This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. What I mean by a credit bust is that after the housing bubble burst in 2005 into 2006, we saw a massive increase in supply. Mortgage rates went from a low of 2.5%

housingmarket , we just experienced an event that most people never thought could happen. The Federal Reserve wanted a housing reset , and it got a housing recession, with activity falling the fastest since the brief pause during COVID-19. During that period, we saw newlisting data decline.

However, the housingmarket did run into one problem in 2020. Inventory levels broke to all-time lows and thus created massive housing inflation quickly, which broke my model. I knew housing would be OK as long as home prices only grew at 23% over five years — 4.6% This means less demand for housing.

As you can see in our newlisting data, we are showing growth. The existing home sales print is catching up to our data, and this, to me, is the best story for housing in 2024 because when the housingmarket was savagely unhealthy in 2022, the NAR total active listings data was below 1 million.

There’s a showdown at the housingmarket corral between homebuyers and sellers. When I came up with the “ savagely unhealthy housingmarket ” label in February of this year, it was based on the premise that the housing inflation story that we have had to deal with since 2020 was a historical event.

The savagely unhealthy housingmarket theme of mine is running in full force now as we have gotten no relief on home prices and now have a mega jump in mortgage rates. . Since the summer of 2020, I have talked about what could change the housingmarket, which was a 10-year yield above 1.94%, which means rates over 4%.

While the growth rate is cooling monthly, we are still in a savagely unhhealthy housingmarket trying to get national inventory levels back to pre-COVID-19 levels. From the index : I know it seems strange, but existing home sales are falling, and the monthly supply of new homes is at 10.9 million listings. From Redfin.

Seriously though, there must be a ceiling to rising rates that have all but extinguished a robust housingmarket. We are now seeing “7s” in front of some rates to new mortgage consumers – a figure not seen since April 2002 – causing applications for new loans to hit a 25-year low this month. (

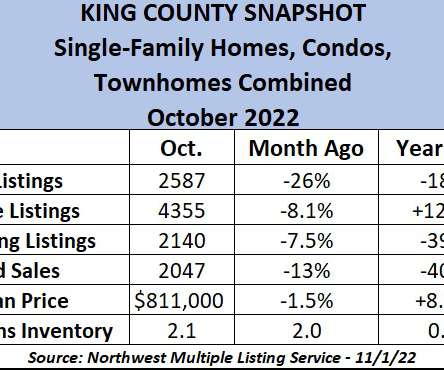

The housingmarket in and around King County was moving along swimmingly at the start of 2022, with homes selling briskly and buyers taking advantage of interest rates in the 3s. and jump in mortgage rates of 4 percentage points has created a housingmarket belly flop. We are in a new phase of the housingmarket cycle.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content