This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The March gain is also the largest since December 2005 and is one of the largest in the index’s 30-year history, said Craig Lazzara, managing director and global head of index investment strategy at S&P DJI. This demand may represent buyers who accelerated purchases that would have happened anyway over the next several years.

The housing market got some much needed relief in the fall when mortgage rates began to drop, but it was short lived. Despite two interest rate cuts by the Federal Reserve, mortgage rates rose again and remain stubbornly high. Its unpredictable, said Teena Jackson, a Redfin agent in Cincinnati.

Buyers who were fortunate enough to snag an available single-family home – new listings are down 46% from a year ago – paid a premium. year-over-year in January, the most growth in a single year since 2005. In Los Angeles, the share of income required to pay a mortgage swelled to 44%. Overall, home prices grew 11.6%

Tuesday’s housing starts report clearly shows that homebuilders are going to be done with single-family construction until mortgage rates fall. Currently, we are in a much different housing recession than what we had from 2005-2011. The credit cycle looks much different now than the build-up from 2002-2005.

Swiss bank UBS Group AG has decided to sell Credit Suisse ’s mortgage servicing company, Select Portfolio Servicing (SPS), to a group of investors led by Sixth Street , HousingWire has learned. Bloomberg first reported on the buyers’ names based on anonymous sources. Credit Suisse acquired SPS in 2005 but was rescued by UBS last year.

The average 30-year fixed-rate mortgage fell four basis points from the week prior to 2.98%, according to data released Thursday by Freddie Mac ‘s PMMS. Within the past almost three months, mortgage rates have only peaked above 3% one time. More recently, however, mortgage applications dipped 6.9%

Since the weaker CPI data was released in November, bond yields and mortgage rates have been heading lower. The question then was: What would lower mortgage rates do to this data? However, mortgage rates have fallen more than 1% since the recent highs, so it’s time to look at the data to explain how to interpret it.

mortgage rate remained essentially unchanged last week, rising by just one basis point to 3.18%, according to Freddie Mac’s Primary Mortgage Market Survey. Overall, homebuyer demand slipped from 25% above pre-COVID levels at the start of the year, when mortgage rates hit record lows, to 8% above pre-COVID levels recently. “We

The housing sector — especially real estate and mortgage — has seen significant layoffs , while the general economy will create more than 4 million jobs in 2022. Then we had the biggest mortgage rate shock in recent history and yet even with that, we will have over 5 million total home sales this year. Production falls. Home sales.

9, when mortgage rates started to fall from 7.37% to 5.99%. In 2022, it was all about affordability as mortgage rates had a historical rise. Even though mortgage rates were falling in November and December, positive purchase application data takes 30-90 days to hit the sales data. Year-over-year, sales fell 22.6% (down from 5.92

But its exacerbated by the rapid rise in mortgage rates over the last three years. Many California homeowners are locked in not just by low property taxes, but by low mortgage rates. Mortgage rates hovered between 3% and 5% from 2010 to the start of 2022, dropping to a record low of under 3% at the height of the pandemic moving frenzy.

UMortgage , a growing nationwide mortgage platform, announced last week the addition of MC Mortgage Group to its network. MC Mortgage Group, a mortgage brokerage based in Wilmington, North Carolina, serves homebuyers across North and South Carolina.

After 2010, qualified mortgage laws were in place, meaning everyone getting a mortgage has to be able to repay the loan. You can see the drastic change this made in the Mortgage Bankers Association Credit Availability index , below, which skyrocketed in 2005 and 2006 before an epic collapse in 2008.

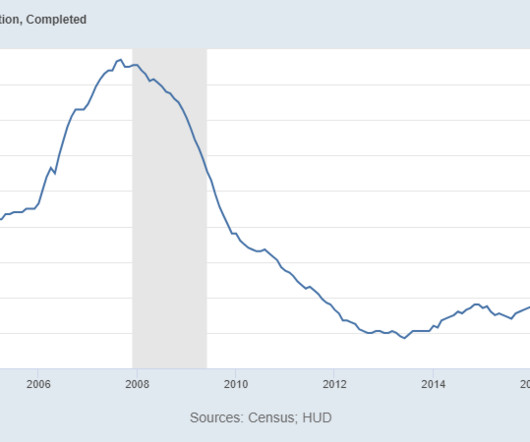

However, the sting of higher mortgage rates is hitting the single-family construction data, and the real story is that the housing completion data, which has been bad for a long time, is still terrible. We simply cannot finish homes in America promptly, and now that mortgage rates are over 5%, some buyers won’t be able to purchase a home.

That belief, however, assumes that one does not understand the two main drivers of housing: demographics and mortgage rates. As it happens, these fabulous demographics are accompanied by the lowest mortgage rates ever recorded in history. All that other stuff, my friends, is just stamp collecting.

No, this is not a new home sales housing bubble as we are far from total new home sales being where they were in 2005. Compare today’s housing market with that in 2018, when mortgage rates were heading toward 5% and monthly supply went above 6.5 The new home buyer is older and makes more money than a traditional existing home buyer.

We finally got mortgage rates to rise, and for people like me who have been concerned about how unhealthy the housing market was last year — and it got a lot worse this year — it’s a blessing that was much needed. million line in the sand has been this: Home prices grow above that 23% level: check Mortgage rates spike higher: check.

But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. In the summer of 2020, I talked about how the housing market would change, but it needed the 10-year yield to break over 1.94%, which roughly means 4% plus mortgage rates.

million existing home sales in 2021, the most recorded in a single calendar year since 2005 and a 21.1% ” Tucker added that record-low mortgage rates are keeping buyers coming to the table – despite rising prices. Approximately 5.6 million existing homes were sold in 2020, a 5.3% Zillow predicts 6.82

Imagine if mortgage rates didn’t rise this year. We are still showing double-digit home-price growth trends in the recent data as it takes time for higher mortgage rates to really increase supply back to normal levels. Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005.

housing market is more tied to mortgagebuyers. Unlike those two cities in Canada, we aren’t as reliant on foreign buyers to such a great extent. foreign buyers have always been less than 300,000 of total home sales for many years. When mortgage rates rise, two things always happen here in America. Here in the U.S.,

We see hints of this delayed home sales shift in the Mortgage Bankers Association’s purchase application data. Because housing demand is at pre-cycle highs, we can infer home prices are not an issue for most buyers. nominal home price growth every year for the next several years, affordability will be an issue for some buyers.

According to a new CoreLogic study , a decrease in affordability has resulted from the simultaneous rise in mortgage rates and housing prices in the U.S. A percentage point increase in the mortgage rate results in increased monthly payments and extra expenses for homebuyers. in May 2024, the highest amount so far this year.

We’ve all been wondering what 5% plus mortgage rates would do to the hot housing market, and now we’ve got that and a bag of chips. As a result, I’ve been rooting for mortgage rates to rise to create a balancing impact on this housing market. 2018 was the last time mortgage rates got to 5%, and sales trended from 5.72

They did not provide information related to the buyers’ names or the financial details. According to Inside Mortgage Finance (IMF), SPS was the 20th-largest U.S. primary mortgage servicer at the end of June, handling $166.7 mortgage unit that focused on “to-be-announced” (TBA) trading. servicing business. In the U.S.,

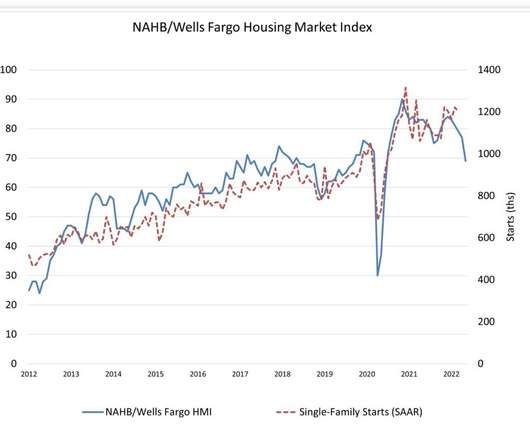

The smart thing to do is go with the builder sentiment trend until it reverses, and most likely, we will need to see lower mortgage rates for that to happen. Some buyers had to wait forever before they could lock in their rate, meaning they didn’t qualify for their homes as rates moved up so fast.

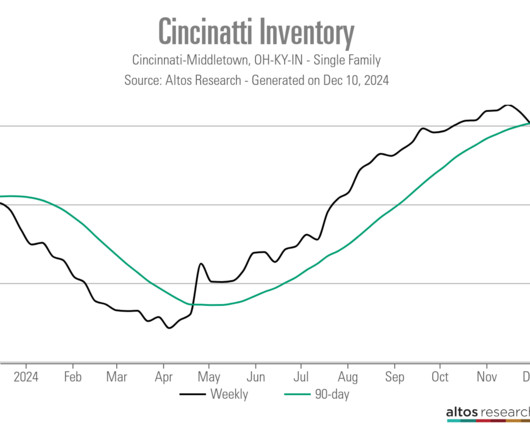

As the 10-year yield broke above 1.94% and mortgage rates rose, we saw the impact on housing data. That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. Credit stress was evident from 2005 to 2008. It’s an excellent time to discuss housing inventory. What is going on here?

The new home sales market is doing well as it really benefits from lower mortgage rates. Good housing demographics, housing tenure at 10 years and low mortgage rates are a perfect recipe for unhealthy home-price growth. The majority of home buyers in America buy homes to live in, not for an investment. higher than a year ago.

Though the desire for buyers to purchase a new home remains strong, skyrocketing prices are putting the dream out of reach for some buyers, economists in the housing industry said. May’s 8% increase was the highest jump for that month since 2005, according to NAR. Mortgage applications increased 5.7% from June 2020.

Low mortgage rates and incredible buyer demand won out over pressure from soaring lumber prices in March as single-family new home sales rose 20.7% With so many buyers snatching up new homes at the ready, inventory fell to 3.6 As long as mortgage rates stay low the builders are going to be fine.” Census Bureau.

Buying a house was obtainable only for the haves in 2023 as home prices and mortgage rates soared. Buyers offer higher down payments to offset steep borrowing costs Overall, the typical down payment was 8% for first-time buyers and 19% for repeat buyers — the highest share since 1997 and 2005, respectively.

We don’t have a massive credit boom as purchase application data is at historical lows; we haven’t had the same run-up in credit as we saw from 2002-2005. You would need years of credit stress building up, as we saw in 2005-2008, all before the job loss recession data. Mortgage rates moving up and down have moved the market.

And the peak in existing home sales was 2005 when you had around 7 million transactions.” That’s what I think is invariably going to happen because you’re going to have more seniors, the silver tsunami, selling and there are fewer buyers so the give is going to be lower home prices.” homeowners.

home prices are quickly shifting the affordability calculus for prospective homebuyers in 2021 — even though mortgage rates have remained near record lows. Despite average 30-year mortgage rates that have remained below 3% for most of 2021, the rapid home price increases are eroding affordability for average wage earners.

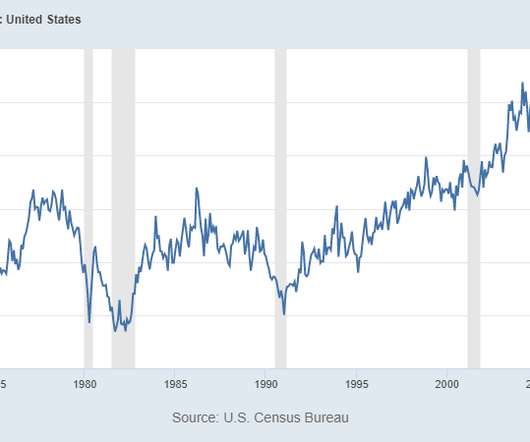

NAR total active listings data going back to 1982 : This explains why the builders and new homes are doing better than the existing home sales market, which deals with higher mortgage rates and low active listings. Also, in the chart below, we can all agree it isn’t housing 2005 or housing 2008 with new home sales.

Consolidation in the mortgage industry is likely in 2022, analysts and lending executives said. Justin Woodward has experienced the best and the worst of the mortgage industry in only 18 months. “I had not done first mortgage lending before, but I was familiar with the basics of real estate lending.

Pending home sales reached its highest mark for the month of May since 2005, up 8% from the previous month of April as low inventory continues driving buyers to snatch up available real estate. “Buyers are still lining up a feverish pace,” Yun said. “Buyers are still lining up a feverish pace,” Yun said.

. “The principal factor was the rapid increase in mortgage rates, which hurt housing affordability and reduced incentives for homeowners to list their homes. ” One of the housing economic realities that I have been trying to stress this year is that a traditional seller of a home is typically a buyer as well.

Tuesday’s new home sales report missed expectations and had negative revisions, which isn’t surprising given this sector of our economy simply can’t handle higher mortgage rates. can’t have a credit sales boom like we saw from 2002-2005. Over the years, I have tried to emphasize that the housing market in the U.S.

9 up until the early part of February as mortgage rates fell from 7.37% to 5.99%. They don’t ever have to have the conversation about how low their total payment is in the new home they’re buying, unlike some of their buyers (which explains higher cancellation rates). Suppose mortgage rates had broken below 5.75%.

When mortgage rates fall, the majority of homebuyers (including homeowners who need to sell to buy another home) are mostly employed, so lower rates greatly benefit them, and housing demand increases. So when you add move-up buyers, move-down buyers, first-time homebuyers, cash buyers and investors together, this can get out of hand.

However, considering Wednesday’s builder confidence index and mortgage rates over 6%, it’s time to raise the fifth recession red flag, since the builders will have a tough time growing housing starts with rates this high. . As rates rise, this will impact the builders more as they try to find buyers for current homes in cancellation.

From NAR : “December was another difficult month for buyers, who continue to face limited inventory and high mortgage rates ,” said NAR Chief Economist Lawrence Yun. However, expect sales to pick up again soon since mortgage rates have markedly declined after peaking late last year.” Also, this is what the Federal Reserve wants.

years in 2005, according to a Redfin analysis of median U.S. Older Americans also have financial incentives attached to staying in their homes, since 54% of the baby boomer cohort own their homes free and clear without making monthly mortgage payments. years last year, up from 6.5 homeowner tenure by year using county records.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content