This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Ive been doing this since 2005 and I tell clients that Ive never seen a market like this, so we have to navigate it together. Its a symptom of a market thats transitioning away from sellers. Altos considers anything above 30 to be indicative of a seller’s market. A substantial drop in new listings is a contributing factor.

There’s a showdown at the housing market corral between homebuyers and sellers. This doesn’t mean homebuyers don’t have something of an edge now: As inventory has increased and buying power has faded, the buyers who are available are dealing with a lot less competition as the bidding wars are ending. million today.

The housing market of 2002-2005 had four years of sales growth facilitated by credit. As we can see below, the purchase application data had four years of growth, peaking in 2005 and then collapsing. However, what isn’t identical is that we have not had a massive sales boom like we saw from 2002-2005. million in 2005.

You can see the drastic change this made in the Mortgage Bankers Association Credit Availability index , below, which skyrocketed in 2005 and 2006 before an epic collapse in 2008. Since most sellers are buyers, inventory should be stable if demand is stable. So you can see why we have so few stressed sellers.

Homebuyers’ median household income increased by $19,000 this year from 2022, reaching $107,000, according to the National Association of Realtors ’ 2023 Profile of Homebuyers and Sellers. The report is an annual survey of homebuyers and sellers who closed transactions between July 2022 and June 2023.

But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. This time around, we have not seen the kind of housing credit boom that we did from 2002-2005. Purchase application data is now below 2008 levels! This means less demand for housing.

As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. What I mean by a credit bust is that after the housing bubble burst in 2005 into 2006, we saw a massive increase in supply. Total inventory levels. NAR: Total Inventory levels 1.22

Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. The housing market can’t replicate the type of massive credit expansion we saw from 2002-2005, so the price-growth story has more to do with inventory collapsing to all-time lows. This is because the biggest buyers of homes are mortgage buyers.

My concern now is that some sellers are feeling stressed about this market, which should never happen because this is the best seller market ever. However, a seller is also a natural homebuyer, unless they’re an investor. You can see why some sellers are stressed now. People who sell need to live somewhere.

.” One of the housing economic realities that I have been trying to stress this year is that a traditional seller of a home is typically a buyer as well. Since the credit standards have improved post-2010, we shouldn’t see distressed sellers until a job loss recession happens, even if sales fall noticeably.

That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. However, the spike in inventory that we saw from 2006 to 2011 can be attributed to the massive credit bubble we had from 2002 to 2005. Credit stress was evident from 2005 to 2008. What is going on here?

And the peak in existing home sales was 2005 when you had around 7 million transactions.” That’s what I think is invariably going to happen because you’re going to have more seniors, the silver tsunami, selling and there are fewer buyers so the give is going to be lower home prices.” homeowners.

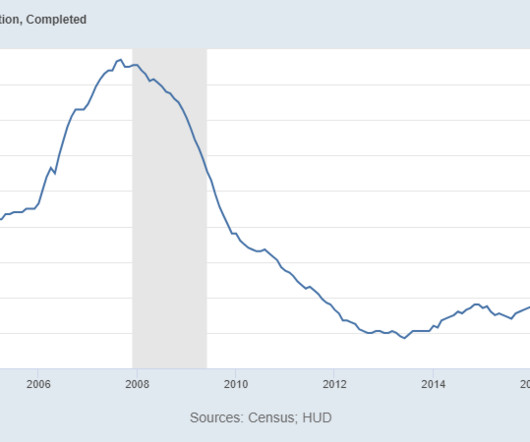

can’t have a credit sales boom like we saw from 2002-2005. This means we won’t be working from record-breaking demand of high sales like we did at the peak of 2005. The builders are in a better position to manage their inventory glut than when they were working from a credit boom in 2005 that took new home sales up to 1.4

They’re effective sellers and don’t want to create a backlog of completed units for sale because that would ruin their business model. This means new homes — with all the bells and whistles — can peel some buyers from the existing home sales market, especially if they pay down mortgage rates. Now on to the report.

Between 2002-2005 in many markets, the real estate market was scorching, much like it is today. Prices were escalating quickly, and buyers were purchasing in a frenzy for fear of being left behind and not being able to get their foot on the property ladder. This is no different than ignoring declining trends. How do we combat this?

However, we haven’t had a credit sales boom like the one we saw from 2002-2005. Total Inventory had been growing from 2001-2005; total listings data in 2005 was at the higher historical range of 2.5 However, not to the degree we saw from 2005-2008. million listings. Today, we stand at 1,310,000 active listings.

The lack of sellers is also a demand problem and what we saw after June of 2022 is that sellers called it quits earlier and faster in the year than usual, resulting in total existing home sales totaling 5,030,000 to end 2022. So the fact that we are back to an average of 26 days on market makes me happier.

However, what is different this year from 2023 is that we have more sellers that will be buyers. Of course, the housing market didn’t have the credit sales boom it had from 2002-2005, but it lacked inventory. Just as they did in 2023, higher rates took the winds out of the growing sales numbers.

It’s also driven more by mortgage buyers who tend to be older and make more money than the new-home buyers. Compared to the existing home sales marketplace, it doesn’t have a high cash buyer or investor buyer profile. Like home sellers, they try to make as much money as possible. percent (±11.9 percent (±13.7

They don’t ever have to have the conversation about how low their total payment is in the new home they’re buying, unlike some of their buyers (which explains higher cancellation rates). If sales are working from an elevated number, like what we saw from 2003-2005, it’s a different subject altogether.

Similarly, companies like Zillow and Trulia launched in 2005 and 2006 as “real estate search engines” to help buyers more easily find a home online. Having everything in-house enables iBuyers to lower closing costs for buyers and sellers, offer real-time, 24/7 customer support and provide unique financing solutions for buyers.

The writer in the Economist says, “…either the fat fee [real estate commission] inflates the house price, or the buyer ends up paying a similar fee when he or she sells.” This is from the Editorial Board of The Wall Street Journal, “Ninety percent of transactions offer buyer agent commissions of exactly 3%.”

NAR Research : First-time buyers were responsible for 28% of sales in October; All-cash sales accounted for 26%; Individual investors purchased 16%; Distressed sales represented 1% of sales; Properties typically remained on the market for 21 days in October. Now we are getting the call back to balance, which is good.

NAR: First-time buyers were responsible for 28% of sales in March; Individual investors purchased 17% of homes; All-cash sales accounted for 27% of transactions; Distressed sales represented 1% of sales; Properties typically remained on the market for 29 days. million before we saw the massive stress spike in supply from 2005 to 2007.

I understand that grifters have to keep the grift going, but not even the Joker would say that the housing market lives off investors and not mortgage buyers. As you can see below, we don’t have a booming credit housing market as we saw from 2002-2005; we have steady replacement buyer demand.

Demand driven by demographics is different than demand driven by mortgage finance innovation and “fix-and-flip” home buyers, as was the case in the mid-2000s. The only period when the median sale price was greater than house-buying power was from 2005 through 2007, indicating an overvaluation of housing, or a “housing bubble.”

Round one with the DOJ According to an antitrust lawsuit the DOJ filed against NAR in September 2005, the hesitancy and suspicion some brokers expressed over moving MLS listings online led to the creation of NAR’s “Initial VOW Policy.” You can also potentially increase your business by marketing your services to off-MLS sellers.”

Buyers have fewer choices than normal in the past eight years — but in reality, since 1982. Homebuilders are efficient sellers of homes because it’s like a commodity to them; they don’t have to look for shelter after they sell or have a 3% mortgage rate they have to give up after they sell. months and above.

The new home sales market doesn’t have a 28% cash-buyer profile as we saw in the last existing home sales report. So, while cash buyers as a percent of sales have been growing, this sector is driven by mortgage buyers primarily. Builders have to find buyers for canceled homes, then think about their demand.

As we can see in the chart below, it’s not like the new home sales market is booming at all; we aren’t anywhere near the top of sales in 2005 or in 2020. percent (±15.2 percent)* above the revised February rate of 623,000, but is 3.4 percent (±12.7 percent)* below the March 2022 estimate of 707,000. When did this all happen?

Logan Mohtashami: Rising rates make housing less affordable, so for a first-time home buyer that doesn’t have the benefit of selling their home with that nested equity, it makes it harder for them. This is much different from the marketplace we saw from 2002-2005, a massive credit bubble. months on a 3-month average.

The truth here that nobody wants to talk about is that we didn’t have a massive sales credit boom in housing from 2020-2021 like we saw from 2002-2005. We must remember that the builders don’t operate like existing home sellers; they treat their products as commodities.

We have to remember that a conventional seller is usually also a traditional buyer, so new listings growing toward their seasonal peak throws cold water on the idea that no one will list their homes because they already have a low mortgage rate (the mortgage rate lockdown theory). didn’t go into recession until 2008.

Inventory falling again in 2022 created more forced bidding wars, which frustrates buyers, keeps potential sellers from wanting to list, and creates stress for real estate agents doing a lot of work with nothing to show for it. We will see if we get some more buyers with the seasonal rise in inventory every year.

Sears Real Estate has been serving buyers and sellers since 1971, under the influential leadership of the late Paul Sears. Elected as president of the REALTOR® Association of Pioneer Valley in 2005, Kevin chaired numerous committees. The brokerage is one of the most recognized brokerages in the area and continues to thrive.

And has quickly became a key figure, known for her expertise with buyers, sellers, and investors. Accordingly , Lisa was named a real estate All-Star in the Northshore Magazine for being able to expertly assist both buyers and sellers on the North Shore. Cyn di thrives to make her buyers and sellers her top priority.

“Our goal is always to make our clients as appealing as possible to a seller to help increase their conversion of getting their offer accepted. trillion in cash-out refis in 2021, up 20% compared to the prior year, the highest volume since 2005. ” Others that leaned purchase in 2021 included depository U.S. .”

In it I included a year over year chart of all sales through the local MLS back to 2005. This information clearly shows a declining trend from the 2005 data down to a low point between 2009 and 2011. Buyers, sellers, and the Realtors who work with them are adaptable, and some transactions have continued via virtual showings.

is skilled in many facets of real estate including both Buyer & Seller Representation, Commercial, Investment, Relocation & Luxury Properties. Licensed in NH since 2005 and MA since 2007, she brings a deep passion for real estate, a strong work ethic, and expert market knowledge. To learn more about her, click here.

The rising rates over the past 16 months have decelerated the number of sales as buyer affordability has been greatly diminished and because sellers are hesitating to list. Listing essentially requires sellers to trade in their pandemic-era rates of 2-3% for the current rates hovering in the high 6%-low 7% range.

It kept inventory down, which propped up prices, but sales are down nearly 22%, and buyers are hungry. Some of that had to do with buyers feeling the affordability crunch of higher interest rates and still-rising prices. 2023 produced the lowest number of home sales since 2005 with the exception of 2011. Sales Decline by 21.7%

Inventory of homes listed reached a record low by July of 2023 , and mortgage rates increased dramatically, diminishing buyer affordability. Many sellers are holding the line, and buyers continue to face competition. The result is buyers are still faced with some of the highest monthly mortgage payments in history.

It was the year of the frustrated buyer, particularly in the first half of the year. The inventory of homes for sale and the number of homes being listed for sale were not nearly enough to satisfy the buyer demand. Remember only one offer can win so this caused lots of disappointment for both buyers and buyer’s agents alike.

It’s the best example of how supply and demand determine the market climate in that with high demand and low supply the market becomes a frenzy for buyers. Below is a graph that illustrates home sales per year since 2005. Below is a graph that illustrates monthly home prices since 2005. It has more to do with buyer consumption.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content