This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Newly released data from the annual profile of home buyers and sellers by the National Association of Realtors (NAR) shows just how dramatically this trend has manifested since the financial crisis of 2008. Elevated mortgage rates, sky-high home prices, tight credit and stagnant wages have all contributed to homebuyers getting older.

There’s a showdown at the housing market corral between homebuyers and sellers. This means the housing boom period of 2002-2005 had major credit tightening, which won’t happen this time around when the next recession hits. Home prices ebb and flow, pricing was working in the sense that sellers met homebuyers to a degree.

This rule is no longer in place due to the terms of NAR’s home seller commission lawsuit settlement , which went into effect in August. The suit is seeking class-action status for a nationwide class that is defined as all persons who purchased a residential property listing on a Realtor-affiliated MLS between 2002 and the present.

I am so proud of our network and the professionals that work tirelessly to guide buyers and sellers on their home selling and buying journeys.” ” According to a spokesperson at HomeServices of America, Budnick has no immediate plans for her next steps or role.

The housing market of 2002-2005 had four years of sales growth facilitated by credit. However, what isn’t identical is that we have not had a massive sales boom like we saw from 2002-2005. This is significantly different than the period from 2002-2005 when credit expansion was booming. Home sales. million in 2005.

As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. These were forced credit sellers, which means these sellers don’t sell to buy a home like a traditional seller does. Total inventory levels. NAR: Total Inventory levels 1.22

That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. However, the spike in inventory that we saw from 2006 to 2011 can be attributed to the massive credit bubble we had from 2002 to 2005. If you connect the lines, you can see where we are on a historical basis.

In 2002, Natalya Delcoure and Norman Miller, two real estate economists, set about to learn what fees consumers pay real estate agents in America. They were especially interested in real estate commissions. What Decloure and Miller discovered was somewhat shocking. That’s part two, coming up Thursday.

I know some people don’t agree with me on this, but the price gains in both the existing home and new home sales sector show that homebuilders and sellers had too much pricing power and needed to be checked. As you can see, sales levels were never elevated like what we saw from 2002-2005. The only way this happens is by higher rates.

My concern now is that some sellers are feeling stressed about this market, which should never happen because this is the best seller market ever. However, a seller is also a natural homebuyer, unless they’re an investor. You can see why some sellers are stressed now. People who sell need to live somewhere.

Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. The housing market can’t replicate the type of massive credit expansion we saw from 2002-2005, so the price-growth story has more to do with inventory collapsing to all-time lows. Even today, the MBA purchase application index is below 2008 levels.

However, what is different this year from 2023 is that we have more sellers that will be buyers. Of course, the housing market didn’t have the credit sales boom it had from 2002-2005, but it lacked inventory. Just as they did in 2023, higher rates took the winds out of the growing sales numbers.

The seller is Robert Sarver, managing partner of Suns Legacy Holdings , which owns the Phoenix Suns and Mercury. He was a backup point guard from 1998-2002 and won a national championship. The transaction, which values the Suns and Mercury at $4 billion, first became public in December. The executive acquired both teams in 2004.

The lack of sellers is also a demand problem and what we saw after June of 2022 is that sellers called it quits earlier and faster in the year than usual, resulting in total existing home sales totaling 5,030,000 to end 2022. I have often said that anytime days on the market are at a teenager level, nothing good will happen.

This is why I have called them efficient home sellers. As we can see in the chart below, sales levels aren’t exactly booming like they were from 2002-2005. The builders sell homes as a commodity, and they had a big spike in monthly supply last year, forcing them to make some deals to move product.

Between 2002-2005 in many markets, the real estate market was scorching, much like it is today. As appraisers, we faced tremendous pressure from buyers, sellers, real estate agents, and loan officers during the previous run-up. We are seeing that as a profession again. Is this any different than last time? How do we combat this?

As you can see below, the new home sales market from 2018-2022 doesn’t look like the housing market we had from 2002-2005. Like home sellers, they try to make as much money as possible. First, as you can see from the chart below, the market we had from 2002-2005 never existed in housing from 2014-2022. percent (±11.9

This time around, we have not seen the kind of housing credit boom that we did from 2002-2005. NAR total inventory data 1,250,000 One thing about purchase application data and demand is that a traditional seller is typically a buyer of a home. Post-2012, whenever mortgage rates rise, existing home sales always trend below 5 million.

Frazier also testified that the average commission at ReeceNichols is 2.75% for both buyer and seller agents. According to Frazier, homebuyers working with ReeceNichols agents sign a buyer agreement that if the seller doesn’t pay the buyer agent’s fees, then the buyer will pay the fee themselves. They were guidelines.

One tool I used for a time to level this playing field was seller-funded down payment assistance. In 2002, to protect lenders, I cofounded and organized an industry association called HAND, whose mission was to educate the mortgage industry on the proper utilization of seller funded DPA, and to curb risky practices.

According to Ketchmark, the home sellers paid an average of $6,700 to the buyer’s agent in the transactions, adding up to $1.78 In the script the seller asks the agent if he or she can reduce their commission, stating that they would like to save money. billion in damages. I reported the numbers and walked off the stage.”

The 2002 housing market has been a tale of two halves,” said Green. Temporary rate buydowns have become a popular concession, especially among homebuilders, in which one out of 10 loans feature a seller-paid buydown, said Peter Idziak, senior associate at Polunsky Beitel Green. A mortgage rate lockdown freezes the housing market.

However, we haven’t had a credit sales boom like the one we saw from 2002-2005. One of the issues with existing home inventory has been that, for the most part, a traditional seller is usually a buyer of a home. Nor can we ever have a credit sales boom again with lending standards back to normal. million listings.

A traditional primary resident seller is also a buyer, which means if they don’t list, they’re not just taking a potential home to be bought off the table — they’re taking a future sale off the books as well. However, it’s not the market of 2002-2011. From NAR Research : “Total existing-home sales notched a minor contraction of 0.4%

In fact, while in won’t match 2020 or 2021, purchase mortgage dollar volume should be better than any year from 2002–2020. When mortgage rates come down, homebuyers will come out in droves and it will be a sellers’ market again. Buying now means being able to negotiate as a buyer.

percent)* below the December 2020 estimate of 943,000 Slow and steady wins the race and the market that we had from 2002-2005 doesn’t exist today. This is also a factor why I don’t believe in the housing construction boom premise, because when builders and sellers have pricing power they push it to the limits. This is 11.9

This problem is much different than the housing credit bubble of 2002-2005. Home sellers and builders had too much pricing power, pushing prices to the extreme. After 2021 ended and my price-growth model was broken after only two years and we started 2022 at all-time lows in inventory, I labeled the U.S.

The truth here that nobody wants to talk about is that we didn’t have a massive sales credit boom in housing from 2020-2021 like we saw from 2002-2005. We must remember that the builders don’t operate like existing home sellers; they treat their products as commodities.

As you can see below, we don’t have a booming credit housing market as we saw from 2002-2005; we have steady replacement buyer demand. More choices are better for homebuyers and sellers who need to buy a home typically as well. A positive outcome for me in 2022 would be to see days on the market grow above the teenager age.

can’t have a credit sales boom like we saw from 2002-2005. With housing post-2020, home sellers and homebuilders had a lot of pricing power and pushed it on the consumer because they could. However, this is on them — they had pricing power, and just like home sellers in America, they pushed it to make a lot of money in the short run.

The 30-year fixed-rate mortgage broke 7% for the first time since April 2002, leading to greater stagnation in the housing market,” Sam Khater, Freddie Mac’s chief economist, said in a statement. A year ago at this time, rates averaged 3.14%.

The only thing that I believe creates balance in the housing market is higher rates because the sellers and builders have too much pricing power in this low inventory environment. . This is much different from the marketplace we saw from 2002-2005, a massive credit bubble. The days on the market to sell a home is too low.

Home sellers strive to get the highest price from the best offers and homebuilders have the pricing power over consumers. Since housing tenure is now over 11 years, the built-in equity position is much higher today without a massive credit boom like what we saw from 2002-2005. In short, we made American mortgage debt great again !

The one thing housing has going for it now is that we don’t have the speculative booming demand as we saw from 2002 to 2005. The builders have pricing power and they — along with home sellers — have pushed it very hard since 2020. From Census: The median sales price of new houses sold in March 2022 was $436,700.

Inventory falling again in 2022 created more forced bidding wars, which frustrates buyers, keeps potential sellers from wanting to list, and creates stress for real estate agents doing a lot of work with nothing to show for it. As you can see below, the housing market from 2018 to 2022 doesn’t look like anything we saw from 2002 to 2005.

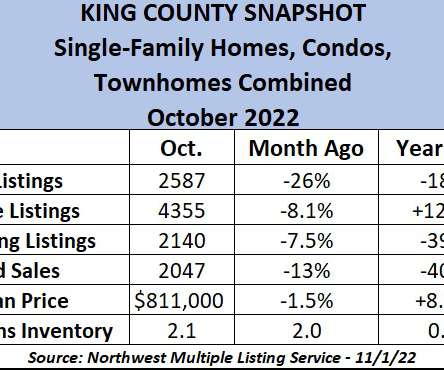

Who said this is a sellers’ market? >> Housing permits for single-family home construction in the Seattle/King County area this year is 49% lower than the peak period of 2002-2008. The sellers were seeking $7.8M ($1527/sq. The post SELLERS’ MARKET? from a year ago and at a level not seen since 2011.

The drop in nearly 4,000 closings wasn’t just because buyers weren’t buying; they would, but many couldn’t because sellers weren’t selling. Sellers find themselves in a holding pattern , desiring to move but hesitant due to the reluctance to part with their low pandemic-era interest rates. Will the 2024 Real Estate Market Improve?

She’s held her real estate salesperson license in Ohio since 2002 and is active in many associations, including the Real Estate Educators Association, The Ohio Association of Realtors, and The Columbus Board of Realtors, among others. John Wenner.

Jessica’s Law was passed in 2002 after ice broke off a moving truck, hit a second truck, and caused it to crash into Jessica Smith’s vehicle, then 20 years old, killing her. Sidewalks on public roads are maintained and cleared of snow and ice by the municipality at no additional cost to property owners, source. Jessica's Law.

Jessica's Law Jessica’s Law was passed in 2002 after ice broke off a moving truck, hit a second truck, and caused it to crash into Jessica Smith’s vehicle, then 20 years old, killing her. New Hampshire Sidewalks on public roads are maintained and cleared of snow and ice by the municipality at no additional cost to property owners.

Houston Home Seller Resources. Full Houston Home Seller Guide. Get A FREE Home Valuation Enter your email to receive a free, easy to read seller's guide on how to sell your house in the shortest time for the most money. This means a seller’s listing is competing with all these fast-paced, high-quality images.

The stats are an unwelcome paradox for buyers and sellers alike. The 30-year, fixed-rate mortgage recently broke the 7% level for the first time since April 2002, leading to greater stagnation in the housing market. We are in a new phase of the housing market cycle.

No seller must use a real estate agent to sell a home — ever. They may buy directly from a seller, whether that seller is represented by an agent or not. RealTrends + Harris Insights ‘ studies from 2002, 2005, 2006, 2011, 2014, and 2019 all show that consumers know that commissions are negotiable.

Keep them up to date in every step of the report so that they can keep the Lender (and the Buyer/Seller/Realtor/Closing Attorneys when applicable) all in the loop on the progress of the report. percent, but remained close to its highest since 2002,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content