This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

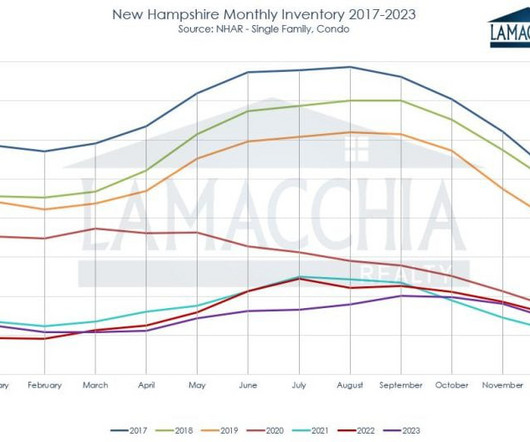

This time around, we have not seen the kind of housing credit boom that we did from 2002-2005. Since the end of June, we have seen that the home seller called it quits earlier this year than usual, and now the newlisting data is negative year to date. Newlisting data is down 5% year to date, as you can imagine.

During that period, we saw newlisting data decline. However, in 2020 newlisting data came back, and we don’t want to see the newlistings continue to decline this year — that would be a double negative for the housing market. So the fact that we are back to an average of 26 days on market makes me happier.

As you can see in our newlisting data, we are showing growth. Of course, the housing market didn’t have the credit sales boom it had from 2002-2005, but it lacked inventory. Just as they did in 2023, higher rates took the winds out of the growing sales numbers. It’s nothing spectacular but it’s growth nonetheless.

However, we haven’t had a credit sales boom like the one we saw from 2002-2005. Total Inventory had been growing from 2001-2005; total listings data in 2005 was at the higher historical range of 2.5 million listings. I don’t need to see total active listing get back to the historical range of 2-2.5 From Redfin.

Existing home sales have more legs to go lower, especially now that newlisting data is falling. A traditional primary resident seller is also a buyer, which means if they don’t list, they’re not just taking a potential home to be bought off the table — they’re taking a future sale off the books as well. million in August.”

As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. One issue that has created a waterfall dive in purchase application data and sales is that newlisting data is declining faster than usual.

This means the housing boom period of 2002-2005 had major credit tightening, which won’t happen this time around when the next recession hits. To have a balanced housing market, we need active listings to rise yearly, which they typically do; 2020 was an anomaly. The only time this happened was 2006-2011 — the housing bust years.

In 2002, when Dara Alperen Cipollone purchased her first home in East Boston, her real estate agent suggested she would be a great fit for residential sales. I need to stay on top of the market and every newlisting to assist them with navigating through what is the right information and what is to be ignored.

Sales were down in all three categories: Single family sales down by 19%: 11,625 in 2023 from 14,359 in 2022 Condo sales down by 15.7%: 3,839 in 2023 from 4,555 in 2022 Multi-family sales down by 29.5%: 853 in 2023 from 1,210 in 2022 Below is a bar graph that depicts home sales per year since 2002.

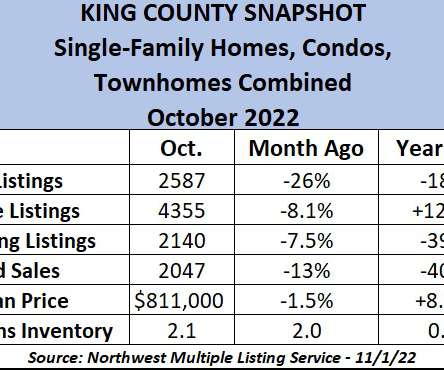

Among all home types in King, newlistings have fallen 26% in the past month and existing homes for sale at the start of November were down 8.1% Active listings for single-family homes are up 159% in King YoY, up 86% in Seattle and 425% on the Eastside. But the number of newlistings in the county is down 18% in the same period.

We are now seeing “7s” in front of some rates to new mortgage consumers – a figure not seen since April 2002 – causing applications for new loans to hit a 25-year low this month. ( Counties in and near Chicago and New York City were seen as the most vulnerable to today’s economic headwinds. OCTOBER HOUSING UPDATE.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content