This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

increase from 2005. From 2005 to 2023, single family homes increased by only 16.7%, with annual expansions remaining below 1%. Florida, Texas, and North Carolina were three of the most popular states for relocation, and this accelerated migration has fueled construction to meet the surging housing demand.

New-home construction in the U.S. Census Bureau data to analyze housing inventory changes across 489 cities between 2005 and 2023. from 2005 to 2023 — the lowest inventory increase among all property types. has focused on single-family and multifamily inventory growth to boost supply and affordability. The report used U.S.

The March gain is also the largest since December 2005 and is one of the largest in the index’s 30-year history, said Craig Lazzara, managing director and global head of index investment strategy at S&P DJI. ” The post Home prices haven’t risen this fast since 2005 appeared first on HousingWire. .

Census Bureau released their construction report for February, showing a positive trend in housing construction data with a lovely print in housing permits at 1,859,000 and housing starts at 1,769,000. So far, housing construction has done well during 2020-2022 considering the economic drama. Today, the U.S.

Tuesday’s housing starts report clearly shows that homebuilders are going to be done with single-family construction until mortgage rates fall. If it wasn’t for solid rental demand boosting multifamily construction this year — 18% year to date —this data line would have looked much worse. Why do I call it a housing recession?

Housing construction in the U.S. Just to give you some perspective here, at the peak of 2005, we had about 2.24 months of homes they have under construction or have not even started yet. Now that mortgage rates have spiked up so much, the housing construction growth we have seen in single-family construction is done.

For this reason, the number of housing units “under construction” is the largest ever recorded in history because they were taking so long to finish. Housing construction productivity has always been terrible compared to other sectors of our economy; I get that, as we still build homes with hammers and nails, not robots.

From the National Association of Home Builders : Looking at the housing starts report, the numbers came in slightly better than anticipated, driven by multifamily construction. Still, it’s backward-looking and the growth in multifamily construction, which we desperately need to cool down rental inflation, has recently been positive.

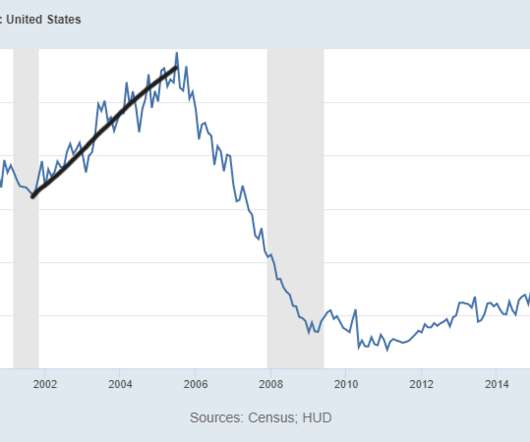

The housing market of 2002-2005 had four years of sales growth facilitated by credit. As we can see below, the purchase application data had four years of growth, peaking in 2005 and then collapsing. However, what isn’t identical is that we have not had a massive sales boom like we saw from 2002-2005. million in 2005.

However, demand has construction playing catch-up , as the estimate of new houses for sale at the end of October was just 278,000. Sales are increasingly being driven from homes not yet under construction. And more sales means more construction means more sales: A large share (38.5%, up from 28.5% This represents a supply of 3.3

That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. However, the spike in inventory that we saw from 2006 to 2011 can be attributed to the massive credit bubble we had from 2002 to 2005. Credit stress was evident from 2005 to 2008. What is going on here?

Will the Federal Reserve pivot in time to save construction workers? This is key because, traditionally, residential construction workers are the first to lose their jobs before every recession since higher mortgage rates hit housing first. months , the builders will pause construction. months 274K homes under construction = 5.3

So for now, the builders will take their time with the homes under construction and make sure they offer enough incentives to unload the new home supply they’re dealing with. can’t have a credit sales boom like we saw from 2002-2005. This time, we have less production of homes and more multifamily construction. months and above.

Construction of single-family homes dropped 2.3% from November to 1.172 million units, the construction of multifamily units again posted a sizable increase of 13.7% 2021 was a strong year for construction.”. But while this is good news for new housing construction, homebuilders still have plenty of obstacles to overcome.

million level we saw in 2005. However, it does show that the builders are in a much better spot to deal with their massive supply, compared to the 2005-2008 period. The builders will pull back on construction when the supply is 6.5 months are under construction, 1.86 below the August 2021 estimate of 686,000.

However, the demand curve of what we have in housing too doesn’t resemble the speculation demand curve of what we saw from 2002-to 2005. So the type of boom and bust we would need to see to reflect bubble speculation demand isn’t in this market like we saw from 2002-to 2005. Have more questions for Logan?

to help with persistent labor shortages, the construction industry reversed this trend and managed to attract over 90,000 new immigrant workers, levels unseen since the housing boom of 2005-2006. After years of being unable to ratchet up the number of new workers coming from outside the U.S.

million until 2020-2024, when demand would finally warrant that type of construction. Fortunately, as you can see in the chart below, the number of housing units (five units or more) under construction is historically high. There are 943,000 apartments currently under construction. percent (±16.9 percent (±11.2 When supply is 4.3

This data line confirms what we all know to be the case: The housing market, at least as it relates to construction, is in a recession. We talked about this in March , and even last year, when I wrote about the problem with the housing construction boom premise. “I don’t expect a boom in housing construction.

As we can see in the chart below, new home sales aren’t booming like what we saw at the peak of 2005 but are getting back to trend sales growth from the bottom we saw when rates got 5% in 2018. Also, in the chart below, we can all agree it isn’t housing 2005 or housing 2008 with new home sales. When supply is 4.4-6.4 When supply is 6.5

If sales are working from an elevated number, like what we saw from 2003-2005, it’s a different subject altogether. months of the supply is active listings, 68K 5 months of the supply is still under construction, 280K 1.6 The builders will pull back on construction when the supply is 6.5 When supply is 4.3 When supply is 4.4

In addition, employment in the construction industry is now 21,000 jobs above its pre-pandemic level after the sector added 2,000 jobs. While the number of employees in construction is on the rise, annual growth in average hourly earnings of production and nonsupervisory employees in construction slowed in April from 6.1%

As you can see below, during the housing bubble years, housing starts, permits, sales, credit, prices and housing completions moved together in 2005 to form the peak of the housing bubble. We have 910,000 two-unit buildings under construction; let’s get these buildings out to fight inflation! When supply is 4.4 months and above.

This is the reason construction workers still have jobs, and that backlog needs to be finished; this is a positive outcome. The bigger story here is that if we want to see mortgage rates fall, we need more rental units, and right now we have a massive backlog of 2-unit homes under construction — over 900,000. percent (±12.3

Construction continued to play catch-up also as Novembers new-home inventory rose nearly 14% to a 4.1-month a record low in the series dating back to 1963, while the share of homes sold-but-not-yet-started was at a level only seen during the housing bubble in 2005.” The West came in second at a 17.3%

The New York City Council this week narrowly passed a housing plan backed by Mayor Eric Adams (D) known as City of Yes, which calls for the construction of 82,000 new homes over the next 15 years in the Big Apple. But the plan backed by a mayor who is currently embroiled in a high-profile legal case in which the U.S.

As you can see in the chart below, this looks nothing like the housing peak in 2005 and the crash toward 2008. However, because of the COVID-19 delays, we are still working through a backlog of homes under construction. As you can see in the chart below, we have a historic number of 5-unit construction in the works.

As we can see in the chart below, sales levels aren’t exactly booming like they were from 2002-2005. months, the builders will pause construction. months, and we had a big miss on housing starts last week , mostly coming from multifamily construction. They will build as long as new home sales are growing. When supply is over 6.5

It gives an idea of what to expect for housing construction. months and above, the builders will pull back on construction. The builders will pull back on construction growth if new homes sales start to head lower. The MBA purchase application data from 2002-2005 is much different than what we have seen from 2018-2022.

Census Bureau released their new residential construction report for April, showing a miss on the estimate and a negative revisions data line, which I believe is lagging behind the current market reality. As you can see below, the housing demand data from 2002 to 2005 was never apparent in any housing data lines from 2018 to 2022.

As you can see, sales levels were never elevated like what we saw from 2002-2005. This housing cycle is and will always be based on real demand, versus the credit boom we saw from 2002 to 2005. months and above, the builders will pull back on construction. However, this is much different than what we saw from 2002-to 2005.

I have said for many years that we wouldn’t see total housing construction start a year at 1.5 2020 is looking great on that front for the new home sales market and housing starts, which need more new home sales to warrant more single-family construction. It is not out of the question that we can get to 6.2 Context is key!

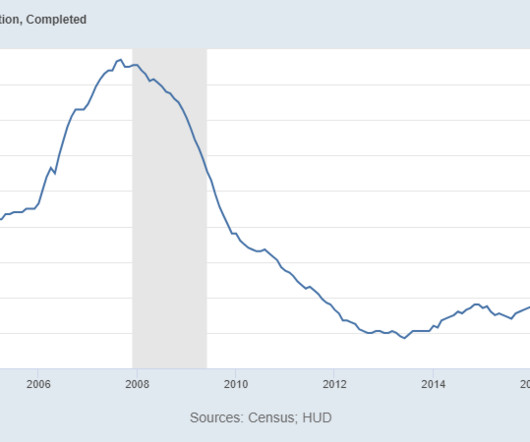

In an odd twist of fate, the delays due to COVID-19 are currently an infrastructure and jobs program for Americans in the construction industry. As you can see below, housing completions are slowly moving along; the homebuilders have more new homes under construction that they haven’t even started yet than active new homes for sale.

You always want to be skeptical of any housing starts data that comes in too strong or too negative from the trend, and we had some specific factors in this report that boosted multifamily construction. Some of the demand that we saw from 2002-2005 was facilitated by credit that no longer exists in the marketplace today. This is 17.2

Housing permits are growing and this is a good thing for the economy and construction jobs. While I have never been a housing construction boom guy because mature economies typically don’t have a construction boom, the fact that permits are keeping their uptrend is a big positive for the United States of America.

We didn’t have the credit stress issue from 2010-2023 like we did from 2005 through 2008. The builders will pull back on construction when the supply is 6.5 We have had many people on social media sites saying a massive housing supply will hit the market soon because we have a record amount of homes under construction.

According to this theory, we have more homes under construction than any time in history. As we can see in the chart below, it’s not like the new home sales market is booming at all; we aren’t anywhere near the top of sales in 2005 or in 2020. months and above, the builders will pull back on construction. percent (±15.2

years in 2005, according to a Redfin analysis of median U.S. Some young families are turning to new construction, and others are renting homes.” While “homeowner tenure” has fallen slightly since its 2020 peak, the length of time that homeowners are remaining in their properties doubled to 11.9 years last year, up from 6.5

Pending home sales reached its highest mark for the month of May since 2005, up 8% from the previous month of April as low inventory continues driving buyers to snatch up available real estate. ” Ruben Gonzalez, Keller Williams chief economist, added that he is “optimistic” new home construction will pick up.

What we see in this latest starts report is encouraging, as a record number of 5-units are still in construction and anything that gets finished is positive against inflation. As you can see, the 1974 recession destroyed the 5-unit construction production. The future growth of 5-unit construction will be at risk if a recession happens.

Five months of the supply are homes in construction. That is a high level, and two months of the supply hasn’t started construction yet, and a whopping 0.68 The builders will pull back on construction when the supply is 6.5 We don’t say the new home sales market supply is the existing home sales market. When supply is 4.4

If you look at the monthly supply for new homes from 1996 to 2005, it was always lower than what we saw from 2008 to 2019. Then in 2018, when mortgage rates got to 5%, we had a supply shock for the builders, which in essence stalled out construction for 30 months.

In 2005, when the housing bubble peaked in sales at around 1.4 The builders will pull back on construction when the supply is 6.5 We are still in housing recession land as the builders still have a lot of new construction homes and haven’t started yet to build. When supply is 4.3 When supply is 4.4 months and above.

months and above, the builders will pull back on construction. It is an embarrassment, but construction productivity — which has been terrible for decades — is now also dealing with shortages that delay finishing homes. When supply is 4.4 months, this is an OK market for the builders. When supply is 6.5 This is 11.9 percent (±20.3

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content