This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Newly released data from the annual profile of home buyers and sellers by the National Association of Realtors (NAR) shows just how dramatically this trend has manifested since the financial crisis of 2008. Elevated mortgage rates, sky-high home prices, tight credit and stagnant wages have all contributed to homebuyers getting older.

There’s a showdown at the housing market corral between homebuyers and sellers. When I came up with the “ savagely unhealthy housing market ” label in February of this year, it was based on the premise that the housing inflation story that we have had to deal with since 2020 was a historical event.

As we close out 2022, it’s time to reflect on a historic year for the housing market, which was even crazier than the COVID-19 year of 2020. It is crazy to think we are seeing these four things happen in the housing market considering that even in March of this year we were seeing bidding wars accelerate before mortgage rates rose.

To get the housing market to be sane and normal again, we need inventory to get back in a range between 1.52 – 1.93 million ; this is still historically low, but this gives the housing market a breather from the madness that we see today. One of the critical data lines that I want to see improve this year is days on market.

Now, with five weeks of data in front of us, we can say they have stabilized the market. As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. As we can see below, none of that is happening today because the seller isn’t stressed.

This data line lags the current housing market as it’s a few months old. Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. The housing market can’t replicate the type of massive credit expansion we saw from 2002-2005, so the price-growth story has more to do with inventory collapsing to all-time lows.

Marty Green thinks of the housing market in 2022 as two very different movies. But the housing market in the second half of 2022? By September, a full-fledged housing market recession had set in. The 2002 housing market has been a tale of two halves,” said Green. A mortgage rate lockdown freezes the housing market.

I have been part of the mortgage banking industry since 1983 — 39 years to date through different housing markets. In many ways it was similar to today, with one exception: When I started, I hadn’t been spoiled by a housing market like the one in 2020 and 2021. The housing market won’t be like this forever.

A bullish housing market. The housing market didn’t crash at all, in fact, more Americans bought homes with mortgages in 2021 than in 2020. We do have some very positive stories about the housing market in 2021, but not all is perfect, of course. What a year 2021 has been. However, not only did the U.S. The excellent.

The housing market shifted in March of this year. Yes, crazy to think, but this is a survey trend data line, and the housing market was in free-fall at that time. That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. housing market. What is going on here?

We’ve all been wondering what 5% plus mortgage rates would do to the hot housing market, and now we’ve got that and a bag of chips. As a result, I’ve been rooting for mortgage rates to rise to create a balancing impact on this housing market. Have higher rates worked? What higher rates should accomplish.

Going back to the summer of 2020, the one factor that I said could change the housing market was the 10-year yield getting above 1.94%. The market is savagely unhealthy and needs balance; this is what we call balance! As you can see, sales levels were never elevated like what we saw from 2002-2005. Guess what happened in March?

Let’s keep it simple: total active listings are still below 2019 levels nationally, and the days on market are under 30 days today. However, what is different this year from 2023 is that we have more sellers that will be buyers. However, I can clear up any confusion on this topic.

housing market , we just experienced an event that most people never thought could happen. The lack of sellers is also a demand problem and what we saw after June of 2022 is that sellers called it quits earlier and faster in the year than usual, resulting in total existing home sales totaling 5,030,000 to end 2022.

This is why I have called them efficient home sellers. As we can see in the chart below, sales levels aren’t exactly booming like they were from 2002-2005. months and below, this is an excellent market for builders. months , this is just an OK market for builders. The existing home market is only sitting at 3.3

Due to this reality, I have downgraded the housing market from unhealthy housing to a savagely unhealthy housing market. For now, it’s ok, but this is one sector that people need to keep their eye out on because it’s tied to mortgage buyers more than the existing home sales market.

We finally got mortgage rates to rise, and for people like me who have been concerned about how unhealthy the housing market was last year — and it got a lot worse this year — it’s a blessing that was much needed. This sector on an apples-to-apples basis is more expensive than the existing home sales market. The only risk to that 6.2

Many of the complaints and allegations about appraisals related to not addressing the changes happening in the market as the meltdown began to occur, calling the market stable when prices were starting to decline. Between 2002-2005 in many markets, the real estate market was scorching, much like it is today.

The seller is Robert Sarver, managing partner of Suns Legacy Holdings , which owns the Phoenix Suns and Mercury. He was a backup point guard from 1998-2002 and won a national championship. But, amid a shrinking mortgage market, UWM had a market cap of about $7 billion as of Tuesday afternoon.

But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. Understanding this data line and what it is trying to tell you will be more valuable than erroneously thinking the market is crashing and we’ll see a wave of foreclosures.

During plaintiff lead attorney Michael Ketchmark’s cross examination of Warner, he presented her with some statistics showing that HomeServices affiliated agents in four Missouri markets paid buyer broker commissions of roughly 3% in at least 88% of the transactions completed between 2015 and 2022. We don’t want people unrepresented.”

Looking at the housing market in the years 2020-2024, one risk i identified early on was that home prices could accelerate more in this period than we saw in the previous expansion if inventory channels broke to all-time lows. housing market as savagely unhealthy. million homes, using the NAR data.

The savagely unhealthy housing market theme of mine is running in full force now as we have gotten no relief on home prices and now have a mega jump in mortgage rates. . Since the summer of 2020, I have talked about what could change the housing market, which was a 10-year yield above 1.94%, which means rates over 4%. million to 1.28

However, with that said, it’s still just an OK housing market for me based on how I view the new home sales market. months and below, this is an excellent market for the builders. months, this is an OK market for the builders. When supply is 4.4 They will build as long as new home sales are growing. When supply is 6.5

Then everyone went crazy on investors and iBuyers , suggesting that these people were holding up the entire housing market. I understand that grifters have to keep the grift going, but not even the Joker would say that the housing market lives off investors and not mortgage buyers. Home prices and days on market.

One tool I used for a time to level this playing field was seller-funded down payment assistance. In 2002, to protect lenders, I cofounded and organized an industry association called HAND, whose mission was to educate the mortgage industry on the proper utilization of seller funded DPA, and to curb risky practices.

While the growth rate is cooling monthly, we are still in a savagely unhhealthy housing market trying to get national inventory levels back to pre-COVID-19 levels. However, we haven’t had a credit sales boom like the one we saw from 2002-2005. Nor can we ever have a credit sales boom again with lending standards back to normal.

The truth here that nobody wants to talk about is that we didn’t have a massive sales credit boom in housing from 2020-2021 like we saw from 2002-2005. That would reverse the problem the housing market has had selling homes with mortgage rates above 7%. months, and below, this is an excellent market for builders.

The housing market is in a recession, something that the homebuilders and the National Association of Realtors now agree with me on, as this recent CNBC clip shows. Over the years, I have tried to emphasize that the housing market in the U.S. can’t have a credit sales boom like we saw from 2002-2005. This is 12.6 percent (±16.9

Tuesday, the new home sales report for March came in as a miss of estimates at 763,000, but the revisions were all positive, which shows that the housing data is still lagging behind the current market reality. The new home sales market doesn’t have a 28% cash-buyer profile as we saw in the last existing home sales report.

“The 30-year fixed-rate mortgage broke 7% for the first time since April 2002, leading to greater stagnation in the housing market,” Sam Khater, Freddie Mac’s chief economist, said in a statement. Temporary rate buydowns are not new, but tend to receive more attention when rates surge, according to industry experts.

Who said this is a sellers’ market? Perhaps it’s truly a builders’ market. GREATER BUYING POWER Buyers who are struggling to purchase a home in this frenzied housing market will receive a bit of a lifeline in 2022. However, single-family permits for King and Pierce counties combined are up 4.2%

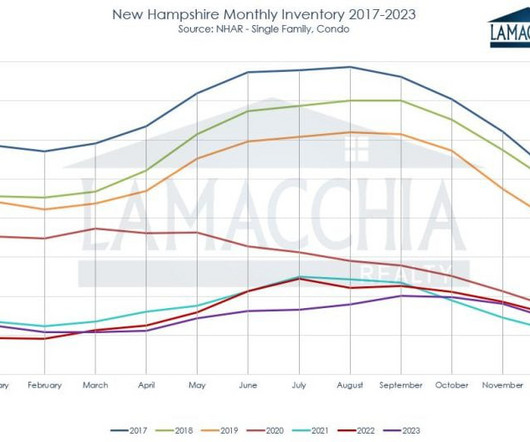

The real estate landscape witnessed significant developments in 2023, as the New Hampshire market saw a historic low in listings. Sales were also down in 2022 , which sparked concerns of a market crash , but as Anthony predicted, it didn’t happen , more thanks to reduced inventory rather than a decline in sales.

She’s held her real estate salesperson license in Ohio since 2002 and is active in many associations, including the Real Estate Educators Association, The Ohio Association of Realtors, and The Columbus Board of Realtors, among others. John Wenner.

Sell Your Home Fast For More Money: Houston Properties Online Marketing. This is because more buyers now find homes online, and the Houston Properties Team is #1 in online marketing. We have an innovative listing marketing platform that is more effective and efficient than your average Houston agent. faster and for 7.2%

The housing market in and around King County was moving along swimmingly at the start of 2022, with homes selling briskly and buyers taking advantage of interest rates in the 3s. and jump in mortgage rates of 4 percentage points has created a housing market belly flop. We are in a new phase of the housing market cycle.

No seller must use a real estate agent to sell a home — ever. They may buy directly from a seller, whether that seller is represented by an agent or not. RealTrends + Harris Insights ‘ studies from 2002, 2005, 2006, 2011, 2014, and 2019 all show that consumers know that commissions are negotiable.

NOTE: Please scroll down to read the other topics in this long blog post on retirement, classes, adjustments, real estate market, unusual homes, mortgage origination stats, etc. Some have been pushed out of the market entirely. Lack of affordability impacts the market. Topics include: Are we on the cusp of a market correction?

Keep them up to date in every step of the report so that they can keep the Lender (and the Buyer/Seller/Realtor/Closing Attorneys when applicable) all in the loop on the progress of the report. The Market Composite Index, a measure of mortgage loan application volume, decreased 0.5 Have a very responsive credo. Buyer-Borrower Remorse.

A Guide to Houston's Best Ranches & Farms On The Market. The demand is higher and there are good deals to be made both for sellers and buyers of farm and ranch-style homes. Work with the best Realtor in Houston to ensure that you’re purchasing a high-quality home at a favorable market value. Get PDF Now.

NOTE: Please scroll down to read the other topics in this long blog post on non lender appraisals, liability, markets with few sales, Bias, unusual homes, mortgage origination A California Winery With a 91-Acre Vineyard for $12,995,000 Red Soles Winery, a 91-acre vineyard. Markets hate uncertainty. Or hit the reply button.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content