This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Newly released data from the annual profile of home buyers and sellers by the National Association of Realtors (NAR) shows just how dramatically this trend has manifested since the financial crisis of 2008. Elevated mortgage rates, sky-high home prices, tight credit and stagnant wages have all contributed to homebuyers getting older.

As we close out 2022, it’s time to reflect on a historic year for the housingmarket, which was even crazier than the COVID-19 year of 2020. A few months ago, I was asked to go on CNBC and talk about why I call this a housing recession and why this year reminds me a lot of 2018, but much worse on the four items above.

To get the housingmarket to be sane and normal again, we need inventory to get back in a range between 1.52 – 1.93 million ; this is still historically low, but this gives the housingmarket a breather from the madness that we see today. However, a seller is also a natural homebuyer, unless they’re an investor.

As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. What I mean by a credit bust is that after the housing bubble burst in 2005 into 2006, we saw a massive increase in supply. Total inventory levels. NAR: Total Inventory levels 1.22

There’s a showdown at the housingmarket corral between homebuyers and sellers. When I came up with the “ savagely unhealthy housingmarket ” label in February of this year, it was based on the premise that the housing inflation story that we have had to deal with since 2020 was a historical event.

Marty Green thinks of the housingmarket in 2022 as two very different movies. ” Houses were selling at a fever pitch in a matter of days, with multiple offers, waived contingencies and buyers paying $100,000(!) But the housingmarket in the second half of 2022? over asking price. High octane stuff.

I have been part of the mortgage banking industry since 1983 — 39 years to date through different housingmarkets. In many ways it was similar to today, with one exception: When I started, I hadn’t been spoiled by a housingmarket like the one in 2020 and 2021. economy, especially the mortgage and housing sector.

This data line lags the current housingmarket as it’s a few months old. Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. million, the housingmarket can be sane again, even though those levels were the historically low levels of inventory going back to 1982.

A bullish housingmarket. economic recovery was a false story and that we were about to embark on a second housing bubble crash due to forbearance. The housingmarket didn’t crash at all, in fact, more Americans bought homes with mortgages in 2021 than in 2020. What a year 2021 has been. The excellent.

We’ve all been wondering what 5% plus mortgage rates would do to the hot housingmarket, and now we’ve got that and a bag of chips. As a result, I’ve been rooting for mortgage rates to rise to create a balancing impact on this housingmarket. Have higher rates worked? Some data to consider: 1.

Due to this reality, I have downgraded the housingmarket from unhealthy housing to a savagely unhealthy housingmarket. HousingWire: Switching gears really quickly, have you received any feedback on your savagely unhealthy housingmarket piece ? The days on the market to sell a home is too low.

It’s an excellent time to discuss housing inventory. The housingmarket shifted in March of this year. As the 10-year yield broke above 1.94% and mortgage rates rose, we saw the impact on housing data. Yes, crazy to think, but this is a survey trend data line, and the housingmarket was in free-fall at that time.

A lot of the housing data was lagging the rate move, so it wasn’t apparent that higher rates impacted the data yet. Going back to the summer of 2020, the one factor that I said could change the housingmarket was the 10-year yield getting above 1.94%. However, the housingmarket changed once the 10-year yield broke over 1.94%.

housingmarket , we just experienced an event that most people never thought could happen. If you believe people sell to become homeless, then you’re in the group of people that have simply not read housing data for decades. The days on market were too low. And existing home sales crashed in 2022 from a peak of around 6.5

We finally got mortgage rates to rise, and for people like me who have been concerned about how unhealthy the housingmarket was last year — and it got a lot worse this year — it’s a blessing that was much needed. As you can see below, the new home sales market from 2018-2022 doesn’t look like the housingmarket we had from 2002-2005.

However, what is different this year from 2023 is that we have more sellers that will be buyers. The existing home sales print is catching up to our data, and this, to me, is the best story for housing in 2024 because when the housingmarket was savagely unhealthy in 2022, the NAR total active listings data was below 1 million.

This is why I have called them efficient home sellers. As we can see in the chart below, sales levels aren’t exactly booming like they were from 2002-2005. From Census: For sale inventory and months’ supply : The seasonally‐adjusted estimate of new houses for sale at the end of August was 436,000.

Looking at the housingmarket in the years 2020-2024, one risk i identified early on was that home prices could accelerate more in this period than we saw in the previous expansion if inventory channels broke to all-time lows. housingmarket as savagely unhealthy. million homes, using the NAR data.

However, the housingmarket did run into one problem in 2020. Inventory levels broke to all-time lows and thus created massive housing inflation quickly, which broke my model. I knew housing would be OK as long as home prices only grew at 23% over five years — 4.6% This means less demand for housing.

The savagely unhealthy housingmarket theme of mine is running in full force now as we have gotten no relief on home prices and now have a mega jump in mortgage rates. . Since the summer of 2020, I have talked about what could change the housingmarket, which was a 10-year yield above 1.94%, which means rates over 4%.

Knowing that the housing crash addicts on YouTube , Twitter , Facebook , and Clubhouse would incorrectly push the negative year-over-year data spin, I wanted to get ahead of that narrative. Then everyone went crazy on investors and iBuyers , suggesting that these people were holding up the entire housingmarket.

While the growth rate is cooling monthly, we are still in a savagely unhhealthy housingmarket trying to get national inventory levels back to pre-COVID-19 levels. However, we haven’t had a credit sales boom like the one we saw from 2002-2005. Case in point, purchase application data is already below 2008 levels today.

The housingmarket is in a recession, something that the homebuilders and the National Association of Realtors now agree with me on, as this recent CNBC clip shows. Over the years, I have tried to emphasize that the housingmarket in the U.S. can’t have a credit sales boom like we saw from 2002-2005. This is 12.6

Between 2002-2005 in many markets, the real estate market was scorching, much like it is today. As appraisers, we faced tremendous pressure from buyers, sellers, real estate agents, and loan officers during the previous run-up. We are seeing that as a profession again. Is this any different than last time?

The truth here that nobody wants to talk about is that we didn’t have a massive sales credit boom in housing from 2020-2021 like we saw from 2002-2005. That would reverse the problem the housingmarket has had selling homes with mortgage rates above 7%.

“The 30-year fixed-rate mortgage broke 7% for the first time since April 2002, leading to greater stagnation in the housingmarket,” Sam Khater, Freddie Mac’s chief economist, said in a statement. Temporary rate buydowns are not new, but tend to receive more attention when rates surge, according to industry experts.

The one thing housing has going for it now is that we don’t have the speculative booming demand as we saw from 2002 to 2005. From Census: The median sales price of new houses sold in March 2022 was $436,700. The builders have pricing power and they — along with home sellers — have pushed it very hard since 2020.

In reality, as we talked about many times on HousingWire, housing data was going to moderate, find a base and work from that COVID-19 surge in the data. However, with that said, it’s still just an OK housingmarket for me based on how I view the new home sales market. This is 11.9 percent (±20.3 percent (±16.6

Who said this is a sellers’ market? Perhaps it’s truly a builders’ market. GREATER BUYING POWER Buyers who are struggling to purchase a home in this frenzied housingmarket will receive a bit of a lifeline in 2022. DECEMBER HOUSING UPDATE. What may 2022 offer for our housingmarket?

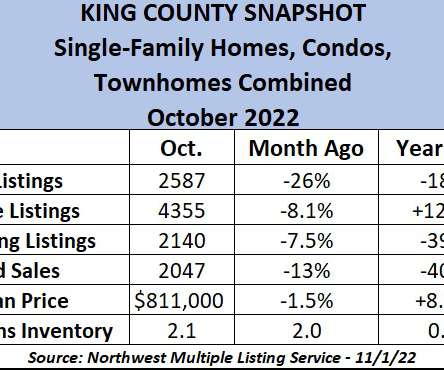

The housingmarket in and around King County was moving along swimmingly at the start of 2022, with homes selling briskly and buyers taking advantage of interest rates in the 3s. and jump in mortgage rates of 4 percentage points has created a housingmarket belly flop. We are in a new phase of the housingmarket cycle.

No seller must use a real estate agent to sell a home — ever. They may buy directly from a seller, whether that seller is represented by an agent or not. RealTrends + Harris Insights ‘ studies from 2002, 2005, 2006, 2011, 2014, and 2019 all show that consumers know that commissions are negotiable.

Keep them up to date in every step of the report so that they can keep the Lender (and the Buyer/Seller/Realtor/Closing Attorneys when applicable) all in the loop on the progress of the report. percent, but remained close to its highest since 2002,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist.

Dear Sellers, the housingmarket misses you It’s tough to value properties today! How does your market compare with Ryan’s? percent, the highest rate since 2002. To read more, click here My comments: Good comments. I had never looked at appraisal downturns this way.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content