This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Now, with five weeks of data in front of us, we can say they have stabilized the market. As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. The question then was: What would lower mortgage rates do to this data?

housing market , we just experienced an event that most people never thought could happen. During that period, we saw newlisting data decline. However, in 2020 newlisting data came back, and we don’t want to see the newlistings continue to decline this year — that would be a double negative for the housing market.

But I need to explain why this level has more in common with 2014 housing data than the credit stress markets of 2005-2008, and why you should care. Understanding this data line and what it is trying to tell you will be more valuable than erroneously thinking the market is crashing and we’ll see a wave of foreclosures.

Let’s keep it simple: total active listings are still below 2019 levels nationally, and the days on market are under 30 days today. As you can see in our newlisting data, we are showing growth. Of course, the housing market didn’t have the credit sales boom it had from 2002-2005, but it lacked inventory.

While the growth rate is cooling monthly, we are still in a savagely unhhealthy housing market trying to get national inventory levels back to pre-COVID-19 levels. From the index : I know it seems strange, but existing home sales are falling, and the monthly supply of new homes is at 10.9 million listings.

The savagely unhealthy housing market theme of mine is running in full force now as we have gotten no relief on home prices and now have a mega jump in mortgage rates. . Since the summer of 2020, I have talked about what could change the housing market, which was a 10-year yield above 1.94%, which means rates over 4%.

There’s a showdown at the housing market corral between homebuyers and sellers. When I came up with the “ savagely unhealthy housing market ” label in February of this year, it was based on the premise that the housing inflation story that we have had to deal with since 2020 was a historical event.

In 2002, when Dara Alperen Cipollone purchased her first home in East Boston, her real estate agent suggested she would be a great fit for residential sales. Some want me to summarize the market data and give concise guidance on market values. Q: What obstacles are Millennials facing in the Boston real estate market?

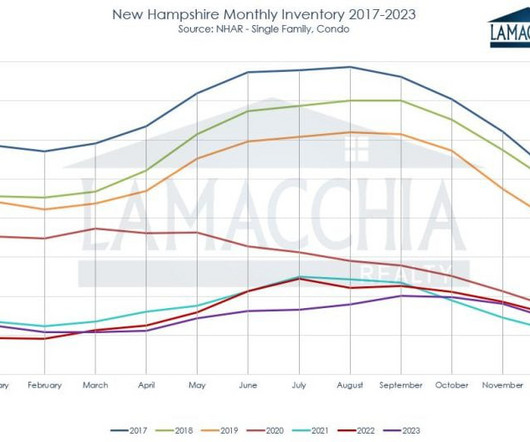

The real estate landscape witnessed significant developments in 2023, as the New Hampshire market saw a historic low in listings. Sales were also down in 2022 , which sparked concerns of a market crash , but as Anthony predicted, it didn’t happen , more thanks to reduced inventory rather than a decline in sales.

Seriously though, there must be a ceiling to rising rates that have all but extinguished a robust housing market. We are now seeing “7s” in front of some rates to new mortgage consumers – a figure not seen since April 2002 – causing applications for new loans to hit a 25-year low this month. ( OCTOBER HOUSING UPDATE.

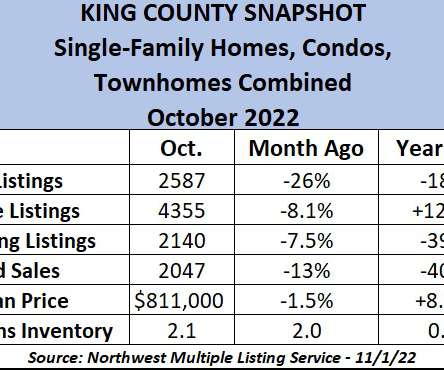

The housing market in and around King County was moving along swimmingly at the start of 2022, with homes selling briskly and buyers taking advantage of interest rates in the 3s. and jump in mortgage rates of 4 percentage points has created a housing market belly flop. We are in a new phase of the housing market cycle.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content