This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Patrice Ficklin, who has served at the Consumer Financial Protection Bureau (CFPB) since the agency’s founding in 2011, will depart for Fannie Mae to serve as the government-sponsored enterprise’s fair lending officer. CFPB Director Rohit Chopra praised Ficklin’s fair lending work in a statement published by American Banker.

As recession talk becomes more prevalent, some people are concerned that mortgage credit lending will get much tighter. One of the biggest reasons home sales crashed from their peak in 2005 was that the credit available to facilitate that boom in lending simply collapsed. The short (and long) answer is no, not a chance.

Planet Home Lending has promoted four people to vice president positions, supporting the company’s continual growth. Michaelene Whyte has been promoted from processing manager of the East to VP, national fulfillment, distributed retail, and has been with Planet Home Lending since October 2018.

Ohio -based UHM promoted Brian Smith to chief operating officer of retail lending and hired David Alonzo as its chief technology officer. Smith joined the company in 2002 and quickly became a top producer, earning a spot in the UHM President’s Club for his standout origination volume and customer service efforts.

Baltimore -based Dominion Financial Services , a nationwide private lender that specializes in financing for real estate investors , announced the hiring of Dustin Wells as the president of its newly launched wholesale lending division. Wells has more than 20 years of experience in the financial services arena.

Prior to HOMESTAR, he served as the executive vice president of retail production at AmeriSave Mortgage Corporation and area lending manager roles at Citi. The company was established in 2002 in Georgia. Bhandal’s professional career spans more than 20 years in financial services.

We aren’t anywhere close to the housing bubble dynamics we had from 2002 to 2008; that environment is simply impossible to replicate. I’m going to take their talking points and explain in detail why this isn’t the housing bubble of 2002-2005. “ Let me explain. Our evidence points to abnormal U.S.

Riccio began his career in the mortgage industry in 2002 and has held key leadership roles with several prominent organizations, including Stearns Lending and Caliber Home Loans.

First, the refinance boom’s main driver in the 2000s was unhealthy because of the marketplace’s speculative unhealthy lending standards. Home prices were growing at an unsustainable level from 2002-2005, leading to some excess risk-taking on inadequate loan debt structures.

” Christie’s International Real Estate Belgium is the real estate arm of Hillewaere Group , a firm established in 2002 by Roel Druyts that offers real estate , insurance and mortgage lending services.

today and why they’re so different than the period of 2002-2008. However, the current housing market is much different than the credit boom-and-bust cycle of 2002-2008, and it’s vital to understand why. How can we be sure not to make the same mistake that millions of people made by calling for housing to crash in 2020 and 2021?

Increasing lending and servicing capacity – regardless of mortgage rates. “Home prices have caught up to per capita income, just like what we saw in 2002. As mortgage rates come off of their historic lows, mortgage applications followed suit, dropping for the second week, according to data from the Mortgage Bankers Association.

Regions Bank is looking to make a big dent in the home improvement lending space , striking a deal to acquire EnerBank USA for $960 million in cash. The Salt Lake City-based lender says it’s worked with over 1 million homeowners since its founding in 2002 and funded $11.6 billion in home improvement projects.

“This is about the same rate of price growth that occurred during the 2002 through 2006 period when subprime lending drove exuberant housing demand. “But that is where the similarities end.

She has served as president of Lennar Mortgage, the mortgage lending subsidiary of Lennar Corp., Escobar joined Lennar Mortgage in 2002 as branch manager. Escobar is a 37-year mortgage industry veteran, She has held leadership positions with both bank-owned and independent mortgage companies overseeing all aspects of mortgage banking.

This is evident if one compares the purchase application data from the overheating market of 2002-2005 to the period between 2012-2020. First the rate of growth in no way compares to what we had during the bubble years of 2002-2005. While sales are and will stay elevated compared the COVID-19 lows, the market is not bubbly.

These sales have been tested by HUD since 2002, but HUD said that the proposed rule will improve community stability and expand the availability of affordable homes for families as the market faces a supply challenge.

The housing market of 2002-2005 had four years of sales growth facilitated by credit. However, what isn’t identical is that we have not had a massive sales boom like we saw from 2002-2005. This is significantly different than the period from 2002-2005 when credit expansion was booming. Home sales. Housing credit.

HomeStar — founded in 2002 as a local mortgage bank in Georgia — offers conventional, government and jumbo purchase loans, as well as refinances, reverse mortgages and a doctor/medical professional mortgage program. OCMBC also originated $2.1 billion in volume in nonqualified mortgage ( non-QM ) volume, placing No.

Tyrrell joined Ellie Mae in 2002, where he was promoted to executive vice president in 2013 from chief operating officer and senior vice president. Bowler will be in charge of ICE’s business segment, which is focused on automating elements of the mortgage industry and delivered a revenue of $1.1 billion in 2022, the firm said Tuesday.

Wade Susini, chief lending officer at Dominion Financial Services, told HousingWire in an email response that while inventory levels remain low across the U.S., A national lender, Dominion was founded in 2002 and has reportedly funded more than $3 billion in loans across more than 11,000 deals.

I’m not saying that home-price growth will somehow morph into a speculation bubble like it did in the 2000s — our credit lending standards will prevent that — but housing could become considerably less affordable even with low mortgage rates if this continues. The median sales price is now 11.4% higher than a year ago. Context is key!

Kumar was a manager at Standard Chartered Bank from 2002 to 2004. “We intend to change how lending is going to be done fundamentally – behavior, market dynamics, products,” Kumar said. He will serve as LendArch’s executive vice president and chief operating officer. .

Escobar’s background will ensure members’ “commitment to advancing homeownership and affordable rental housing opportunities nationwide,” said Kristy Fercho, 2022 MBA chair and executive vice president and head of home lending at Wells Fargo. Lennar Mortgage’s network includes more than 1,100 workers across 20 states.

Legacy, headquartered in Albuquerque, New Mexico, was founded in 2002 and purchased by its CEO Jack Thompson in 2006. Clients will also benefit from access to new digital and customer relationship tools that improve every step in the lending experience, including servicing, a Guild strength for decades,” Thompson said in prepared remarks.

in September 2002. Ravi Correa is Chief Financial Officer at Angel Oak Lending and responsible for all financial aspects for Angel Oak-related mortgage lending entities. That said, it’s still a far cry from 1980, when inflation spiked to a staggering 14%. consumers are about the economy and their finances.

housing market, and we should never ease lending standards to try to facilitate demand. Lending standards are already liberal enough, so we don’t need to go down that avenue. Late cycle lending is always a risk in the lending industry. Again, what happened in housing from 2002 to 2008? We had a credit boom.

Founded in 2002, Homestar is a full-service mortgage banker that offers conventional, government, jumbo, reverse loans, refinance loans and a doctor/medical professional mortgage program. Your loan should still close on time!

As you can see below, the new home sales market from 2018-2022 doesn’t look like the housing market we had from 2002-2005. Could you imagine this housing market if we eased lending standards? I would be protesting in front of Congress and speaking at congressional hearings if lending standards were reduced.

This means we don’t have enough housing inventory available because with lending standards back to normal we can’t replicate the credit demand we saw in housing from 2002-2005. I have often said that anytime days on the market are at a teenager level, nothing good will happen. Also, this is what the Federal Reserve wants.

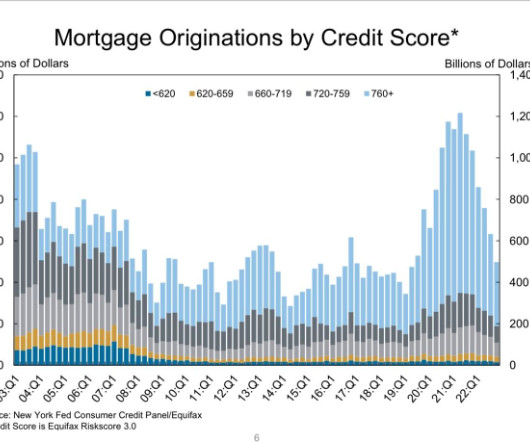

Both these laws paved the way for more responsible lending and a more responsible consumer. The FOMO demand (fear of missing out) credit boom from 2002 to 2005, as we can see below, has not happened in the last 10 years. In 2000, we saw a lot of credit stress in the system. Purchase application data is below 2008 levels today.

Between 2002-2005 in many markets, the real estate market was scorching, much like it is today. Appraisers’ jobs are not to facilitate mortgage lending. This left the appraiser wide-open to being a target of “a series of errors” that affected the credibility of the valuation results. It is not our job to kill or make deals.

Due to the loosey-goosey lending standards of the time, many of these delinquent loan holders had little to negative equity. Here is why I don’t believe that will happen: We do not have an overheated multi-year credit bubble among mortgage holders like we had from 2002-2005. The number isn’t growing; it’s slowly shrinking.

However, we haven’t had a credit sales boom like the one we saw from 2002-2005. Nor can we ever have a credit sales boom again with lending standards back to normal. As I have stressed, people need to be patient with inventory growth and not run 2002-2011 credit sales to inventory models for this marketplace.

Glenn Stearns , founder and CEO of Kind Lending , is a regular TikToker and in one video he was asked the most important lessons he learned in business and his response was “This too shall pass.”. In fact, while in won’t match 2020 or 2021, purchase mortgage dollar volume should be better than any year from 2002–2020.

The most abhorrent racist practices, such as redlining, are officially prohibited, yet bias creeps into mortgage lending in myriad ways. This makes it more important than ever to consider how the U.S. will finally welcome persons of color to share fully in the American dream of homeownership. It’s a serious challenge.

AmCap, founded in 2002, is a much smaller lender. . “I am very proud of what we built at AmCap over the years, but I fully recognize what got us here wasn’t going to get us to where we ultimately wanted to be as a business unit,” Clayton said in a statement. In terms of volume, CCM claims it originated $31.6

Some appraisers, a true minority, have been able to transition to private, non-mortgage-lending appraisal work, but that’s not as easy as some advocate. And many appraisers who only know how to do mortgage lending assignments are reluctant to market themselves outside that confined space. The GSEs started keeping track in 71.

In 2000 and 2002, Architectural Digest named him one of the top 100 architects in the United States. Mortgage lending is very, very cyclical. I agree that I would be world-famous and rich if I could predict mortgage lending cycles! This is to follow up on a meeting Appraisal Institute representatives held in Washington, D.C.

Mortgage Lending You decide. Excerpts: Accurate appraisals are essential to the integrity of mortgage lending. percent, but remained close to its highest since 2002,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. Do not use lender forms. Type of report. Lender decides You decide.

This strategy often backfires because parties involved in the lending process cannot find the specific information they are looking for in the report. I’m reading lots of predictions from people in high places in the real estate and lending worlds saying that the correction is underway, and it’s all about affordability.

In fact, mortgage rates over the last decade have been lower almost every month compared to those during the housing bubble years and we have not seen the massive sales we saw from 2002-2005. Nonetheless, during those years, existing home sales, new home sales, home prices, housing starts, permits, and completions were booming.

Faulty loans on mobile homes led to the downfall of the nation’s largest manufactured home lender in 2002, ensnaring Fannie Mae on its way down, an episode both GSEs remember well. But when home prices depreciated, it flamed out, and its parent Conseco filed for bankruptcy protection in 2002.

While investors of mortgaged securities help dictate their interest rates, the Federal Reserve is behind the scenes influencing the overall lending environment. We are now seeing “7s” in front of some rates to new mortgage consumers – a figure not seen since April 2002 – causing applications for new loans to hit a 25-year low this month. (

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content