This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Riccio has been instrumental in overseeing critical functions such as trading, hedging, pricing, and investor relations. Riccio began his career in the mortgage industry in 2002 and has held key leadership roles with several prominent organizations, including Stearns Lending and Caliber Home Loans.

Prior to this new position, she served as the chief investor and industry relations officer of Home Point Financial Corporation. Meanwhile, Greenberg was promoted to senior vice president of finance where he will oversee investor relations, financial planning, analysis, data analytics and treasury.

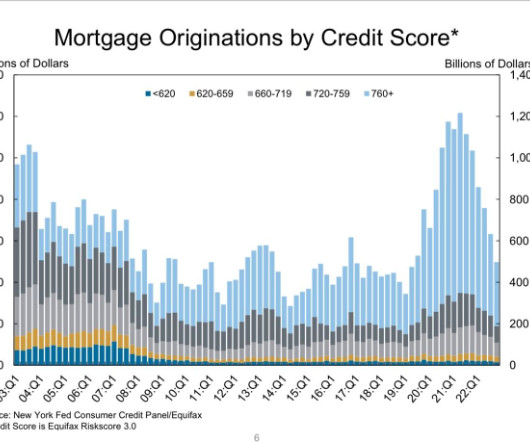

Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. The housing market can’t replicate the type of massive credit expansion we saw from 2002-2005, so the price-growth story has more to do with inventory collapsing to all-time lows. Also, certain investors felt no fear post-2020.

Dominion Financial Services , a Baltimore -based private lender with products tailored to real estate investors , has launched a third-party origination program for mortgage brokers, according to an announcement on Thursday. investors are “finding creative ways“ to acquire and redevelop real estate.

today and why they’re so different than the period of 2002-2008. However, the current housing market is much different than the credit boom-and-bust cycle of 2002-2008, and it’s vital to understand why. How can we be sure not to make the same mistake that millions of people made by calling for housing to crash in 2020 and 2021?

On March 22, Moulder, who worked with Keller Williams from 2002 to 2011, filed a complaint aiming for class-action status in the U.S. Hill, a former KW agent from 2002 to 2013, filed a similar complaint in the U.S. these funds continue to enrich only affiliated real estate agents, investors, brokers, and staff.”

Baltimore -based Dominion Financial Services , a nationwide private lender that specializes in financing for real estate investors , announced the hiring of Dustin Wells as the president of its newly launched wholesale lending division. Wells has more than 20 years of experience in the financial services arena.

That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. The Baby Boomers are not selling their homes en masse, and we have more investors providing shelter for renters than before. If you connect the lines, you can see where we are on a historical basis. What is going on here?

The company’s Loansifter PPE, a component of Black Knight’s suite of integrated solutions designed for brokers, supports execution searches across more than 120 wholesale investors. “If personalized pricing quotes aren’t available on your website, consumers will find them somewhere else. and Thomas H.

The functionality expansion will assist investors and lenders in promoting affordable housing in underserved markets, the firm said. Loansifter PPE, a component of Black Knight’s suite of integrated solutions designed for brokers, allows searches across more than 120 wholesale investors.

As you can see, sales levels were never elevated like what we saw from 2002-2005. This housing cycle is and will always be based on real demand, versus the credit boom we saw from 2002 to 2005. However, this is much different than what we saw from 2002-to 2005. Slow and steady wins the race.

However, a seller is also a natural homebuyer, unless they’re an investor. However, distressed sales are down a lot today compared to back then, and sales to investors are 19% today compared to 16% back then. From NAR in 2016: First-time buyers were 32% in November; Investors were 12%; All-cash sales were 21%; Distressed sales were 6%.

Fannie Mae has unveiled its second credit-risk transfer (CRT) deal of 2002, a $1.2 The recent offering , CAS Series 2022-R02, involves transferring loan-portfolio risk to private investors via a $1.2 billion note offering through its Connecticut Avenue Securities real estate mortgage investment conduit, or REMIC. .

real estate investors and affordable homes. We never saw the credit sales boom as we did from 2002-2005, so the builders themselves are in a better position to manage their future. This is also similar to the purchase application data, since we never had a credit boom in housing as we saw from 2002-2005.

Black Knight announced in July 2020 it would buy 60% of Optimal Blue, a company founded in 2002 that provides an online marketplace that connects originators, investors and providers in the mortgage industry. Investors’ expectations are not so positive. In the first quarter, Black Knight also had a gain of $305.4

Then everyone went crazy on investors and iBuyers , suggesting that these people were holding up the entire housing market. I understand that grifters have to keep the grift going, but not even the Joker would say that the housing market lives off investors and not mortgage buyers.

The 2022 forecast also considers the purchase of the outstanding interests of Optimal Blue from co-investors Cannae Holdings and investment entities affiliated with Thomas H. Kirk Larsen, the company CFO, said organic growth will likely fall between 7% and 8%. Lee Partners for $1.156 billion.

This means we don’t have enough housing inventory available because with lending standards back to normal we can’t replicate the credit demand we saw in housing from 2002-2005. I have often said that anytime days on the market are at a teenager level, nothing good will happen. Also, this is what the Federal Reserve wants.

We don’t have a massive credit boom as purchase application data is at historical lows; we haven’t had the same run-up in credit as we saw from 2002-2005. This is why I always draw the black line on the chart below — to show people that we haven’t had a credit boom for many years.

Compared to the existing home sales marketplace, it doesn’t have a high cash buyer or investor buyer profile. As you can see below, the new home sales market from 2018-2022 doesn’t look like the housing market we had from 2002-2005. percent (±11.9 percent)* below the revised January rate of 788,000 and is 6.2 percent (±13.7

Some of their biggest hits (or should I say misses) in the last 8 years have been the never-realized silver tsunami crash, the ever popular investor supply crash, the Airbnb supply crash, and this year, COVID-19 was for sure going to send prices crashing 30%-50%.

However, we haven’t had a credit sales boom like the one we saw from 2002-2005. I am not talking about investors; I am talking about primary resident homeowners. As I have stressed, people need to be patient with inventory growth and not run 2002-2011 credit sales to inventory models for this marketplace. million listings.

In 2002, Gaines co-founded Claims Recovery Financial Services (CRFS), a prominent investor and government claim services provider, which she initially established from her kitchen table. Under her leadership, CRFS grew to become an industry leader, employing over 600 individuals.

Because we had a housing credit bubble from 2002 to 2005, the credit demand push on exotic loan debt structures was a setup for future forced credit selling. The last time we had total inventory growth was back in 2014 when we tried to get back to 2.5

NAR Research: “First-time buyers were responsible for 29% of sales in August; Individual investors purchased 16% of homes; All-cash sales accounted for 24% of transactions; Distressed sales represented approximately 1% of sales; Properties typically remained on the market for 16 days.”. However, it’s not the market of 2002-2011.

What I believe occurred is that some housing investors took the decline in builders confidence and the increase in monthly supply to push that something bad was going to occur quickly. percent)* below the December 2020 estimate of 943,000 Slow and steady wins the race and the market that we had from 2002-2005 doesn’t exist today.

Housing demand has been stable for the past few years; we have never had a credit boom in demand since 2002-2005. From NAR : Total existing-home sales dipped 2.7% from February to a seasonally adjusted annual rate of 5.77 million in March. So, we never had a credit bust as we saw from 2005 to 2008.

The 30-year fixed-rate mortgage broke 7% for the first time since April 2002, leading to greater stagnation in the housing market,” Sam Khater, Freddie Mac’s chief economist, said in a statement. A year ago at this time, rates averaged 3.14%. The 10-year note went to 4.04% from 4.14% in the same period.

Again, what happened in housing from 2002 to 2008? Our market is much different than that 2002-2008 period. I believe some people who say that iBuyers and Wall Street investors are holding up the housing market don’t understand they’re making a super bullish thesis that housing can’t ever fade. We had a credit boom.

According to KBW analysts, affordability is 30% below the long run with payment-to-income of 27% compared to 20% between 2002 and 2004. ” “The outlook, at least from investors, is better, and I would also highlight that if you just look at gain-on-sale margins, they are really stabilized. million homes.

Since 2002, Butler has served as the founding chairman of the Technology Leadership Council, Boston chapter. This is a time when business should be ticking back up, giving customers and investors confidence while getting us time to come out of ’24 in a really good position.

Also, the market we have today doesn’t look like the credit boom we saw from 2002-2005. When you add move-up, move-down, cash and investor demand together, demand will be stable and hard to break under the post-1996 trend of 4 million plus total sales every year in the years 2020-2024. The X factor.

Properties are ideal for young professionals, investors seeking properties to rent to college students, and established folks looking to settle in their home for the long haul. The majority of this neighborhood was built in 2002 and offers easy access to greenways adjacent to the Neuse River. Falls River is an impeccable area to see.

Historically low interest rates brought buyers and investors out of the woodwork for any homes for sale. The 30-year, fixed-rate mortgage recently broke the 7% level for the first time since April 2002, leading to greater stagnation in the housing market. While a slowdown is expected in autumn months, this rate of decline is not.

He joined Prudential in 1995 as chief financial officer and rose the ranks to being named to the office of the chairman in 2002 and vice chairman in 2007. He oversaw finance, risk management, the chief investment office, corporate actuarial, investor relations, global business technology solutions, marketing and communications.

In 2002, he joined the firm’s executive team, serving as president, before a nine-year stint as CEO from 2005 to 2014. ” Since 1991, Willis has served in various leadership roles within the company, including regional director, operating principal, team leader, and as a market center and region investor. That’s Mark Willis.”

Fannie Mae will end up creating more instability for the trillions in the bond market – investors will have to process millions of valuations with the physical attributes of the home collected by unlicensed, uninsured, and unprepared individuals getting paid $10-$25 per inspection. . His homes are as unique as he was,” says Heinrich. “He

I have never been a housing sales boom person because I don’t believe we can have a credit boom in America like we saw from 2002 to 2005. More Americans bought homes in 2020 and 2021 than any single year from 2008 to 2019, which looks normal. However, total home sales — new and existing — during 2020-2024 should be 6.2

While investors of mortgaged securities help dictate their interest rates, the Federal Reserve is behind the scenes influencing the overall lending environment. We are now seeing “7s” in front of some rates to new mortgage consumers – a figure not seen since April 2002 – causing applications for new loans to hit a 25-year low this month. (

Just last month, Canada’s prime minister proposed a two-year ban on some foreign investors buying Canadian real estate to try to tame price growth. I’ve tried to stress that we need to worry about home prices getting overheated in 2020-2024, but not because of some massive credit boom like we saw from 2002 to 2005.

She was EVP of Strategy and Planning at residential mortgage banker MortgageIT from 2004-2007, and President of MortgageITs Home Closer LLC division from 2002-2004. From 1999-2002, Prokop was EVP of Corporate Development at Digital Convergence Corporation, and she was an Investment Officer at AIG-Brunswick Capital Management from 1996-1999.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content