This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Thats the highest share for new sales since 2005, which was during the building boom driven by cheaper housing, looser credit requirements and high demand for mortgage-backed securities. The existing-home sales slump coupled with a strong tally of new sales has resulted in new-home sales accounting for 14.4% of all transactions.

increase from 2005. From 2005 to 2023, single family homes increased by only 16.7%, with annual expansions remaining below 1%. Today, Texas leads the nation in housing inventory growth, with 15 cities in the top performers in housing stock increases from 2005 to 2023. In 2023, total inventory hit 144 million housing units, a 16.7%

trillion in cash-out refis in 2021, up 20% compared to the prior year, the highest volume since 2005. in 2021, highest level since 2005 appeared first on HousingWire. Record home prices in recent years have pushed tappable home equity to new heights, increasing the demand for one specific product: cash-out refis.

The March gain is also the largest since December 2005 and is one of the largest in the index’s 30-year history, said Craig Lazzara, managing director and global head of index investment strategy at S&P DJI. ” The post Home prices haven’t risen this fast since 2005 appeared first on HousingWire. In fact, they rose 13.2%

Census Bureau data to analyze housing inventory changes across 489 cities between 2005 and 2023. from 2005 to 2023 — the lowest inventory increase among all property types. McKinney — located in the Dallas area — had the fastest-growing middle housing inventory among the cities analyzed at 185% from 2005 to 2023.

March’s year-over-year gain in home prices had not been exceeded since December 2005, The post Home Prices Saw Largest Annual Gain Since 2005 as Affordability Concerns Rise appeared first on Appraisal Buzz.

Founded in 2005, My Home Group has been recognized on the Inc. “Arizona’s real estate market presents significant opportunities, and My Home Group’s agent-focused approach aligns seamlessly with Fathom’s culture. 5000 list of the nation’s fastest-growing companies for seven straight years.

Platinum arrived on scene in 2005 and is now one of the largest independent residential brokerages in the Midwest. . “And then we know that if you are going to be successful, you have to persist in the face of challenges, and we know that together we can make all that happen.”

The housing market of 2002-2005 had four years of sales growth facilitated by credit. As we can see below, the purchase application data had four years of growth, peaking in 2005 and then collapsing. However, what isn’t identical is that we have not had a massive sales boom like we saw from 2002-2005. million in 2005.

There are several important reasons why the market today is materially different then the bubble-forming market of 2005. From 2002 to 2005 we experienced a credit boom due to the rapid increase in borrowing for speculation purchases. Speculation demand.

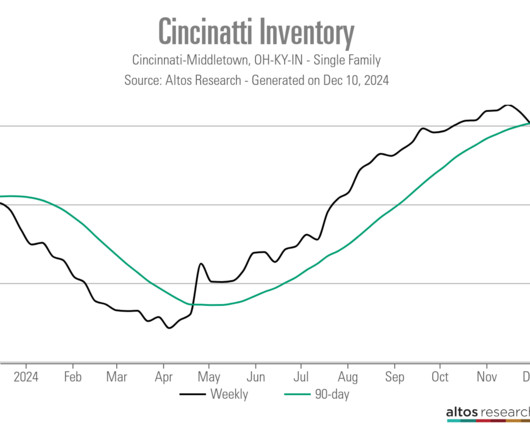

Ive been doing this since 2005 and I tell clients that Ive never seen a market like this, so we have to navigate it together. The turbulence in rates has trickled down to individual markets like Cincinnati, where real estate agents say they dont know what to expect from sale to sale.

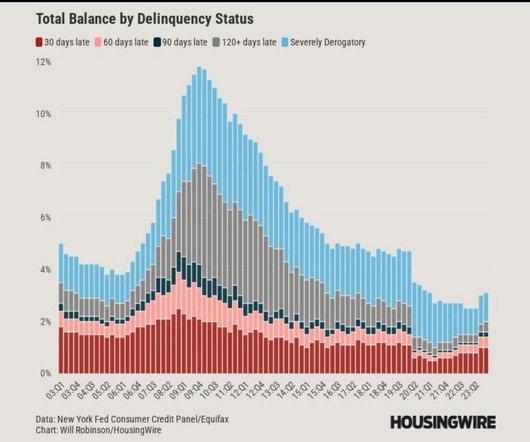

One of the unsung heroes of the most prolonged economic and job expansion ever recorded in history was the passing of the 2005 Bankruptcy Reform Act and the 2010 qualified mortgage rule under Dodd-Frank. As we can see below, the bankruptcy levels were extremely high before the bankruptcy law was passed in 2005. Today, we are at 1.25

This typically happens in a recession, however, the notion that credit lending in America will collapse as it did from 2005 to 2008 couldn’t be more incorrect, as we haven’t had a credit boom in the period between 2008-2022. Because credit got better post-2010, we can see credit availability declines from 2005-2008. Why is this?

trillion in 2005 — but sees refinances decreasing to $971 billion. trillion, the highest since 2005. The rebounding economy is also likely to mean higher mortgage rates , with the MBA forecasting 2.9% by the end of 2020, rising to 3.3% by Q4 2021. MBA is forecasting a rise in purchase originations to $1.59 That includes an expected 91.5%

Because of the qualified mortgage laws of 2010, we are lending to the capacity to own the debt, which means speculative credit cycles from primary resident homebuyers or even investors can’t occur in the same fashion as from 2002-2005. We don’t have a rise in foreclosures as we did from 2005-2008 before the job-loss recession.

Of course, housing starts today aren’t collapsing in the way they did from the peak of 2005 because we haven’t had a sales credit boom in recent years as we did from 2002-2005, which inflated new home sales toward 1.4 Currently, we are in a much different housing recession than what we had from 2005-2011.

from 2005 to 2006, then another 22.4% in unit sales from the peak of 2005 to the trough of 2008. While we generally understand that the unit sales of 2003 to 2005 were fed by fraudulent mortgage activities; nonetheless, unit sales in the record year of 2021 were only 4.1% from 2006 to 2007 and another 20.9% from 2007 to 2008.

That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. However, the spike in inventory that we saw from 2006 to 2011 can be attributed to the massive credit bubble we had from 2002 to 2005. Credit stress was evident from 2005 to 2008. What is going on here?

housing credit looks very different than in 2005, 2006, 2007 or 2008. Bankruptcies and foreclosures After 2010, the qualified mortgage laws came into play and all the exotic loan debt structures in the system, especially in the run-up in demand from 2002 to 2005, disappeared. The truth is, U.S.

But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. This time around, we have not seen the kind of housing credit boom that we did from 2002-2005. Purchase application data is now below 2008 levels!

I’m going to take their talking points and explain in detail why this isn’t the housing bubble of 2002-2005. “ Over the years, I have tried to express that we won’t have a repeat of 2002-2005 when it comes to a speculative mortgage debt expansion on unsound credit. Our evidence points to abnormal U.S.

First, purchase applications in the data should be skyrocketing as they did during the 2002-2005 ill-considered, home-buying extravaganza. If the housing market was in the grips of some mass hysteria of irrational purchasing, we would expect to see certain hallmarks in the data.

As you can see in the chart below, we had a nice, slow up-trend from 2002 to 2005 and here in the 2020 to 2022 timeframe, we haven’t gone anywhere much with total completion data. Back in 2005, new home sales were so elevated from exotic loan debt structures that the collapse in sales was truly epic.

We can see a slow and steady positive downtrend in stressed financial data, unlike in the 2005-2008 period where people filed for bankruptcies and foreclosures without a job loss recession. This content is exclusively for HW+ members. Start an HW+ Membership now for less than $1 a day.

In 2005, the DOJ filed a lawsuit against NAR claiming that these policies were anticompetitive and harming the upcoming cohort of discount brokerages who were using the internet to provide low-cost brokerage services. Additionally, the listing brokerages were allowed to limit what information could be shared on these websites.

This, combined with the 2005 Bankruptcy Reform law and the most prolonged economic and job expansion in our nation’s history before COVID-19, has created a favorable financial environment for American homeowners. But, we don’t have large numbers of American homeowners that are financially stressed right now.

However, we haven’t had a credit sales boom like the one we saw from 2002-2005. Total Inventory had been growing from 2001-2005; total listings data in 2005 was at the higher historical range of 2.5 However, not to the degree we saw from 2005-2008. million listings. Today, we stand at 1,310,000 active listings.

We never saw the credit sales boom as we did from 2002-2005, so the builders themselves are in a better position to manage their future. We won’t see a sales decline in scale terms as we had from 2005-2008 since we simply have never had that type of sales and credit demand. This data line is already below 2008 levels currently.

This was the case for housing during the lead-up to the bubble years as housing data went criminally insane in the years 2002-2005. Each economic sector behaves differently in a recession; typically, the industry with the most leverage on growth gets hit the hardest.

You can see the drastic change this made in the Mortgage Bankers Association Credit Availability index , below, which skyrocketed in 2005 and 2006 before an epic collapse in 2008. Just look how lousy credit looked below in 2005, 2006 and 2007 — all before the job-loss recession in 2008. Demographics also play a role here.

However, the demand curve of what we have in housing too doesn’t resemble the speculation demand curve of what we saw from 2002-to 2005. So the type of boom and bust we would need to see to reflect bubble speculation demand isn’t in this market like we saw from 2002-to 2005.

Home prices were growing at an unsustainable level from 2002-2005, leading to some excess risk-taking on inadequate loan debt structures. First, the refinance boom’s main driver in the 2000s was unhealthy because of the marketplace’s speculative unhealthy lending standards.

is the highest reading for May since 2005. From the National Association of Realtors : “Pending home sales rose 8% in May from the prior month and 13.1% from one year ago. The May 2021 Pending Home Sales Index of 114.7 Contract signings rose in all regions in May compared to the prior month and one year ago.

Mark Willis, who served as CEO of Keller Williams from 2005 to 2014, has stepped back into the role effective immediately. In 2002, he joined the firm’s executive team, serving as president, before a nine-year stint as CEO from 2005 to 2014. Marc King will continue to serve as President of Keller Williams. He left the company in 2016.

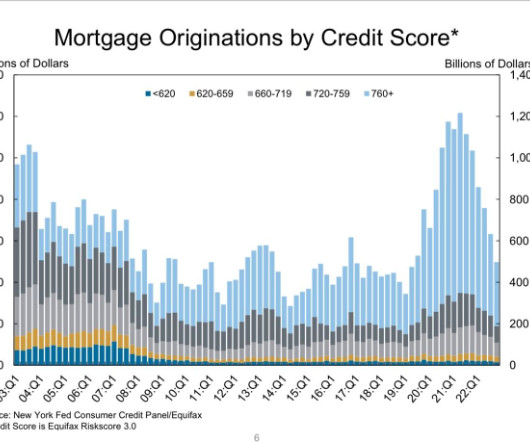

trillion, with the largest refinance market since 2003 and the largest home purchase loan market since 2005 and 2006. According to the Mortgage Bankers Association, mortgage origination volume is expected to reach $3.1

Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. The housing market can’t replicate the type of massive credit expansion we saw from 2002-2005, so the price-growth story has more to do with inventory collapsing to all-time lows. Even today, the MBA purchase application index is below 2008 levels.

In 2005, near the height of the housing boom, almost half of all mortgages were ARMs, which typically meant they had an initial fixed period of five or seven years followed by annual adjustments linked to a benchmark like LIBOR. Treasury’s repo market where investors offer banks overnight loans backed by their bond assets.

No, this is not a new home sales housing bubble as we are far from total new home sales being where they were in 2005. The monthly supply of new homes was mostly higher every month in the previous expansion (2008-2019) than any period from 1996-2005. At that time, the new home sales sector got so bad that I put it in the penalty box.

Just to give you some perspective here, at the peak of 2005, we had about 2.24 Not the case this time around as we haven’t seen the kind of booming sales market like we saw from 2002-2005. Housing construction in the U.S. million housing completions in the monthly report. below the revised July estimate of 1.419 million, but 3.1%

million existing home sales in 2021, the most recorded in a single calendar year since 2005 and a 21.1% Approximately 5.6 million existing homes were sold in 2020, a 5.3% increase from 2019, according to officials. Zillow predicts 6.82 increase from 2020. “[The low rates] are keeping monthly payments in reach,” he said.

Credit Suisse acquired SPS in 2005 but was rescued by UBS last year. Fitch Ratings said in a report that SPS has been servicing residential mortgages since 1989 and residential mortgage-backed securities (RMBS) transactions since 2000. The Swiss bank added SPS to its division that is focused on non-core and legacy businesses.

This is evident if one compares the purchase application data from the overheating market of 2002-2005 to the period between 2012-2020. First the rate of growth in no way compares to what we had during the bubble years of 2002-2005. While sales are and will stay elevated compared the COVID-19 lows, the market is not bubbly.

Willis previously held the top leadership position at Keller Williams Realty from 2005-2015 and had recently rejoined the company in a consulting capacity.

The Southern California brokerage was founded in 2005 by George Penner and Mike Deasy, who will both remain with the firm after it joins the Robert Reffkin -helmed firm. Moving forward, the firm will be known as DPP @ Compass. Compass described the move as a “partnership,” but the financial terms of the deal were not disclosed.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content