. As you can see, sales levels were never elevated like what we saw from 2002-2005. This housing cycle is and will always be based on real demand, versus the credit boom we saw from 2002 to 2005. Slow and steady wins the race.

As you can see below, new home sales are still below the 2000 recession level, and we just had a significant spike in mortgage rates too. These monthly reports can be very wild, and I anticipate big swings in the reports until things calm down with mortgage rates. Five months of the supply are homes in construction.

In 2005, when the housing bubble peaked in sales at around 1.4 The builders will pull back on construction when the supply is 6.5 We are still in housing recession land as the builders still have a lot of new construction homes and haven’t started yet to build. When supply is 4.3 When supply is 4.4 months and above.

You always want to be skeptical of any housing starts data that comes in too strong or too negative from the trend, and we had some specific factors in this report that boosted multifamily construction. Some of the demand that we saw from 2002-2005 was facilitated by credit that no longer exists in the marketplace today. This is 17.2

Pending home sales reached its highest mark for the month of May since 2005, up 8% from the previous month of April as low inventory continues driving buyers to snatch up available real estate. ” Ruben Gonzalez, Keller Williams chief economist, added that he is “optimistic” new home construction will pick up.

months and above, the builders will pull back on construction. It is an embarrassment, but construction productivity — which has been terrible for decades — is now also dealing with shortages that delay finishing homes. When supply is 4.4 months, this is an OK market for the builders. When supply is 6.5 This is 11.9 percent (±20.3

This problem is much different than the housing credit bubble of 2002-2005. Mortgage rates of 4%-5% weren’t doing the amount of demand destruction I thought they would. Mortgage rates closer to 6% for sure are driving bigger year-over-year decline data. From BLS : The downside of higher rates Housing construction will slow.

If you look at the monthly supply for new homes from 1996 to 2005, it was always lower than what we saw from 2008 to 2019. Then in 2018, when mortgage rates got to 5%, we had a supply shock for the builders, which in essence stalled out construction for 30 months.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content