This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

As we close out 2022, it’s time to reflect on a historic year for the housingmarket, which was even crazier than the COVID-19 year of 2020. A few months ago, I was asked to go on CNBC and talk about why I call this a housing recession and why this year reminds me a lot of 2018, but much worse on the four items above.

I have been part of the mortgage banking industry since 1983 — 39 years to date through different housingmarkets. In many ways it was similar to today, with one exception: When I started, I hadn’t been spoiled by a housingmarket like the one in 2020 and 2021. economy, especially the mortgage and housing sector.

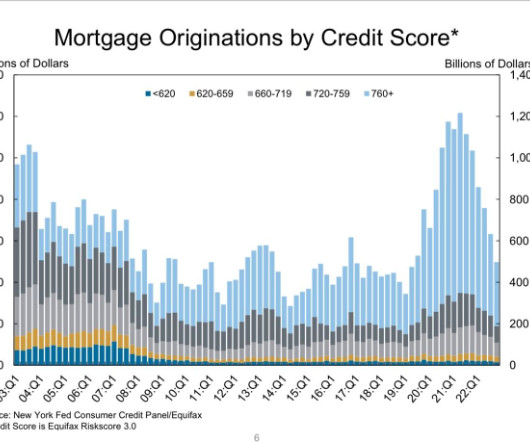

As recession talk becomes more prevalent, some people are concerned that mortgage credit lending will get much tighter. One of the biggest reasons home sales crashed from their peak in 2005 was that the credit available to facilitate that boom in lending simply collapsed. The short (and long) answer is no, not a chance.

housingmarket and compare those to where we are today — in the middle of one of the most epic years in our country’s history, due to COVID-19. No doubt about it, the COVID crisis has taken some juice out of the 2020 housingmarket. The February housing data, pre-COVID, was juicy indeed. higher than a year ago.

One of the reasons that I moved into the “team higher mortgage rate” camp is that what I saw in January, February, and March of this year was so unhealthy that I labeled the housingmarket savagely unhealthy. million — once that happens, I can take the unhealthy label off the housingmarket.

That’s not to say that the data points the Fed used are incorrect — in fact, we are in a savagely unhealthy housingmarket , but it’s not a bubble. First, because there is no speculative debt demand going on today, there can’t be a housing bubble. housingmarket behavior for the first time since the boom of the early 2000s.

With the banking crisis spurring more talk of a recession, the question now is: What would housing credit look like in a recession? housingmarket would crash during the pandemic. One of the main reasons for that fear was that housing credit was about to get tight, meaning fewer people could buy homes with mortgages.

I hear a lot of chatter about a boom in cash-out refinances, and the presumption seems to be that this is destined to wreak havoc on the housingmarket and the economy at some point. First, the refinance boom’s main driver in the 2000s was unhealthy because of the marketplace’s speculative unhealthy lending standards.

Let’s just say this is the final nail in the coffin for the housing bear troll camps that were so sure that this time, housing would finally crash. COVID didn’t get the housingmarket, but it did pull a fast one on those pesky bears. We saw hints of a flourishing housingmarket prior to the COVID crisis.

“This is about the same rate of price growth that occurred during the 2002 through 2006 period when subprime lending drove exuberant housing demand. “But that is where the similarities end.

” Christie’s International Real Estate Belgium is the real estate arm of Hillewaere Group , a firm established in 2002 by Roel Druyts that offers real estate , insurance and mortgage lending services.

housingmarket , we just experienced an event that most people never thought could happen. However, in 2020 new listing data came back, and we don’t want to see the new listings continue to decline this year — that would be a double negative for the housingmarket. The days on market were too low.

We finally got mortgage rates to rise, and for people like me who have been concerned about how unhealthy the housingmarket was last year — and it got a lot worse this year — it’s a blessing that was much needed. As you can see below, the new home sales market from 2018-2022 doesn’t look like the housingmarket we had from 2002-2005.

Tyrrell joined Ellie Mae in 2002, where he was promoted to executive vice president in 2013 from chief operating officer and senior vice president. Bowler will be in charge of ICE’s business segment, which is focused on automating elements of the mortgage industry and delivered a revenue of $1.1 billion in 2022, the firm said Tuesday.

Despite what they promised, we sit here today with the United States housingmarket outperforming all other economic sectors in the world during the pandemic. In order for the housingmarket to crash due to too many loans going into default when forbearance programs end, the number of loans in these programs needs to grow.

While the growth rate is cooling monthly, we are still in a savagely unhhealthy housingmarket trying to get national inventory levels back to pre-COVID-19 levels. However, we haven’t had a credit sales boom like the one we saw from 2002-2005. Case in point, purchase application data is already below 2008 levels today.

in September 2002. Mortgage executives should focus on these indicators — as well as keep a close eye on their originating markets — to ensure they understand key market factors and can adjust business strategies accordingly. That said, it’s still a far cry from 1980, when inflation spiked to a staggering 14%.

Both these laws paved the way for more responsible lending and a more responsible consumer. During the build-up to when the housing bubble burst, housing was getting noticeably weaker on many fronts. Currently, the housingmarket is in a recession: sales, production, jobs and incomes are all falling in the housing sector.

Between 2002-2005 in many markets, the real estate market was scorching, much like it is today. Appraisers’ jobs relate to analyzing the market and reporting what we have analyzed in a manner that is factual and not misleading. Appraisers’ jobs are not to facilitate mortgage lending. We analyze and report.

Seriously though, there must be a ceiling to rising rates that have all but extinguished a robust housingmarket. While investors of mortgaged securities help dictate their interest rates, the Federal Reserve is behind the scenes influencing the overall lending environment. may be the better million-dollar question.).

Mortgage Lending You decide. Excerpts: Accurate appraisals are essential to the integrity of mortgage lending. percent, but remained close to its highest since 2002,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. Do not use lender forms. Type of report. Lender decides You decide.

In fact, mortgage rates over the last decade have been lower almost every month compared to those during the housing bubble years and we have not seen the massive sales we saw from 2002-2005. Nonetheless, during those years, existing home sales, new home sales, home prices, housing starts, permits, and completions were booming.

million Americans who live in homes financed with chattel — about 42% of the manufactured housingmarket — don’t enjoy the consumer protections that long-established legislative bulwarks afford those with a traditional mortgage. But the government sponsored enterprises may now be on the cusp of entering the chattel market.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content