This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

It’s an excellent time to discuss housing inventory. That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. How can housing inventory be so low today when it skyrocketed back in 2009? I don’t believe housing inventory below 1.52 What is going on here? housing market.

On Friday NAR reported that total housing inventory levels broke under 1 million in December, dropping to 970,00 units for a population of 330 million people. million in January down to about 4 million in December, We now have total inventory levels near all-time lows again. Unsold inventory sits at a 2.9-month months in Nov.

Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. The housing market can’t replicate the type of massive credit expansion we saw from 2002-2005, so the price-growth story has more to do with inventory collapsing to all-time lows. Also, certain investors felt no fear post-2020.

Inventory has broken to all-time lows, but it doesn’t look like the year-over-year data will be positive at all this year unless demand softens up. NAR Research : Unsold inventory sits at a 1.7-month NAR Research : Unsold inventory sits at a 1.7-month However, negative year-over-year inventory is not what we want to see.

Dominion Financial Services , a Baltimore -based private lender with products tailored to real estate investors , has launched a third-party origination program for mortgage brokers, according to an announcement on Thursday. investors are “finding creative ways“ to acquire and redevelop real estate.

As you can see, sales levels were never elevated like what we saw from 2002-2005. This housing cycle is and will always be based on real demand, versus the credit boom we saw from 2002 to 2005. However, this isn’t going to help much because the existing home sales market has a different inventory channel.

Second, because of the downtrend in inventory since 2014 and the demand pick-up we will see in the years 2020-2024, we had a risk of home prices accelerating too much. Compared to the existing home sales marketplace, it doesn’t have a high cash buyer or investor buyer profile. First, total home sales should be 6.2 percent (±11.9

Some of their biggest hits (or should I say misses) in the last 8 years have been the never-realized silver tsunami crash, the ever popular investor supply crash, the Airbnb supply crash, and this year, COVID-19 was for sure going to send prices crashing 30%-50%. That year, existing homes sales broke over 4.5 This sounds like a broadway play.

This is something that I said would change the tone of housing, and we are seeing that result this year as sales decline and inventory picks up. We were told that population growth is slowing, we were told that Americans would panic sell and that massive inventory would hit the marketplace once rates got to 4%. Wait, what? I use the 1.52-1.93

Then everyone went crazy on investors and iBuyers , suggesting that these people were holding up the entire housing market. I understand that grifters have to keep the grift going, but not even the Joker would say that the housing market lives off investors and not mortgage buyers. Until then, it’s still the hunger games for housing.

We don’t have a massive credit boom as purchase application data is at historical lows; we haven’t had the same run-up in credit as we saw from 2002-2005. If we had a massive credit boom-to-bust, inventory would have skyrocketed in 2022. NAR Total Inventory Data going back to 1982. million, up from 1.03 million last year.

Total Inventory data fell in this report from 1.31 It doesn’t even look like we will breach the lower level of my inventory wish list of 1.52 I am a big fan of inventory to 2019 levels. Even though 2019 inventory levels were historically low, they were at four-decade lows before 2020; they’re a more effective pricing market.

While the growth rate is cooling monthly, we are still in a savagely unhhealthy housing market trying to get national inventory levels back to pre-COVID-19 levels. Housing inventory issue with no booming demand. However, we haven’t had a credit sales boom like the one we saw from 2002-2005. million listings.

However, the real story of 2022 is that the savagely unhealthy housing market continues as inventory is still lower than last year, sending home prices growth into double digits again. Housing demand has been stable for the past few years; we have never had a credit boom in demand since 2002-2005. Unsold inventory sits at a 2.0-month

Home prices are skyrocketing, housing inventory is at all-time lows and homebuyers have to contend with multiple bids. Inventory velocity. April 10, 2020: We needed a lot of inventory, fast. The velocity of inventory rising in the next three months is limited. April 2022: Inventory has not recovered. Can this last?

The macro challenge: Still not much inventory Analysts unanimously agree that inventory will continue to be a significant issue entering 2024. ” George agrees that inventory will remain a problem. Given these distinct macro forecasts for 2024, what should originators keep in their playbook for next year? million homes.

Also, the market we have today doesn’t look like the credit boom we saw from 2002-2005. Housing inventory has been falling since 2014 and mortgage purchase applications have been rising since then. When demand is stable, it’s extremely rare for inventory to skyrocket and American homeowners have never looked better on paper.

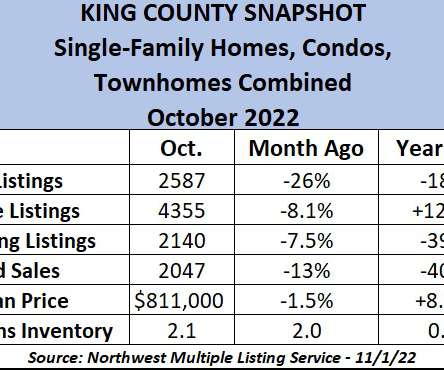

Historically low interest rates brought buyers and investors out of the woodwork for any homes for sale. Sure, the increases in inventory are impressive – up 123% for all homes in the county from 2021 to today and up a whopping 359% on the Eastside – but that should not surprise anyone. months’ inventory while Seattle is at 2.5

I have never been a housing sales boom person because I don’t believe we can have a credit boom in America like we saw from 2002 to 2005. As we are getting closer and closer to the spring selling season, we are at fresh new all-time lows in inventory and mortgage rates, and the unemployment rate is below 4% still.

Fannie Mae will end up creating more instability for the trillions in the bond market – investors will have to process millions of valuations with the physical attributes of the home collected by unlicensed, uninsured, and unprepared individuals getting paid $10-$25 per inspection. . His homes are as unique as he was,” says Heinrich. “He

While investors of mortgaged securities help dictate their interest rates, the Federal Reserve is behind the scenes influencing the overall lending environment. We are now seeing “7s” in front of some rates to new mortgage consumers – a figure not seen since April 2002 – causing applications for new loans to hit a 25-year low this month. (

Just last month, Canada’s prime minister proposed a two-year ban on some foreign investors buying Canadian real estate to try to tame price growth. I’ve tried to stress that we need to worry about home prices getting overheated in 2020-2024, but not because of some massive credit boom like we saw from 2002 to 2005.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content