This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

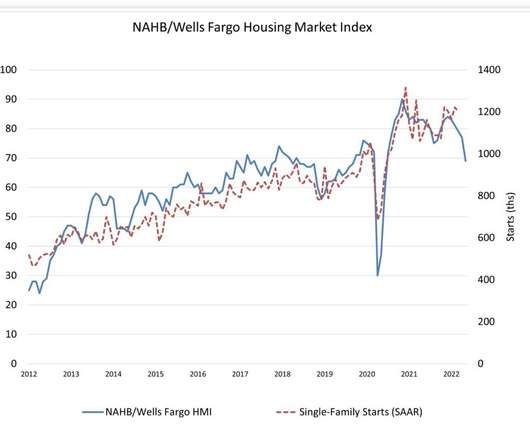

For this reason, the number of housing units “under construction” is the largest ever recorded in history because they were taking so long to finish. For the builders, they have a new problem: they had homes under contract and then mortgage rates jumped in the biggest fashion ever recorded in history.

I have been part of the mortgage banking industry since 1983 — 39 years to date through different housingmarkets. In many ways it was similar to today, with one exception: When I started, I hadn’t been spoiled by a housingmarket like the one in 2020 and 2021. economy, especially the mortgage and housing sector.

Marty Green thinks of the housingmarket in 2022 as two very different movies. ” Houses were selling at a fever pitch in a matter of days, with multiple offers, waived contingencies and buyers paying $100,000(!) But the housingmarket in the second half of 2022? over asking price. High octane stuff.

family housing starts in April were at a rate of 1,100,000; this is 7.3 As you can see below, the housing demand data from 2002 to 2005 was never apparent in any housing data lines from 2018 to 2022. When you don’t have a credit boom with exotic loan debt products, housing demand has limits. percent (±7.7

A lot of the housing data was lagging the rate move, so it wasn’t apparent that higher rates impacted the data yet. Going back to the summer of 2020, the one factor that I said could change the housingmarket was the 10-year yield getting above 1.94%. However, the housingmarket changed once the 10-year yield broke over 1.94%.

That means that our weekly pending sales contract data is showing growth year over year. The existing home sales print is catching up to our data, and this, to me, is the best story for housing in 2024 because when the housingmarket was savagely unhealthy in 2022, the NAR total active listings data was below 1 million.

housingmarket , we just experienced an event that most people never thought could happen. However, in 2020 new listing data came back, and we don’t want to see the new listings continue to decline this year — that would be a double negative for the housingmarket. The days on market were too low.

“The 30-year fixed rate decreased for the first time in over two months to 7.06%, but remained close to its highest since 2002.”. The Fed will announce the new federal funds rate’s target on Wednesday, which industry observers expect to increase by 75 basis points to 3.25%-4%. from the week prior.

The savagely unhealthy housingmarket theme of mine is running in full force now as we have gotten no relief on home prices and now have a mega jump in mortgage rates. . Since the summer of 2020, I have talked about what could change the housingmarket, which was a 10-year yield above 1.94%, which means rates over 4%.

Of course, that’s until you look at the housing completion data, which hasn’t gone anywhere in years. Housing starts data, like new home sales data, can be wild month to month, so the trend is always more important than any one report and the revisions are critical. has the most prolific housing demographic patch in history.

The housingmarket is in a recession, something that the homebuilders and the National Association of Realtors now agree with me on, as this recent CNBC clip shows. Over the years, I have tried to emphasize that the housingmarket in the U.S. can’t have a credit sales boom like we saw from 2002-2005. This is 12.6

Between 2002-2005 in many markets, the real estate market was scorching, much like it is today. Almost daily, there is some story on social media about being “turned in” to the state by a disgruntled agent, buyer, or seller for appraising a property below the contract price. We are seeing that as a profession again.

Seriously though, there must be a ceiling to rising rates that have all but extinguished a robust housingmarket. We are now seeing “7s” in front of some rates to new mortgage consumers – a figure not seen since April 2002 – causing applications for new loans to hit a 25-year low this month. ( higher compared with last year.

percent, but remained close to its highest since 2002,” said Joel Kan, MBA’s Vice President and Deputy Chief Economist. The average contract interest rate for 30-year fixed-rate mortgages with conforming loan balances ($647,200 or less) decreased to 7.06 The average contract interest rate for 5/1 ARMs decreased to 5.79

Dear Sellers, the housingmarket misses you It’s tough to value properties today! How does your market compare with Ryan’s? To read more, click here My comments: I remember the easy days before 2020, with enough sales, listings and pendings to figure out the market. percent, the highest rate since 2002.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content