This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. The housing market can’t replicate the type of massive credit expansion we saw from 2002-2005, so the price-growth story has more to do with inventory collapsing to all-time lows. Also, certain investors felt no fear post-2020.

However, a seller is also a natural homebuyer, unless they’re an investor. As you can see from this NAR report, cash buyers as a percent of sales is slightly lower now than levels in 2016. However, distressed sales are down a lot today compared to back then, and sales to investors are 19% today compared to 16% back then.

That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. The Baby Boomers are not selling their homes en masse, and we have more investors providing shelter for renters than before. If you connect the lines, you can see where we are on a historical basis. What is going on here?

real estate investors and affordable homes. Some buyers had to wait forever before they could lock in their rate, meaning they didn’t qualify for their homes as rates moved up so fast. We never saw the credit sales boom as we did from 2002-2005, so the builders themselves are in a better position to manage their future.

Then everyone went crazy on investors and iBuyers , suggesting that these people were holding up the entire housing market. I understand that grifters have to keep the grift going, but not even the Joker would say that the housing market lives off investors and not mortgage buyers.

From NAR : “December was another difficult month for buyers, who continue to face limited inventory and high mortgage rates ,” said NAR Chief Economist Lawrence Yun. This means we don’t have enough housing inventory available because with lending standards back to normal we can’t replicate the credit demand we saw in housing from 2002-2005.

It’s also driven more by mortgage buyers who tend to be older and make more money than the new-home buyers. Compared to the existing home sales marketplace, it doesn’t have a high cash buyer or investorbuyer profile. percent (±11.9 percent)* below the revised January rate of 788,000 and is 6.2 percent (±13.7

Because we had a housing credit bubble from 2002 to 2005, the credit demand push on exotic loan debt structures was a setup for future forced credit selling. Even though mortgage rates are historically low, they still always matter because mortgage buyers are the biggest homebuyers in America.

We don’t have a massive credit boom as purchase application data is at historical lows; we haven’t had the same run-up in credit as we saw from 2002-2005. This is why I always draw the black line on the chart below — to show people that we haven’t had a credit boom for many years.

A traditional primary resident seller is also a buyer, which means if they don’t list, they’re not just taking a potential home to be bought off the table — they’re taking a future sale off the books as well. However, it’s not the market of 2002-2011. From NAR Research : “Total existing-home sales notched a minor contraction of 0.4%

However, we haven’t had a credit sales boom like the one we saw from 2002-2005. One of the issues with existing home inventory has been that, for the most part, a traditional seller is usually a buyer of a home. I am not talking about investors; I am talking about primary resident homeowners. million listings.

The 30-year fixed-rate mortgage broke 7% for the first time since April 2002, leading to greater stagnation in the housing market,” Sam Khater, Freddie Mac’s chief economist, said in a statement. A year ago at this time, rates averaged 3.14%. The survey, conducted weekly since 1990, covers 75% of all U.S.

Housing demand has been stable for the past few years; we have never had a credit boom in demand since 2002-2005. From NAR : Total existing-home sales dipped 2.7% from February to a seasonally adjusted annual rate of 5.77 million in March. So, we never had a credit bust as we saw from 2005 to 2008.

history are ages 26-32, and the first-time median home buyer age is now 33. Again, what happened in housing from 2002 to 2008? Our market is much different than that 2002-2008 period. Don’t forget the mortgage buyer is the most significant homebuyer out there; they matter the most. We are currently a t 1.7

Also, the market we have today doesn’t look like the credit boom we saw from 2002-2005. In a B&B market, buyers have choices, sales move at a reasonable pace without bidding wars, and the whole home-buying experience is less stressful and more sane. However, one thing is for sure: demand has been solid and stable in 2020 and 2021.

Properties are ideal for young professionals, investors seeking properties to rent to college students, and established folks looking to settle in their home for the long haul. The majority of this neighborhood was built in 2002 and offers easy access to greenways adjacent to the Neuse River. Falls River is an impeccable area to see.

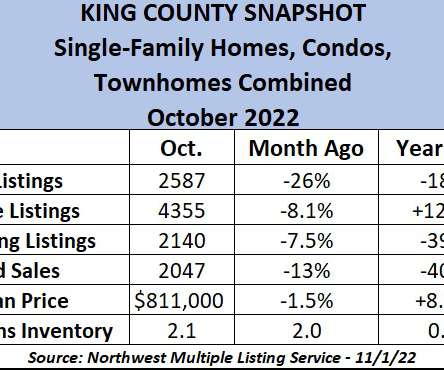

The housing market in and around King County was moving along swimmingly at the start of 2022, with homes selling briskly and buyers taking advantage of interest rates in the 3s. Historically low interest rates brought buyers and investors out of the woodwork for any homes for sale. Give us some cooling – stat! “We

In 2002, he joined the firm’s executive team, serving as president, before a nine-year stint as CEO from 2005 to 2014. ” Since 1991, Willis has served in various leadership roles within the company, including regional director, operating principal, team leader, and as a market center and region investor. That’s Mark Willis.”

Fannie Mae will end up creating more instability for the trillions in the bond market – investors will have to process millions of valuations with the physical attributes of the home collected by unlicensed, uninsured, and unprepared individuals getting paid $10-$25 per inspection. . Most buyers were tech people from the Bay Area.

While investors of mortgaged securities help dictate their interest rates, the Federal Reserve is behind the scenes influencing the overall lending environment. We are now seeing “7s” in front of some rates to new mortgage consumers – a figure not seen since April 2002 – causing applications for new loans to hit a 25-year low this month. (

I have never been a housing sales boom person because I don’t believe we can have a credit boom in America like we saw from 2002 to 2005. More Americans bought homes in 2020 and 2021 than any single year from 2008 to 2019, which looks normal. However, total home sales — new and existing — during 2020-2024 should be 6.2

housing market is more tied to mortgage buyers. Unlike those two cities in Canada, we aren’t as reliant on foreign buyers to such a great extent. Just last month, Canada’s prime minister proposed a two-year ban on some foreign investors buying Canadian real estate to try to tame price growth. In addition, the U.S.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content