This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Riccio has been instrumental in overseeing critical functions such as trading, hedging, pricing, and investor relations. Riccio began his career in the mortgage industry in 2002 and has held key leadership roles with several prominent organizations, including Stearns Lending and Caliber Home Loans.

Baltimore -based Dominion Financial Services , a nationwide private lender that specializes in financing for real estate investors , announced the hiring of Dustin Wells as the president of its newly launched wholesale lending division. Wells has more than 20 years of experience in the financial services arena.

Dominion Financial Services , a Baltimore -based private lender with products tailored to real estate investors , has launched a third-party origination program for mortgage brokers, according to an announcement on Thursday. investors are “finding creative ways“ to acquire and redevelop real estate.

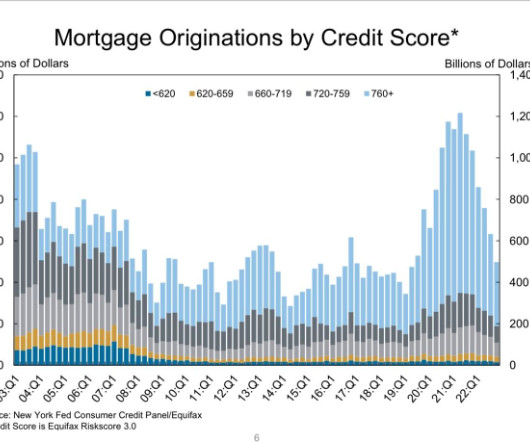

today and why they’re so different than the period of 2002-2008. However, the current housing market is much different than the credit boom-and-bust cycle of 2002-2008, and it’s vital to understand why. How can we be sure not to make the same mistake that millions of people made by calling for housing to crash in 2020 and 2021?

This means we don’t have enough housing inventory available because with lending standards back to normal we can’t replicate the credit demand we saw in housing from 2002-2005. I have often said that anytime days on the market are at a teenager level, nothing good will happen. Also, this is what the Federal Reserve wants.

Compared to the existing home sales marketplace, it doesn’t have a high cash buyer or investor buyer profile. As you can see below, the new home sales market from 2018-2022 doesn’t look like the housing market we had from 2002-2005. Could you imagine this housing market if we eased lending standards?

housing market, and we should never ease lending standards to try to facilitate demand. Lending standards are already liberal enough, so we don’t need to go down that avenue. Late cycle lending is always a risk in the lending industry. Again, what happened in housing from 2002 to 2008? We had a credit boom.

Some of their biggest hits (or should I say misses) in the last 8 years have been the never-realized silver tsunami crash, the ever popular investor supply crash, the Airbnb supply crash, and this year, COVID-19 was for sure going to send prices crashing 30%-50%. The number isn’t growing; it’s slowly shrinking.

However, we haven’t had a credit sales boom like the one we saw from 2002-2005. Nor can we ever have a credit sales boom again with lending standards back to normal. I am not talking about investors; I am talking about primary resident homeowners. Case in point, purchase application data is already below 2008 levels today.

Fannie Mae will end up creating more instability for the trillions in the bond market – investors will have to process millions of valuations with the physical attributes of the home collected by unlicensed, uninsured, and unprepared individuals getting paid $10-$25 per inspection. Mortgage lending is very, very cyclical.

While investors of mortgaged securities help dictate their interest rates, the Federal Reserve is behind the scenes influencing the overall lending environment. Seriously though, there must be a ceiling to rising rates that have all but extinguished a robust housing market. may be the better million-dollar question.).

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content