This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Newly released data from the annual profile of home buyers and sellers by the National Association of Realtors (NAR) shows just how dramatically this trend has manifested since the financial crisis of 2008. While the median age of buyers gradually increased over the course of two decades, the COVID-19 pandemic sped it up.

In addition to the claims about artificially inflated agent commissions, the suit also alleges that NAR and its affiliated MLSs allowed agents to filter properties by commission amount, and that “NAR ethics rules allowed buyer-agents to show these filtered properties with higher commissions to buyers.”

I am so proud of our network and the professionals that work tirelessly to guide buyers and sellers on their home selling and buying journeys.” ” According to a spokesperson at HomeServices of America, Budnick has no immediate plans for her next steps or role.

The second part of this story that folks seem to forget is that the existing home sales market only needs 4 million mortgage buyers a year to remain stable. Note too, that the housing market for the last many years has been composed of 15-20% cash buyers – that is a big chunk of buyers that don’t need a mortgage in order to purchase.

Because housing demand is at pre-cycle highs, we can infer home prices are not an issue for most buyers. nominal home price growth every year for the next several years, affordability will be an issue for some buyers. However, this does not mean that real home prices may grow at an unhealthy pace in the years 2020-2024.

Since 2014, we’ve not seen the credit housing boom that we saw from 2002-2005. The housing market can’t replicate the type of massive credit expansion we saw from 2002-2005, so the price-growth story has more to do with inventory collapsing to all-time lows. This is because the biggest buyers of homes are mortgage buyers.

That’s not the case now because we have’t had a credit boom post-2010 as we did from 2002 to 2005. However, the spike in inventory that we saw from 2006 to 2011 can be attributed to the massive credit bubble we had from 2002 to 2005. If you connect the lines, you can see where we are on a historical basis.

. “This is about the same rate of price growth that occurred during the 2002 through 2006 period when subprime lending drove exuberant housing demand. “But that is where the similarities end.

Because housing is becoming an outperforming asset, we may see an increase in cash buyers in 2021 as a percent of sales. The majority of home buyers in America buy homes to live in, not for an investment. This is the big difference between the housing market now and what we saw in 2002-2005, when we saw a lot of speculation going on.

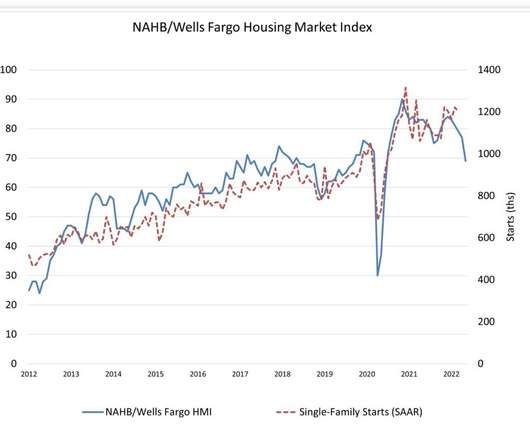

We simply cannot finish homes in America promptly, and now that mortgage rates are over 5%, some buyers won’t be able to purchase a home. Housing in 2020 and 2021 benefited from rates between 2.5% – 3.75% , which gave buyers more purchasing power. The builders are mindful of this and will be cautious on single-family starts.

housing market is more tied to mortgage buyers. Unlike those two cities in Canada, we aren’t as reliant on foreign buyers to such a great extent. foreign buyers have always been less than 300,000 of total home sales for many years. from 2002-to 2005, which led to forced credit selling. In addition, the U.S.

The housing market of 2002-2005 had four years of sales growth facilitated by credit. However, what isn’t identical is that we have not had a massive sales boom like we saw from 2002-2005. This is significantly different than the period from 2002-2005 when credit expansion was booming. Home sales. Housing credit.

Of course, housing starts today aren’t collapsing in the way they did from the peak of 2005 because we haven’t had a sales credit boom in recent years as we did from 2002-2005, which inflated new home sales toward 1.4 The credit cycle looks much different now than the build-up from 2002-2005.

Some buyers had to wait forever before they could lock in their rate, meaning they didn’t qualify for their homes as rates moved up so fast. We never saw the credit sales boom as we did from 2002-2005, so the builders themselves are in a better position to manage their future. This data line is already below 2008 levels currently.

.” Houses were selling at a fever pitch in a matter of days, with multiple offers, waived contingencies and buyers paying $100,000(!) The number of home listings dried up , contracts were canceled , the few buyers still out there demanded concessions , mortgage rates spiked to 7% and homebuilder sentiment hit rock bottom.

NAR Research : First-time buyers were responsible for 29% of sales in February; Individual investors purchased 19% of homes; All-cash sales accounted for 25% of transactions; Distressed sales represented less than 1% of sales; Properties typically remained on the market for 18 days. We have solid replacement buyers: people needing shelter.

During plaintiff lead attorney Michael Ketchmark’s cross examination of Warner, he presented her with some statistics showing that HomeServices affiliated agents in four Missouri markets paid buyer broker commissions of roughly 3% in at least 88% of the transactions completed between 2015 and 2022. It is human nature,” Frazier said.

As rates rise, this will impact the builders more as they try to find buyers for current homes in cancellation. As you can see below, housing completion data hasn’t done much for many years, unlike 2002-2005. But, this data line should grow a tad more while they finish up homes that they do have buyers for.

However, what is different this year from 2023 is that we have more sellers that will be buyers. Of course, the housing market didn’t have the credit sales boom it had from 2002-2005, but it lacked inventory. Just as they did in 2023, higher rates took the winds out of the growing sales numbers.

Loan buyers must offer loss-mitigation options that are as or more generous than FHA loss mitigation options when buying loans through the program, according to the rule. A pilot program for single-family loan sales has been in effect since 2002 and this final rule transitions it into a permanent program.

In 2002, he joined the firm’s executive team, serving as president, before a nine-year stint as CEO from 2005 to 2014. “With so much uncertainty surrounding the real estate industry today, it’s never been more important to have a leader who thoroughly knows us and understands business at the highest level,” said Keller. billion.

It’s also driven more by mortgage buyers who tend to be older and make more money than the new-home buyers. Compared to the existing home sales marketplace, it doesn’t have a high cash buyer or investor buyer profile. This sector on an apples-to-apples basis is more expensive than the existing home sales market.

Between 2002-2005 in many markets, the real estate market was scorching, much like it is today. Prices were escalating quickly, and buyers were purchasing in a frenzy for fear of being left behind and not being able to get their foot on the property ladder. This is no different than ignoring declining trends. How do we combat this?

From NAR : “December was another difficult month for buyers, who continue to face limited inventory and high mortgage rates ,” said NAR Chief Economist Lawrence Yun. This means we don’t have enough housing inventory available because with lending standards back to normal we can’t replicate the credit demand we saw in housing from 2002-2005.

This business model means that the builders are very mindful of the demand for their product and keep an eye out on their main competition, the existing home market, where supply is cheaper for a buyer. They can cut prices, pay down mortgage rates for their buyers, and do what they need to to make it work for them to move their products.

Traditionally, housing starts, permits, and completions would move together, like what we saw in 2002-2005. From 2002-2005 it was a steady rise to the top of the housing bubble, and then it burst. Over the last six weeks, we have seen that buyers came back in the data line when mortgage rates fell from 7.373% to 6.12%.

The second day of the trial for the Sitzer/Burnett bombshell class action buyer broker commission class action lawsuit included plenty of insights into how the plaintiffs are approaching what is expected to be a battle royal. When you reduce the commission, you reduce the incentive for that agent to bring a buyer to your house.

We had more housing starts during the bubble years because from 2002 to 2005 that demand curve was higher, but it was facilitated by unhealthy credit growth. The buyers are frustrated beyond belief with how long the process is taking while they watch rates rise. As we can see below, slow and steady wins this race.

I understand that grifters have to keep the grift going, but not even the Joker would say that the housing market lives off investors and not mortgage buyers. As you can see below, we don’t have a booming credit housing market as we saw from 2002-2005; we have steady replacement buyer demand.

Because we had a housing credit bubble from 2002 to 2005, the credit demand push on exotic loan debt structures was a setup for future forced credit selling. Even though mortgage rates are historically low, they still always matter because mortgage buyers are the biggest homebuyers in America.

It boxed out many first-time homebuyers who found themselves unable to compete against buyers willing to place a non-contingent offer above full price. In fact, while in won’t match 2020 or 2021, purchase mortgage dollar volume should be better than any year from 2002–2020. Buying now means being able to negotiate as a buyer.

A traditional primary resident seller is also a buyer, which means if they don’t list, they’re not just taking a potential home to be bought off the table — they’re taking a future sale off the books as well. However, it’s not the market of 2002-2011. From NAR Research : “Total existing-home sales notched a minor contraction of 0.4%

This time around, we have not seen the kind of housing credit boom that we did from 2002-2005. NAR total inventory data 1,250,000 One thing about purchase application data and demand is that a traditional seller is typically a buyer of a home. Post-2012, whenever mortgage rates rise, existing home sales always trend below 5 million.

As you can see from the chart above, the last several years have not had the FOMO (fear of missing out) housing credit boom we saw from 2002-2005. million, the equilibrium balance between a buyer and seller marketplace that has been here for four decades. Accordingly, we also haven’t had a credit bust in the data line.

We don’t have a massive credit boom as purchase application data is at historical lows; we haven’t had the same run-up in credit as we saw from 2002-2005. This is why I always draw the black line on the chart below — to show people that we haven’t had a credit boom for many years.

The new home sales market doesn’t have a 28% cash-buyer profile as we saw in the last existing home sales report. So, while cash buyers as a percent of sales have been growing, this sector is driven by mortgage buyers primarily. Builders have to find buyers for canceled homes, then think about their demand.

In addition, some white neighborhoods had zoning laws that legally banned non-white buyers from owning homes in those neighborhoods. million new minority homeowners when the president launched the Blueprint for the American Dream in 2002. This means that the most likely buyer for many of these new retirees will be a minority family.

However, we haven’t had a credit sales boom like the one we saw from 2002-2005. One of the issues with existing home inventory has been that, for the most part, a traditional seller is usually a buyer of a home. Nor can we ever have a credit sales boom again with lending standards back to normal. million listings.

The 30-year fixed-rate mortgage broke 7% for the first time since April 2002, leading to greater stagnation in the housing market,” Sam Khater, Freddie Mac’s chief economist, said in a statement. A year ago at this time, rates averaged 3.14%. The survey, conducted weekly since 1990, covers 75% of all U.S.

So, early in my career, I sought for ways to help would-be buyers, most being minorities, bridge the gap and achieve homeownership earlier. In the early 2000s, many — including myself — believed empowering someone with a home for sale to contribute to the buyer’s down payment was a small way to help deserving families.

Logan Mohtashami: Rising rates make housing less affordable, so for a first-time home buyer that doesn’t have the benefit of selling their home with that nested equity, it makes it harder for them. This is much different from the marketplace we saw from 2002-2005, a massive credit bubble. months on a 3-month average.

history are ages 26-32, and the first-time median home buyer age is now 33. Again, what happened in housing from 2002 to 2008? Our market is much different than that 2002-2008 period. Don’t forget the mortgage buyer is the most significant homebuyer out there; they matter the most. We are currently a t 1.7

Housing demand has been stable for the past few years; we have never had a credit boom in demand since 2002-2005. From NAR : Total existing-home sales dipped 2.7% from February to a seasonally adjusted annual rate of 5.77 million in March. So, we never had a credit bust as we saw from 2005 to 2008.

can’t have a credit sales boom like we saw from 2002-2005. The housing construction cycle is over, but the builders will finish their homes under contract and hope rates will fall soon to lock up buyers. Now the trick for the builders is figuring out how much they need to discount to get buyers to buy the homes under construction.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content