This site uses cookies to improve your experience. To help us insure we adhere to various privacy regulations, please select your country/region of residence. If you do not select a country, we will assume you are from the United States. Select your Cookie Settings or view our Privacy Policy and Terms of Use.

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Used for the proper function of the website

Used for monitoring website traffic and interactions

Cookie Settings

Cookies and similar technologies are used on this website for proper function of the website, for tracking performance analytics and for marketing purposes. We and some of our third-party providers may use cookie data for various purposes. Please review the cookie settings below and choose your preference.

Strictly Necessary: Used for the proper function of the website

Performance/Analytics: Used for monitoring website traffic and interactions

Home construction New home construction ramped up early in the pandemic but moderated as interest rates ticked up and mortgage rates followed. The seasonally adjusted annual rates of homes permitted, started, under construction and completed all remain well above pre-pandemic levels but below the peaks reached in the last three years.

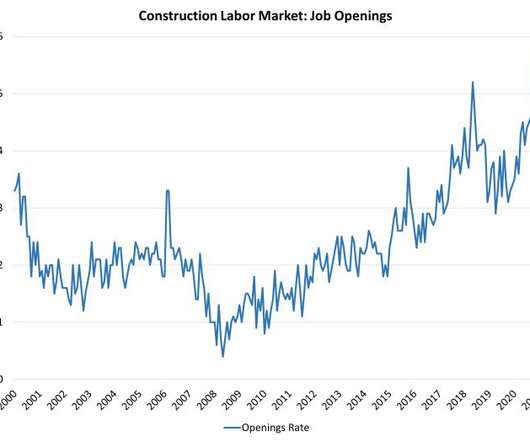

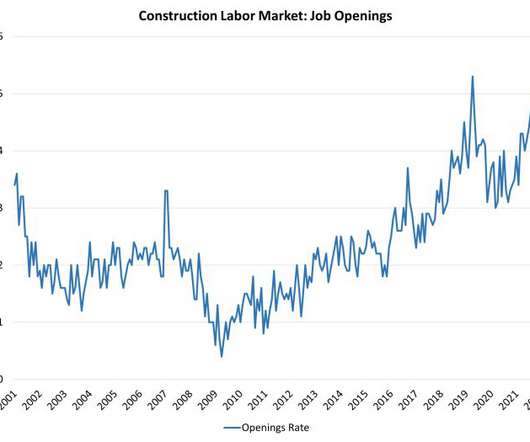

The construction labor market remains tight, as the industry sees a rising number of job openings year-over-year. The count of open construction jobs increased for the month to 380,000 unfilled positions in January. The highest measure in the history of the data series (going back to late 2000) was 416,000 in April 2019.

New construction starts and permits showed surprising strength in October while existing-home sales slumped to their worst reading since 2010. Except for the last seven weeks, current mortgage rates hit their highest levels since 2000.

By extension, Zonda also acquired NewHomeSource.com , one of the largest listings platforms for newly constructed homes, and Envision , a new home design platform. Founded in 2000, BDX is owned by a group of 24 leading U.S. Zonda will be able to integrate its new construction data and tech platform with the leading portal for U.S.

The construction labor market remains tight, as the industry sees a rising number of job openings year-over-year. The count of open construction jobs jumped to 449,000 unfilled positions in April. This is the highest measure in the history of the data series (going back to late 2000).

The construction labor market remains tight, as the industry sees a rising number of job openings year-over-year. The count of open construction jobs remained steady at 381,000 unfilled positions in February. The highest measure in the history of the data series (going back to late 2000) was 416,000 in April 2019.

The labor market continues to tighten, especially for the construction industry. The count of open construction jobs increased to 410,000 unfilled positions in October, the highest measure in the history of the data series (going back to late 2000).

This data line confirms what we all know to be the case: The housing market, at least as it relates to construction, is in a recession. We talked about this in March , and even last year, when I wrote about the problem with the housing construction boom premise. “I don’t expect a boom in housing construction.

The construction labor market remains tight, as the levels of quits rise. The count of open construction jobs declined to 345,000 unfilled positions in November, after recording the highest measure in the history of the data series (going back to late 2000), 445,000 in October.

We are well below the 2000 recession level and back to 1996 levels. When you account for a population of over 330 million people, that sales number looks a lot lower than in 2000 and 1996 so be mindful that we are trending at low levels today. The builders will pull back on construction when the supply is 6.5 When supply is 4.3

The Census Bureau’s Survey of Construction (SOC) provides valuable information on the characteristics of new homes started construction, such as air conditioning and heating system installations. The trend, going back to 2000, shows a steady rise in the share of. Air Conditioning In 2022, 97.1 percent in 2021.

Without rents taking off, the CPI data would look much more tame, like what we saw from the years 2000-2019. However, because of the COVID-19 delays, we are still working through a backlog of homes under construction. As you can see in the chart below, we have a historic number of 5-unit construction in the works. Since 44.4%

New home sales are now below the recession levels of 2000 and have fallen all the way to 1996 levels, when interest rates were near 8%. The builders will pull back on construction when the supply is 6.5 When rates rose back in March, there was a considerable risk to the business model with many homes under construction.

From the National Association of Home Builders : Looking at the housing starts report, the numbers came in slightly better than anticipated, driven by multifamily construction. Still, it’s backward-looking and the growth in multifamily construction, which we desperately need to cool down rental inflation, has recently been positive.

New home construction is taking on an increased role in the marketplace because many home owners with loans well below current mortgage rates are electing to stay put, and this is keeping the supply of existing homes at a very low level ,” Alicia Huey, the NAHB chair, said in a statement. That share from 2000-2019 was a 12.7%

The construction labor market remains tight, as the industry sees a rising number of job openings year-over-year. The count of open construction jobs increased slightly to 396,000 unfilled positions in March. The highest measure in the history of the data series (going back to late 2000) was 416,000 in April 2019.

Homebuilders responded to the shortage of homes for sale, accelerating new home construction, even as they face severe supply-side challenges, including rising building material costs and supply-chain bottlenecks, a lack of affordable lots, and difficulty in finding skilled labor. What about existing homes?

In fact, new home sales are below the recession level of 2000 and back to 1996 levels already. The builders will pull back on construction when the supply is 6.5 That’s not a lot of homes and the builders will take their sweet time building out the rest of the homes in construction and the homes that haven’t even been started yet. .

Mortgages rates reached their highest level since 2000 , construction costs rose and building regulations remained burdensome, leaving U.S. housing affordability near a 10-year low point at the end of last year, according to the National Association of Home Builders (NAHB). median income of $96,300.

The construction labor market remains tight, as the industry sees a rising number of job openings year-over-year. The count of open construction jobs declined for the month to 337,000 unfilled positions in December. The highest measure in the history of the data series (going back to late 2000) was 445,000 in October 2021.

Strategic Solutions for Today’s Homebuyers New construction financing and meeting the demand for new homes: According to the National Association of Home Builders (NAHB), in March, 33% of all home sales were new construction financing. That is a significant increase from the 13% average between 2000-2019 in new construction.

As we can see in the chart below, we are still below the recession levels of 2000 and really trending at 1996 levels. months of the supply is active listings, 68K 5 months of the supply is still under construction, 280K 1.6 The builders will pull back on construction when the supply is 6.5 When supply is 4.3 When supply is 4.4

As you can see below, new home sales are still below the 2000 recession level, and we just had a significant spike in mortgage rates too. Five months of the supply are homes in construction. That is a high level, and two months of the supply hasn’t started construction yet, and a whopping 0.68 This is 10.7 percent (±18.9

So for now, the builders will take their time with the homes under construction and make sure they offer enough incentives to unload the new home supply they’re dealing with. This is below the recession levels of 2000 and back to 1996 levels. This time, we have less production of homes and more multifamily construction.

assessed three separate elements of the HECM program’s effectiveness from 2000 to 2020 — including borrower impacts, financial impacts and policy impacts. In its executive summary, the report found that the HECM program grew “substantially” during the 2000s and reached its height of 114,000 originations in 2009.

Unfortunately, the rising cost of construction forces developers to find more funding sources to complete these projects. As a result of rising construction costs, the Terner Center for Housing Innovation estimates that the average number of loans per project on top of tax credits has doubled in the past two decades from two to four.

Multifamily construction is different than single-family homes. We are already below the 2000 recession levels. While this data line isn’t crashing, the ability to grow from these levels is limited with rising mortgage rates. From Census: Housing Completions Privately? The 5th recession red flag.

It was 2000, and the real estate market was fairly uneventful – rates were around 8% and house prices were affordably flat. With resale inventory shockingly low, 1 out of 3 single family homes for sale is new construction. HousingWire : What has been one of the biggest learning opportunities in your career?

The Census Bureau’s Survey of Construction (SOC) provides valuable information on the characteristics of new homes started construction, such as air conditioning and heating system installations. The trend, going back to 2000, shows a steady rise in the share. Air Conditioning In 2020, 95.4 percent in 2019.

The MHCC is a statutory Federal Advisory Committee body charged with providing recommendations to the Secretary on the revision and interpretation of HUD’s manufactured home construction and safety standards and related procedural and enforcement regulations.

metro areas going back to 2000. But multifamily construction starts have slowed , which is good news for landlords looking to increase rents. While investors are still sensitive to mortgage rate changes, they are less sensitive than consumer buyers as 69% of investors pay in cash.

NAHB analysis of the Survey of Construction (SOC) shows that 72.4% in 2000 to 72.4% of new single-family homes started in 2023 were built on slab foundations, 16.6% were built with full or partial basements, and 9.9% with crawl spaces. The share of new homes built on slabs has risen steadily from 45.8% in 2023.

As an Irish immigrant to the United States in 1996 who became a real estate broker in 2000, I can tell you this: The U.S. I have been following the discussion around the competitiveness, costs and consumer benefits of U.S. Multiple Listing Services (MLS) by those trying to disparage the system. It’s a trusted, predictable process.

The number of entry-level homes represent less than 10% of all newly constructed homes, compared to about 35% in the 1970s. Entry-level home prices have risen 62% faster than higher-end home prices since 2000, largely driven by millennials reaching the home buying age.

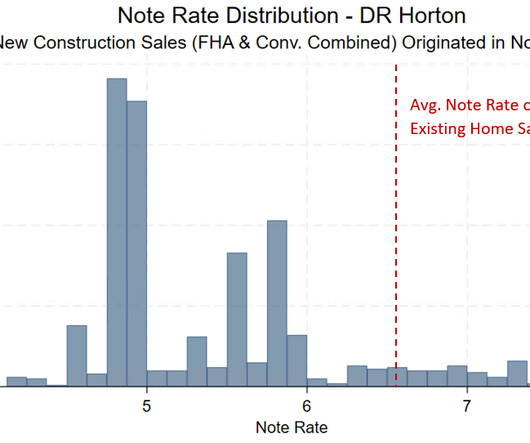

After a long period of rate repression, the Federal Reserve began aggressive monetary tightening, which would ultimately send mortgage rates to their highest levels since 2000. The gap peaked in November 2022, when the average note rate for new construction sales was one percentage point lower than the rate for existing home sales.

As I have explained, this started in the year 2000, when total active listings grew from 2 million to 2.5 The housing economy is built on housing construction, and the recession that started in June meant housing permits were going to fall, which they have. million in 2005.

The Time Warner precedent-setting mall scenario included a condo offering plan circa 2000 named "AOL Time Warner Center" and then the project was renamed "Time Warner Center" after they sold off AOL (Someone named Jonathan Miller took over AOL strangely enough).

The Census Bureau’s Survey of Construction (SOC) provides valuable information on the characteristics of new homes started construction, such as air conditioning and heating system installations. The trend, going back to 2000, shows a steady rise in the share of. percent in 2020.

The building rate of the previous decade struggled to keep up with the pace of the 2000s when homes were being built at nearly twice the rate ! The number of constructed homes dropped below the million mark in 2008 for the first time since 1992. Clearly, construction is not keeping up. either quit or lost their jobs.

Below is a direct comparison of all sales in the Ann Arbor school district excluding new construction and “to be built”. This information takes into account all listed houses in the Ann Arbor school district other than “to be built” and new construction. 2000-2999 increase in sales 1.27%. 2000-2999 sqft increase 5.21%.

By 2000, the proportion had dropped to 5.7%. Today, older homes tend to have smaller floor plans, while more recent constructions are more spacious. Some newer constructions may offset this footprint with energy efficient features. People moved into bigger houses with more land outside the densely packed cities. In 1950, 15.7%

Data was pulled from the year 2000 to the present date. Approximately 6% of sales in the neighborhood were new constructions. For instance, the 50th percentile, or median rank, shows that half of all sales since the year 2000 have been under $340,350. With that out of the way, let’s look at some neighborhood stats.

Data was pulled from the year 2000 to the present date. Approximately 3% of sales in the neighborhood were new constructions. For instance, the 50th percentile, or median rank, shows that half of all sales since the year 2000 have been under $279,900. With that out of the way, let’s look at some neighborhood stats.

March 2025 Winners of the Top 10 for the Company are: (IN ALPHABETICAL ORDER BY LAST NAME) Laurie Howe Bourgeois , a licensed REALTOR since 2000 with over 650 successful sales, joined Lamacchia Realty Leominster in 2019. Additionally, she has beena consistent NCMAR Top Producer from 2000-2022 and received the RACM Diamond award in 2023.

We organize all of the trending information in your field so you don't have to. Join 9,000+ users and stay up to date on the latest articles your peers are reading.

You know about us, now we want to get to know you!

Let's personalize your content

Let's get even more personalized

We recognize your account from another site in our network, please click 'Send Email' below to continue with verifying your account and setting a password.

Let's personalize your content