This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

The March gain is also the largest since December 2005 and is one of the largest in the index’s 30-year history, said Craig Lazzara, managing director and global head of index investment strategy at S&P DJI. This demand may represent buyers who accelerated purchases that would have happened anyway over the next several years.

Buyers who were fortunate enough to snag an available single-family home – new listings are down 46% from a year ago – paid a premium. year-over-year in January, the most growth in a single year since 2005. Buyers are paying the price appeared first on HousingWire. In nearly three quarters of the 100 largest U.S.

Ive been doing this since 2005 and I tell clients that Ive never seen a market like this, so we have to navigate it together. Relatively more homes for sale are giving buyers more leverage, as evidenced by Altos Researchs Market Action Index score falling from 55 in May to 45 today. It’s just become a more common theme.

But relief for buyers could be coming in the next 12 months. gain by this time next year, as ongoing affordability challenges deter potential buyers — as well as an uptick in new for sale listings. May’s 8% increase was the highest jump for that month since 2005, according to NAR. Home prices increased 2.3% ” The 17.2%

The housing market of 2002-2005 had four years of sales growth facilitated by credit. As we can see below, the purchase application data had four years of growth, peaking in 2005 and then collapsing. However, what isn’t identical is that we have not had a massive sales boom like we saw from 2002-2005. million in 2005.

Bloomberg first reported on the buyers’ names based on anonymous sources. servicing business without naming the buyers or disclosing the financial details. Credit Suisse acquired SPS in 2005 but was rescued by UBS last year. Investment firm Davidson Kempner Capital Management is a co-investor.

Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. The housing market can’t replicate the type of massive credit expansion we saw from 2002-2005, so the price-growth story has more to do with inventory collapsing to all-time lows. This is because the biggest buyers of homes are mortgage buyers.

You can see the drastic change this made in the Mortgage Bankers Association Credit Availability index , below, which skyrocketed in 2005 and 2006 before an epic collapse in 2008. Since most sellers are buyers, inventory should be stable if demand is stable. Demographics also play a role here.

No, this is not a new home sales housing bubble as we are far from total new home sales being where they were in 2005. The monthly supply of new homes was mostly higher every month in the previous expansion (2008-2019) than any period from 1996-2005. At that time, the new home sales sector got so bad that I put it in the penalty box.

Of course, housing starts today aren’t collapsing in the way they did from the peak of 2005 because we haven’t had a sales credit boom in recent years as we did from 2002-2005, which inflated new home sales toward 1.4 Currently, we are in a much different housing recession than what we had from 2005-2011.

The second part of this story that folks seem to forget is that the existing home sales market only needs 4 million mortgage buyers a year to remain stable. Note too, that the housing market for the last many years has been composed of 15-20% cash buyers – that is a big chunk of buyers that don’t need a mortgage in order to purchase.

But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. This time around, we have not seen the kind of housing credit boom that we did from 2002-2005. Purchase application data is now below 2008 levels! This means less demand for housing.

housing market is more tied to mortgage buyers. Unlike those two cities in Canada, we aren’t as reliant on foreign buyers to such a great extent. foreign buyers have always been less than 300,000 of total home sales for many years. from 2002-to 2005, which led to forced credit selling. In addition, the U.S.

years in 2005, then tenure gradually increased over the next 15 years. Long homeowner tenure is an obstacle for first-time buyers all over the country, not just in California, because it contributes to the countrys housing shortage and pushes sale prices higher. The typical homeowner stayed put for 6.5

That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. However, the spike in inventory that we saw from 2006 to 2011 can be attributed to the massive credit bubble we had from 2002 to 2005. Credit stress was evident from 2005 to 2008. What is going on here?

million existing home sales in 2021, the most recorded in a single calendar year since 2005 and a 21.1% ” Tucker added that record-low mortgage rates are keeping buyers coming to the table – despite rising prices. Approximately 5.6 million existing homes were sold in 2020, a 5.3% increase from 2019, according to officials.

Because housing demand is at pre-cycle highs, we can infer home prices are not an issue for most buyers. nominal home price growth every year for the next several years, affordability will be an issue for some buyers. However, this does not mean that real home prices may grow at an unhealthy pace in the years 2020-2024.

Mark Willis, who served as CEO of Keller Williams from 2005 to 2014, has stepped back into the role effective immediately. In 2002, he joined the firm’s executive team, serving as president, before a nine-year stint as CEO from 2005 to 2014. Marc King will continue to serve as President of Keller Williams. He left the company in 2016.

Some buyers had to wait forever before they could lock in their rate, meaning they didn’t qualify for their homes as rates moved up so fast. We never saw the credit sales boom as we did from 2002-2005, so the builders themselves are in a better position to manage their future. This data line is already below 2008 levels currently.

Pending home sales metrics released by the National Association of Realtors on Wednesday revealed pending home sales reached its highest mark for the month of May since 2005, up 8% from the previous month of April. More recently, however, mortgage applications dipped 6.9% last week, according to data from the Mortgage Bankers Association.

“In a still-competitive housing market, more well-off home buyers were able to have their bids accepted by offering larger down payments and even by paying cash.” However, a significant majority of buyers (80%) financed their home purchase in 2023, up from 78% in 2022 but still down from 87% two years ago, according to the survey.

Because housing is becoming an outperforming asset, we may see an increase in cash buyers in 2021 as a percent of sales. The majority of home buyers in America buy homes to live in, not for an investment. This is the big difference between the housing market now and what we saw in 2002-2005, when we saw a lot of speculation going on.

However, we haven’t had a credit sales boom like the one we saw from 2002-2005. Total Inventory had been growing from 2001-2005; total listings data in 2005 was at the higher historical range of 2.5 However, not to the degree we saw from 2005-2008. million listings. Today, we stand at 1,310,000 active listings.

Low mortgage rates and incredible buyer demand won out over pressure from soaring lumber prices in March as single-family new home sales rose 20.7% With so many buyers snatching up new homes at the ready, inventory fell to 3.6 from February to a 1.02 Census Bureau. This is the fastest sales pace since September 2006.

Pending home sales reached its highest mark for the month of May since 2005, up 8% from the previous month of April as low inventory continues driving buyers to snatch up available real estate. “Buyers are still lining up a feverish pace,” Yun said. “Buyers are still lining up a feverish pace,” Yun said.

This means new homes — with all the bells and whistles — can peel some buyers from the existing home sales market, especially if they pay down mortgage rates. Also, in the chart below, we can all agree it isn’t housing 2005 or housing 2008 with new home sales. Now on to the report.

They did not provide information related to the buyers’ names or the financial details. SPS, bought by Credit Suisse in 2005, announced a deal in September 2022 to acquire some of the assets of Texas-based Rushmore Loan Management Services. servicing business. In the U.S., Credit Suisse owns Select Portfolio Servicing (SPS).

can’t have a credit sales boom like we saw from 2002-2005. This means we won’t be working from record-breaking demand of high sales like we did at the peak of 2005. The builders are in a better position to manage their inventory glut than when they were working from a credit boom in 2005 that took new home sales up to 1.4

Though the desire for buyers to purchase a new home remains strong, skyrocketing prices are putting the dream out of reach for some buyers, economists in the housing industry said. May’s 8% increase was the highest jump for that month since 2005, according to NAR. The overall pending home sales index fell 1.9% in 2022.

Patrick Stoy , president of MC Mortgage Group, established the brokerage in 2005 and brings with him 24 years of experience in the housing industry. MC Mortgage Group, a mortgage brokerage based in Wilmington, North Carolina, serves homebuyers across North and South Carolina.

And the peak in existing home sales was 2005 when you had around 7 million transactions.” That’s what I think is invariably going to happen because you’re going to have more seniors, the silver tsunami, selling and there are fewer buyers so the give is going to be lower home prices.” homeowners.

Homes remain much more affordable in 2021 than they were during the home price runup in 2005 and 2006, but the seven-month trend in deteriorating affordability is starting to gradually slow demand. Auction.com buyer Steve Johnson purchases and renovates distressed homes in Georgia and Tennessee. Homebuyers Losing Heart.

As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. What I mean by a credit bust is that after the housing bubble burst in 2005 into 2006, we saw a massive increase in supply. Total inventory levels. NAR: Total Inventory levels 1.22

a record low in the series dating back to 1963, while the share of homes sold-but-not-yet-started was at a level only seen during the housing bubble in 2005.” Eager buyers have been snapping up available new homes, an increasing share of which have not even begun construction, at their highest pace in years.

We don’t have a massive credit boom as purchase application data is at historical lows; we haven’t had the same run-up in credit as we saw from 2002-2005. You would need years of credit stress building up, as we saw in 2005-2008, all before the job loss recession data. This is not, nor can it ever be, like 2008.

“This is confirmation that while purchase demand remains strong, the marginal buyer is feeling the affordability squeeze resulting from the increases in mortgage rates and home prices we’ve experienced in recent months.”. The housing market is in desperate need of more inventory to cool price growth and preserve affordability.

” One of the housing economic realities that I have been trying to stress this year is that a traditional seller of a home is typically a buyer as well. This means what we saw in 2005-2008 with the inventory spike was a historic event that hasn’t been replicated at any time in recent U.S. economic history. .

“Across the United States, homebuilders reliably broke ground on between 125,000 and 140,000 homes almost every month in 2021, and by one common measure, last year was the second-least volatile year for housing starts since 2005.”. Overall, an estimated 1,595,100 housing units were started in 2021, a 15.6% increase from 2020.

NAR Research : First-time buyers were responsible for 29% of sales in February; Individual investors purchased 19% of homes; All-cash sales accounted for 25% of transactions; Distressed sales represented less than 1% of sales; Properties typically remained on the market for 18 days. We have solid replacement buyers: people needing shelter.

From NAR: First-time buyers were responsible for 27% of sales in January; Individual investors purchased 18% of homes; All-cash sales accounted for 28% of transactions; Distressed sales represented 2% of sales; Properties typically remained on the market for 34 days. Also, the days on market are on a level they might feel more comfortable in.

years in 2005, according to a Redfin analysis of median U.S. Long homeowner tenure, particularly among baby boomers, is an obstacle for young first-time buyers trying to break into the market,” the report read. “A years last year, up from 6.5 homeowner tenure by year using county records.

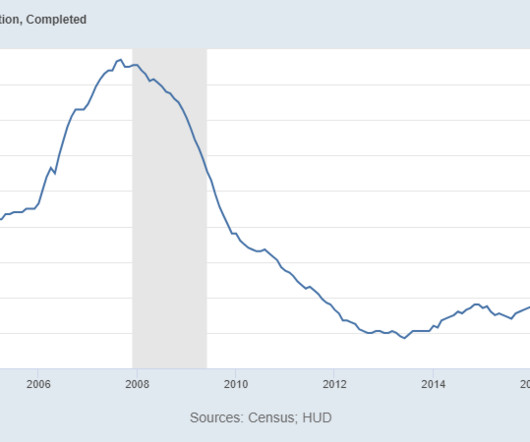

As rates rise, this will impact the builders more as they try to find buyers for current homes in cancellation. As you can see below, housing completion data hasn’t done much for many years, unlike 2002-2005. But, this data line should grow a tad more while they finish up homes that they do have buyers for.

They don’t ever have to have the conversation about how low their total payment is in the new home they’re buying, unlike some of their buyers (which explains higher cancellation rates). If sales are working from an elevated number, like what we saw from 2003-2005, it’s a different subject altogether.

The goal of the expansion is to provide homeowners and buyers, along with real estate, legal, and tax professionals, the option to order an appraisal directly through Opteon’s services, according to a statement from the company. Opteon, founded in 2005, operated in Australia and New Zealand before expanding into the U.S.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content