This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

To get the housingmarket to be sane and normal again, we need inventory to get back in a range between 1.52 – 1.93 million ; this is still historically low, but this gives the housingmarket a breather from the madness that we see today. However, a seller is also a natural homebuyer, unless they’re an investor.

This data line lags the current housingmarket as it’s a few months old. Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. million, the housingmarket can be sane again, even though those levels were the historically low levels of inventory going back to 1982.

real estate investors and affordable homes. The June housing starts data beat estimates with positive revisions, however, this doesn’t change the housingmarket recession call that I made last month. As you can see, the entire housing marketplace is much different from what we experienced in 2008.

Just when I thought days on market were returning to normal, that number for existing homes fell back down to 22 days. If the days on the market are at a teenager level or even lower, it’s never a good sign for the housingmarket. housingmarket inventory channels have changed due to how the U.S.

million , with double-digit home-price growth driving a housingmarket that is still savagely unhealthy. This is something that I said would change the tone of housing, and we are seeing that result this year as sales decline and inventory picks up. We are not taking the unhealthy housingmarket theme off this marketplace.

However, the real story of 2022 is that the savagely unhealthy housingmarket continues as inventory is still lower than last year, sending home prices growth into double digits again. housingmarket; the 10-year is above 1.94%, something that didn’t happen in 2020 or 2021. From NAR : Total existing-home sales dipped 2.7%

One of the reasons that I moved into the “team higher mortgage rate” camp is that what I saw in January, February, and March of this year was so unhealthy that I labeled the housingmarket savagely unhealthy. million — once that happens, I can take the unhealthy label off the housingmarket.

With the banking crisis spurring more talk of a recession, the question now is: What would housing credit look like in a recession? housingmarket would crash during the pandemic. One of the main reasons for that fear was that housing credit was about to get tight, meaning fewer people could buy homes with mortgages.

It’s an excellent time to discuss housing inventory. The housingmarket shifted in March of this year. As the 10-year yield broke above 1.94% and mortgage rates rose, we saw the impact on housing data. Yes, crazy to think, but this is a survey trend data line, and the housingmarket was in free-fall at that time.

A lot of the housing data was lagging the rate move, so it wasn’t apparent that higher rates impacted the data yet. Going back to the summer of 2020, the one factor that I said could change the housingmarket was the 10-year yield getting above 1.94%. However, the housingmarket changed once the 10-year yield broke over 1.94%.

housingmarket , we just experienced an event that most people never thought could happen. However, in 2020 new listing data came back, and we don’t want to see the new listings continue to decline this year — that would be a double negative for the housingmarket. The days on market were too low.

We finally got mortgage rates to rise, and for people like me who have been concerned about how unhealthy the housingmarket was last year — and it got a lot worse this year — it’s a blessing that was much needed. Compared to the existing home sales marketplace, it doesn’t have a high cash buyer or investor buyer profile.

Knowing that the housing crash addicts on YouTube , Twitter , Facebook , and Clubhouse would incorrectly push the negative year-over-year data spin, I wanted to get ahead of that narrative. Then everyone went crazy on investors and iBuyers , suggesting that these people were holding up the entire housingmarket.

Some of their biggest hits (or should I say misses) in the last 8 years have been the never-realized silver tsunami crash, the ever popular investor supply crash, the Airbnb supply crash, and this year, COVID-19 was for sure going to send prices crashing 30%-50%. Housing data started to soften in 2005 after an overheated market.

The savagely unhealthy housingmarket theme of mine is running in full force now as we have gotten no relief on home prices and now have a mega jump in mortgage rates. . Since the summer of 2020, I have talked about what could change the housingmarket, which was a 10-year yield above 1.94%, which means rates over 4%.

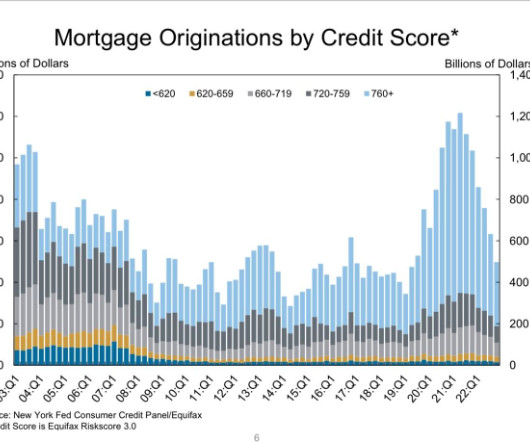

While the growth rate is cooling monthly, we are still in a savagely unhhealthy housingmarket trying to get national inventory levels back to pre-COVID-19 levels. However, we haven’t had a credit sales boom like the one we saw from 2002-2005. Case in point, purchase application data is already below 2008 levels today.

“The 30-year fixed-rate mortgage broke 7% for the first time since April 2002, leading to greater stagnation in the housingmarket,” Sam Khater, Freddie Mac’s chief economist, said in a statement. It may also be helpful to change the requirements of the down payment assistance programs, LOs say.

The bearish take on housing for the second half of 2021 didn’t really pan out, especially in the new home sales sector. What I believe occurred is that some housinginvestors took the decline in builders confidence and the increase in monthly supply to push that something bad was going to occur quickly. This is 11.9

Even in the extreme conditions of COVID-19, my general premise on housing economics predicted that the two variables with the most influence — demographics and mortgage rates — would hold up the housingmarket. Also, the market we have today doesn’t look like the credit boom we saw from 2002-2005. The forecast.

Seriously though, there must be a ceiling to rising rates that have all but extinguished a robust housingmarket. While investors of mortgaged securities help dictate their interest rates, the Federal Reserve is behind the scenes influencing the overall lending environment. may be the better million-dollar question.).

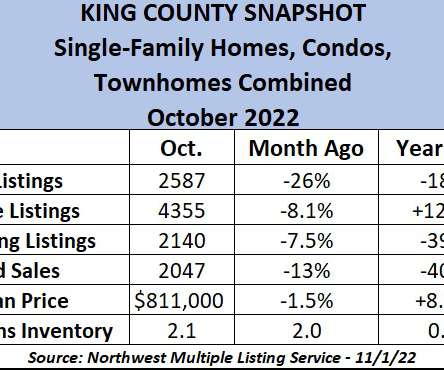

The housingmarket in and around King County was moving along swimmingly at the start of 2022, with homes selling briskly and buyers taking advantage of interest rates in the 3s. and jump in mortgage rates of 4 percentage points has created a housingmarket belly flop. We are in a new phase of the housingmarket cycle.

I have never been a housing sales boom person because I don’t believe we can have a credit boom in America like we saw from 2002 to 2005. The real goal is to get the days on the market to grow. As you can see below, we are far from that type of housingmarket. Preferably 30 days or more creates balance.

housingmarket follow Canada? In short, the answer is no, we won’t have the type of home-price velocity that Canada has experienced because our housingmarket is more diverse than theirs. housingmarket is more tied to mortgage buyers. from 2002-to 2005, which led to forced credit selling.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content